你们想学习用期权交易增加标普500 ETF的投资报酬率吗?

今天我要教大家一个特殊的「滚轮投资法」让你的S&P 500 ETF投资报酬率加倍。

为什么想买标普500的ETF?

我想听说过标普500的人都知道这是世界最具代表性的指数,主要是从美国股市中最大的公司里挑出500间相当优质的公司并追踪他们的表现。

S&P 500的公司市值大约占美国股票市场80%的市值,不但对大盘的走向具代表性,也是被动投资达人最好买、最好分散风险的指数。

只要购买并长期持有追踪标普500指数的ETF可以期待每年9%的投资报酬率。

从S&P 500指数中追踪的公司中可以看到我们常听到的优质公司,例如Apple、Google、Facebook、Netflix、Disney等,Tesla也在去年十二月新加入了指数中。

所以购买标普500的ETF等于是同时投资这些优质的公司,而且又可以分散风险,一举两得。

什么是「滚轮投资法」?

滚轮投资策略主要是结合购买股票和交易选择权的一连串SOP,让投资人能够不只享受股票波动的获利,在股价不动时还可以收取销售期权的收入。

投资期权的达人都知道,卖选择权主要是根据股价的波动定义获利区间,如果股价涨跌大于预期,就可能会赔钱,所以滚轮投资法特别适合像是标普500 ETF这种风险分散,涨跌幅度不大的股票。

哪一个S&P 500 ETF最适合滚轮策略?

目前追踪S&P 500最受欢迎的几个ETF是SPY、 IVV、VOO,这三个ETF追踪标普500的准度不同、管理费也不同,所以你可能会问要怎么挑选ETF最适合滚轮策略。

因为滚轮投资策略的基础是使用选择权交易增加股票的投资报酬率,所以我们主要以期权交易量作为挑选ETF的主要标准。

| 标普500 ETF | 选择权日交易量 |

|---|---|

| SPY | 2,272,620 |

| IVV | 253 |

| VOO | 111 |

如果我们参考这三个ETF单日的期权交易量,可以看到SPY的交易量远高于其他两个,所以我们挑选SPY为最适合交易期权的标普500 ETF。

滚轮投资策略的三个步骤

滚轮投资的主轴是订出一个搭配持股,能在不同的持股数量下销售期权的SOP,不但能增加ETF的投资收入,也能降低股票购买的成本。

根据不同的SPY持股状态总共有三种不同的步骤:

- 在没有持股的情况卖Cash-Secured Put。

- 持有100股的时候卖一个Strangle (也就是卖Put加Covered Call)。

- 在持有200股的情况卖两个Call options。

步骤一在没有持股的情况卖Cash-Secured Put Option

当我们没有持股的情况时,可以卖一个30天的Cash-Secured Put option。

如果30天后SPY的价格没有低于合约价,卖Put的收入就可全部入袋。

如果SPY下跌而提前履约Put option,我们就会便宜买到100股SPY,接下来滚轮策略就走到下一个步骤。

步骤二持有100股的时候卖一个Strangle

既然你取得了100股,接下来就可以卖一个Strangle,也就是Cash-Secured Put和Covered Call的期权。

如果30天后SPY的价格不动,卖期权的收入就全部收下。

如果SPY价格上涨超越Call的合约价并且被履约,就把现有的100股以高价卖掉并退回步骤一。

如果30天后SPY价格下跌低于Put的合约价并被履约,就便宜买入100股的SPY并前进到步骤三。

步骤三在持有200股的情况卖两个Covered Call Options

现在我们拥有了200股的SPY ETF,这时就可以一次卖两个Covered Call合约,加倍我们的Call options收入。

如果30天后SPY的价格不涨 ,卖选择权的收入就全部收下。

如果SPY价格上涨超越Call就把手上的200股以高价卖掉并退回步骤一。

要怎么订定Put和Call的行权价最好?

从SPY的历史数据来看股价涨跌很少超越Bollinger Bands的上下限,所以在Bollinger Bands卖Put和Call是最简单又CP值最高的。

现在SPY的Bollinger Bands上下限价格正好是376元和394元,所以我们可以用这两个价格设定卖Put和Call的期权价格。

另一个方便的定价方式是参考选择权神器挑选0.20 delta的Strangle价格。

| Symbol | Last | Strangle details | Strangle BP | Strangle ROC |

|---|---|---|---|---|

| SPY | 383.63 | C396(0.19) P361(-0.20) | 4313 | 10.5% |

根据选择权分析神器0.20 delta的Strangle:

- 由396元的Call和361元的Put组合而成

- 如果没有持股,需要使用4313元的购买力,有10.5%的投资报酬率

滚轮投资SPY的理想投资报酬率

我们可以用步骤二来计算滚轮投资SPY的理想报酬率,如果我们预估SPY的波动几乎不会超过我们参考Bollinger Bands的376元Put和394元Call价格,我们从卖期权的收入就大约是每个月1200。

我们为200股SPY准备的现金是7万7千元,所以每个月的选择权收入有1.6%,全年就有19%的收入。

长期持有SPY ETF和滚轮投资法的差异

如果长期持有SPY每年平均获得9%的报酬,那滚轮策略可以再增加19%的期权收入,让我们投资SPY ETF每年报酬率达到3倍以上。

| 交易方式 | 持有SPY ETF | 滚轮投资策略 |

|---|---|---|

| 最少投资 | $383 | $77,000 |

| 年报酬率 | 9% | 28% |

最适合滚轮策略的价值股票

滚轮策略适合稳定成长的绩优股,所以我们使用看涨价值投资清单找到现在适合滚轮策略的公司进场。

既然要靠滚轮策略长期投资,我们可以筛选股息贵族,也就是至少25年连续增加配息的绩优公司,在筛选器Years of Dividend Growth 25年以上。

接下来再用Dividend Yield排序,就能得到涨股息贵族中最高殖利率的公司清单。

| 股票 | 收盘价 | 殖利率 | 连续利息成长年份 |

|---|---|---|---|

| SJM | $115.05 | 3.81% | 27 |

| SYY | $78.96 | 2.55% | 54 |

| BDX | $225.12 | 1.84% | 52 |

| MSA | $168.97 | 1.17% | 53 |

| SEIC | $84.23 | 1.14% | 33 |

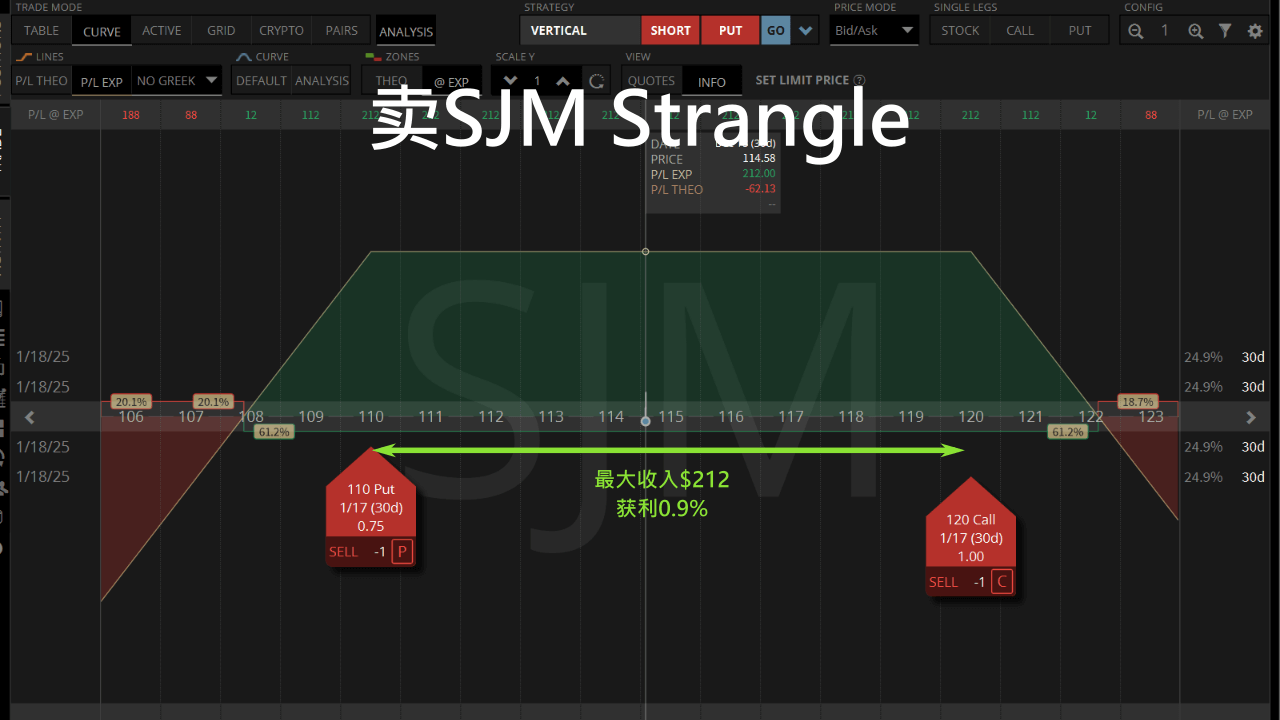

现在殖利率最高的股息贵族是SJM,如果要滚轮投资,就需要准备$23,000购买200股。

30天后截止的SJM 0.20 delta Strangle会获得$212的收入,所以滚轮投资能让我们每个月增加0.9%的收入,大约每年11%。

| SJM股息 | 滚轮投资获利 | 合并年获利 |

|---|---|---|

| 3.81% | 11% | 14.81% |

再加上原本持有SJM的3.81%殖利率,使用滚轮投资可以期待大约14.81%的年获利。

Hi, can this strategy work in IWM? Thanks

Yes it can, try it.

好奇如果這樣的方式改用TQQQ或是UPRO操作, 效果如何呢?

只要波動不大、要長期持有就適合滾輪投資

Nice article Tony!

One question, comparing (benchmarking) the wheel strategy to buy and hold, do you have any insight whether the “frequency” ofgoing through that wheel strategy amplify or kill return?

frequency meaning you set the delta threshold to have step1,2,3 happen quickly.

Thanks,

We find monthly expiration option contracts give the best risk/reward ratio.

So we usually sell the options that expire at least a month away.

你好 感謝你寫了這一篇文章

我有問題 如果資金不足的話 你建議用SPLG取代SPY嗎?

聽說流動性差很多 請問會有多大的影響呢?

可以啊

SPLG價格比較低,用的資金就比較少

流動性雖然比較差,但是如果是散戶要買賣一兩個合約不會有問題

感謝回答 另外還有一個問題

用滾輪在牛市的時候是能多賺3倍的話

那如果有一天進入像2022年那樣的熊市時 是不是會多虧3倍呢?

不會多虧3倍喔

滾輪策略賣選擇權一定會有收入

當股票下跌時,會用較便宜的價格買到股票

所以虧損一定比單純買股票少

Thanks for the information. Any thought on back testing this strategy selling the put in step 1 atm?

Well, we are selling ATM Put Spreads on our Bull Put Spread Screener most of the time and our winning rate is about 75%.

If you use the Wheel Strategy then the winning rate is less relevant as the “losing trades” are held to sell Covered Callsagainst.

请问下文章上期权的收益损失范围图是用的什么软件呢

这是用tastytrade

After being assigned, would selling a straddle be more advantageous than selling a strangle?

That can work if you want to quickly move on to either step 1 or 3.

The straddle means you will always be assigned next, either sell the 100 shares or buy 100 more.

The premium received would be higher than a strangle though.

The figure showing “$376 Put and $394 Call is around $1200 per month” seems to have put/call with expirationof 41d. So the 1.6% return is for 41 days instead of one month. I am also trying to check the current SPY options, can’t find a way to achieve1.6% monthly return. Did I miss anything?

You are right about the timeframe of the expiration, it’s an assumption.

The returns from selling neutral options are lower at the moment because VIX is quite low, which means the volatility is low.

Hence the premium received would be lower right now.

Do you think adding QQQ is a good idea or stick to SPY if you are mostly looking for safety?

QQQ has been working out for me with nice premiums and ability to roll quickly but spy feels a lot less volatile. However when looking at 10 year chart (Monthly), they seem to go hand in hand. What do you think?

I think the point of the Wheel Strategy is to balance less risks and more premiums from the options.

Both QQQ and SPY give you less risks than stocks.

While a slightly more volatile QQQ should give you better premiums and wider Call/Put strike prices.

It’s good to test the two ETFs then decide which gives a better balance for you.

Thanks for your reply.

So far I’m really enjoying SPY and QQQ and don’t have to worry about management, earnings etc

I have learned so far as you mentioned that qqq has better premiums but SPY is a bit more stable.

Covered strangle is working out nicely and adjusting positions up or down depending on market mood

Following your suggestion to use the upper and lower bounds of Bollinger bands for SPY, I come up with 404 and 418 as the strike prices for put and call,respectively. However, your options scanner for 0.20 delta indicates 386 and 427. Big difference! How can this be explained?

I double-checked the 0.20 delta suggestions on SPY, and it seems to fit with the trading platform’s numbers for expirations 7/21 and 6/16.

Can you confirm if the expirations you are looking at are the same?

If so, then the differences may be explained by the delay in data.

Hi, step number 1 considering SPY as underlying, at which delta do you recommend the first trade?

0.20 delta is a good starting point

Is the choice of the strike mainly delta or do you also consider other factors such as high premium, volatility, open interest, volume, earnings, or other?

The Options Scanner is quite useful in picking high return 0.20 delta Strangles to trade the Wheel with

https://slashtraders.com/en/tools/options-scanner/

Use the filter to find high IV stocks (>60%) that have high premium to sell options with, and sort by Strangle ROC to get the best return Strangles

When you’re in Step 1 of the Wheel, you’re selling only one cash-secured put, which means collecting only one premium. Theother two steps involve collecting two premiums. Is it advisable to sell two puts in the beginning, or else one put with a strike price closer to the stockprice, in order to increase the premium?

If you sell 2 cash-secured Puts in step 1, you will need to double the contracts in steps 2 and 3 later as well.

Selling a Put with a closer strike is preferable from the two choices you mentioned.

Why are you adding the theoretical pct return to the buy and hold return to come up with 28%? If you’re doing the whell strategy ur notrealizing the 9% gain from buy and hold, ur in and out of the ETF, so I’m not understanding your math.

28% is a hypothetical return based on step 2, sell a Strangel while holding 100 shares:

Buying and holding the ETF, gaining 9%/year

Both short Put and short Call options expire worthless, receiving a premium of around 19%/year

So you only make 28% if both the put and call from the strangle expire worthless in all 12 months? That’s extremely unlikely to actuallyhappen, right?

Yes and no.

It’s a general assumption.

If the Put get assigned, you get to buy stocks at a discount.

If the Call get assigned, you sold your stocks for a profit greater than the premium earned.

It’s about being profitable long term.

Hi, is there any ready etf that do all this mechanics?

Not that I know of.

Tony您好

我看了您兩篇文章

第一篇是「滾輪投資策略」

第二篇是「我們不愛交易Covered Call的理由」

然而我們都知道,「滾輪」必然會使用到「covered call」,您這樣不就是自相矛盾嗎?

建議您修改一下「covered call」的標題,不要誤導那些不太懂選擇權,但信任您的人。

謝謝您的留言

Covered Call雖然好上手,不過有幾個缺點讓我們不太愛交易它

我們誠實分享我們的想法讓讀者做決定

Hi Tony,

I have been trying wheel strategy with paper money. At what point do we need to cut losses if the stock moves below the put strike? since we will be paying morethan the spot price at assignment.

Are there any adjustments that should be considered?

Thanks

Vishal

Hi Vishal,

Actually, we prefer to trade wheel strategy on stocks that we want to buy and hold for the long term.

So we don’t mind buying the stocks when the spot price moves below the Put.

If we anticipate the blue-chip stock to be valuable in the long run, a temporary dip isn’t that big of a deal.

We just keep selling the Covered Call until we sell the shares for a profit.

Cheers

How do we avoid the “Wash-Sale” in short cycles (monthly or weekly) when ETF keep getting assigned?

After you get assigned the undervalued shares you can sell Covered Calls with monthly expiration as the underlying moves from significantly undervaluedto significantly overvalued.

When an underlying is 30-40% overvalued, you can start selling at 0.15-0.40 delta Covered Calls.

The transition of the underlying from undervalued to overvalued takes a long time and will not be at risk with the wash-sale rules.

Should your underlying be called away, you will not regret it too much because your gain from valuation has been significant.

Hi, if let’s say now we are holidng 200 shares of SPY and SPY crashed, how do we set the strike price for selling calls as we are still in capitalloss?

Thanks in advance.

It depends.

If you expect SPY to bounce back quite quickly, then you can set the Call strike at the breakeven price.

If you expect SPY to stay low for a while, then maybe set the Call strike at 0.20 delta (assuming that is lower than the breakeven price), to earn a betterpremium.

Hi Tony, wow – not complicated but highly effective, thank you so much!

Would it be a advantage to use the weekly contracts in SPY, for example always Friday?

Hi Chris,

We prefer trading monthly options because the theta decay is more predictable, leading to higher probability trades.

We don’t trade weekly contracts because the time to expiration is too short, as that would mean trading gamma not theta.

Gamma is much more unpredictable than theta.

Also, weekly options have less premium due to less time value, so you don’t get as much income from selling options.

What if I own 500 stocks?

Sell 400 calls and one strangle?

Yes, selling 4 Covered Calls and 1 Strangle can work in your situation.

The wheel strategy does seem like a great way to increase my returns on dividend stocks

Yes, you can combine the wheel with high yield dividend stocks to improve your returns

如果卖put被assign了?被assign的股票又在持续下跌,碰到这种情况卖call的话, strike price应该设在哪个位置比较好?设太高,premium赚不了多少,设太低,那股票可能低价卖掉,造成亏损。

如果不想长期持有股票,当Put被assign了的时候,可以卖一个Call在当初Put的strike

这样收入应该还够高,如果股价涨回来就会回本

On what chart are you using the bollinger bands? Because it is different if you use a year chart, 5 year, or 180 days?

We use the Bollinger Bands on the daily chart

It’s an estimation of 2 standard deviation move

Shouldn’t matter too much if you use a year chart, 5 years, or 180 days

你好TONY。。。如果選擇STRIKE的时候刚刚BOLLINGERBAND是在常窄,選擇的STRIKE也非常緊貼現貨價。。。這樣不是會很危險嗎?因為Bollinger Band在收窄之後,很自然的會擴闊到很大!!!這樣的話,不是很容易輸錢嗎??

您好Eric

是的所以我們通常要在Bollinger bands比較短的時候賣期權收入比較高,也可以等IV縮小時靠Vega獲利

这个方法在市场暴跌的时候适用吗

这个交易方式在市场暴跌的时候会以低价买到100股

接下来就可以用卖Call的方式赚收入等待股价上涨

This is a great options strategy, thanks

You’re welcome

Thank you for the detailed explanation of how to use the wheel strategy to increase the returns of my SPY

Yes, the wheel strategy is a simple way to use options to increase your long term returns

Current prices for calls/puts (as of mid Oct 2021) doesn’t yield such high returns and wouldn’t bring you any where close to1.6%.

Have the markets changed so much or am i looking at it wrong?

Market has changed a lot over the course of this year. Volatility (VIX) has come down to 16.30 as of today. During the crash last year, VIX peaked at around 80. The historical level is between 11-16. When you consider the currentROC level as not interesting for selling covered calls, it is the normal market environment and return profile that you will be confronted with goingforward. You can better sell put and call spreads at the money with much higher ROC because in these cases you are selling at-the-money volatility which isthe highest point of volatility of any underlying. The put and call spread scanners are great tools to find such ATM trades. It is not easy to find ATM tradeswith high probability of success because it is a directional trade with high rewards. I do not trade any covered calls because ROC is low and you don’t want your patiently acquired stocks to be called away and after that the stocks moves another 5% without you owning it. Covered callsis easy to comprehend for beginners as a low risk strategy but doesn’t get you anywhere.

Thank you for this great S&P 500 trading strategy, looks like a great way to accelerate the returns of my SPY long term investment strategy.

Thank you for your kind words.

Please give this S&P 500 trading strategy a try and let me know your results.

Thank you for sharing a comparison of the wheel strategy vs buy and hold

I’ll be using the wheel strategy to improve the returns of my buy and hold stocks from now on

Please give the wheel strategy a try, you’ll love it

What is the characteristics for your billing we bands

You can sign up for our affiliate program to be a partner.

這個交易模式好適合選擇權新手試試看!

是啊,只要挑選波動不大的ETF或股票就可以搭配賣選擇權增加收入

Hi, interesting strategy. Have you the strategy backtest? If yes, what are the results?

Here is an interesting video from Tastytrade that backtested stock vs Puts, which should answer half of the equation.

https://www.tastytrade.com/shows/market-measures/episodes/puts-or-stock-07-09-2018

Thank’s for the link.

謝謝好文章篇分享,受益良多

Thank you for the tip

This sounds like a good strategy for MSFT

I definitely would like to own more MSFT stocks at a discount

You are right!

The Wheel Strategy is great for financially strong companies like MSFT and FAANG.

很好的操作模式,想進一步請教有那些股票是適合操作標的?

Hi,如文章提到的The Wheel Strategy主要是用賣期權的收入增加長期持有股票或ETF的投資報酬率

所以使用滾輪投資時建議使用在:

1.你願意長期持有的股票/ETF

2.波動不大的股票/ETF(以免大波動讓股價超越履約價太多,損失價差)

所以建議使用在FAANG等有競爭力又長期成長的優質股票

和S&P 500的ETF,例如VOO、IVV等

非常感謝!

How about TNA and SOXL?

Hi Simon, thank you for getting in touch.

Yes, I think TNA and SOXL are also good candidates for the Wheel Strategy, since they are ETFs that tend to be less volatile than individual stocks.

Their lower prices also mean you need less capital than SPY to execute the Wheel.