When we choose different options strategies to trade at different relative volatility, namely sell options at high IV, and buy options at low IV, we can use VIX to learn more about the market sentiments on volatility.

Today we’ll share with you how VIX works and alternate ways to hedge your portfolio with VIX.

What Is VIX?

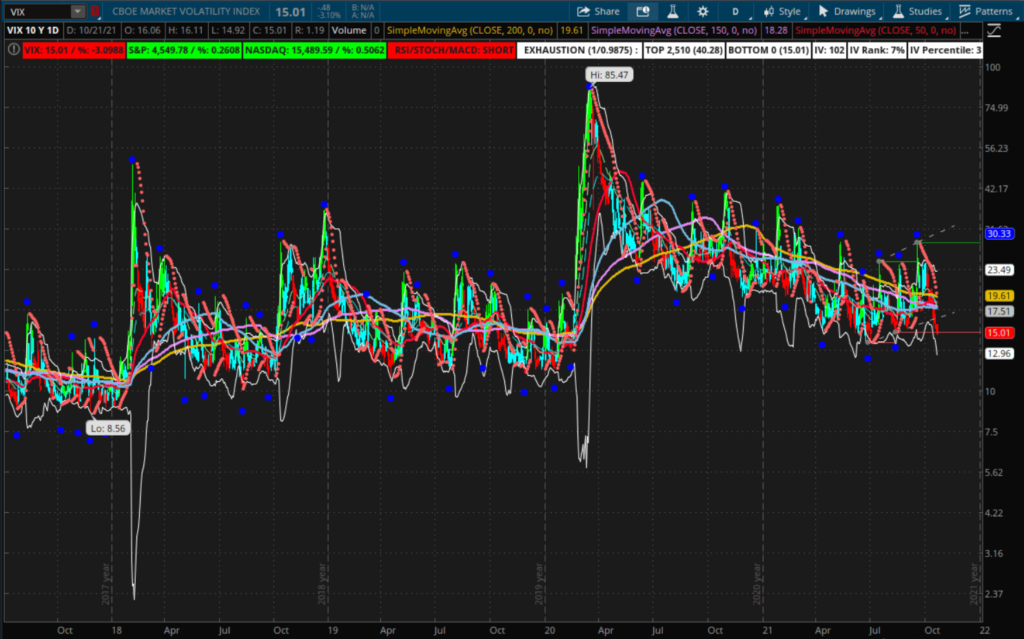

The VIX index was introduced in the early 90s, and it measures the near-term 30 days implied volatility or expected move, of the S&P 500 stocks.

It measures the expected annualised move from now till the expiration in 30 days calculated based on all SPX options prices. Since the SPX index is the largest stock market index in terms of aggregated market cap, globally every market participant uses the VIX as a measure of the volatility of the stock market as a whole. So VIX represents the SPX index annualised expected move for one standard deviation.

The VIX on 2021/10/21 is 15.01, which means the market expects a 68% probability (+/- 1 standard deviation of a normal distribution) that the S&P 500 will move within a range of +/- 15.01% in the next 12 months. With the SPX at 4549.78, it correlates to an expected movement between 3955.98 and 5232.70.

As the market generally expects the stock market to be bullish in the long run, when the SPX moves upward, the VIX will generally go down. But when the market crashes, the VIX will rise sharply, leading to the general feeling that VIX represents the fear index of the market.

Since its inception, the VIX has been moving in a range of 10 to 80, while staying between 11 and 20 most of the time. The 5-year average of VIX is at around 15, whereas the 30-year average is closer to 20.

Just before the 2020 crash, the market was moving at historically low volatilities, whereas in the 1990s the general volatility level was significantly higher.

There are weekly and monthly options available on the VIX that we can trade to profit from exploding or collapsing of volatility.

Unlike stocks where options can be settled in shares, VIX options are settled in cash. Holding VIX options to expiration will affect the cash balance of your account, without any assignment of shares.

Here at SlashTraders, we never hold options to expiration except when we sell Cash-Secured Puts to acquire shares at a discount.

Impact of Volatility on Neutral Options Strategies

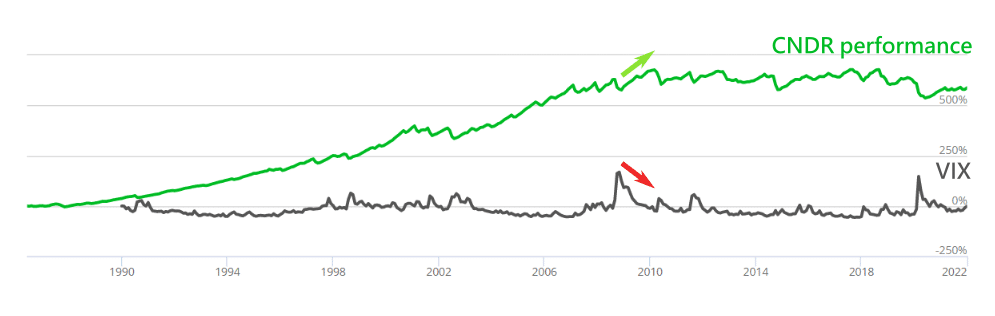

Given the advantages of Iron Condors, such as high premium and defined risks, it is tempting to trade a neutral options strategy all the time and benefit from the lack of price movements in the underlying.

The Cboe S&P 500 Iron Condor Index (CNDR) is the closest thing to answering how selling a 30-day expiration Iron Condor on the SPX would perform over time.

The CNDR index performed around 690% since its inception in 1986, while the S&P 500 generated a return of 5,500% in the same period.

This means an Iron Condor strategy isn't the best option strategy to increase S&P 500 returns over the long term.

If we compare the VIX with the performance of CNDR over time, we can see greater profitability in CNDR usually coincides with a reversion of high VIX to the mean.

Hence, we tend to only trade Iron Condors and Strangles after massive volatility spikes, before the volatility reverts to normal levels.

When to Enter VIX Hedging Positions

Since we see the VIX is inversely correlated to the S&P 500 index, when S&P 500 drops, VIX will increase sharply. During the 2020 crash, VIX jumped from 12 to 85; in 2009, it jumped from 16 to 90; and VIX went as high as 49 in both 1998 and 2001.

An advanced option Greek, vomma measures the sensitivity of vega, while VVIX does the same for VIX. Therefore, VVIX moves as a precursor to VIX. Whenever VVIX crosses above 20 on the RSI, exiting an oversold condition, we can enter a VIX hedging position.

On 2020/2/18, the VVIX crossed above the RSI 20 level and triggered a signal to go long on VIX at 16. As expected the VIX jumped to 23 on 2020/2/23.

Hedging With VIX Call Ratio Backspreads

If you want to use VIX options to hedge your portfolio, it is important to enter early, before the market crash and before the market expects a crash. If the underlying prices already reflect the expected move, then the hedge becomes ineffective.

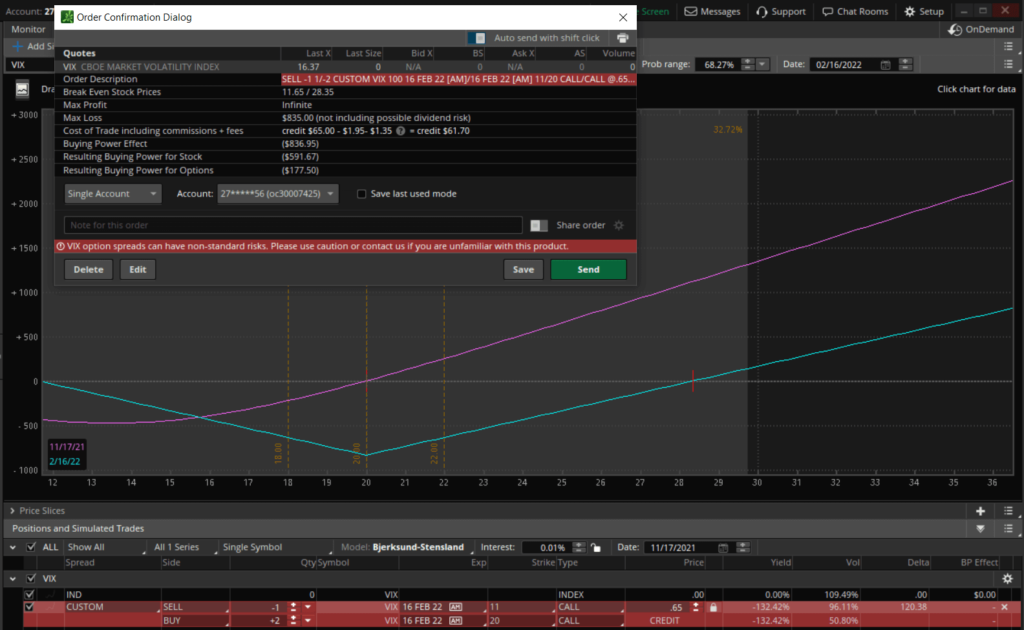

A great hedging strategy with VIX options is the Call Ratio Backspread:

- Sell 1 ATM Call contract.

- Buy 2 OTM Call contracts.

The strategy uses the short ATM Call to finance the cost of the long Calls. As a result, the strategy has a limited downside with unlimited upside.

The expiration of the Call Ratio Backspread is set 3-4 months away to provide sufficient coverage as you wait for a VIX expansion.

The trade gives us a net credit of about $60 and consumes about $840 of buying power. When the VIX crosses above 20, our long Call options kick in to generate profit.

| VIX | Profit from the Call Ratio Backspread |

|---|---|

| 40 | $1,350 |

| 60 | $2,800 |

| 80 | $4,800 |

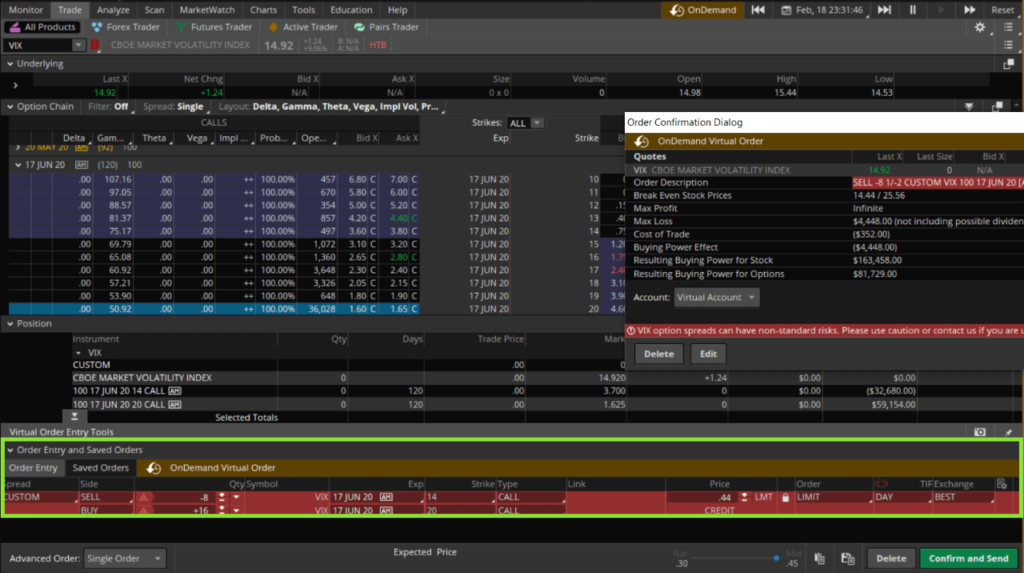

We can backtest the VIX options hedging strategy by entering 8 contracts of Call Ratio Backspreads on 2020/2/18.

The 8 contracts of VIX Call Ratio Backspread expiring on 2020/6/17 required $4,448 buying power with $352 credits received.

By 2020/3/20, the market crash would cause the VIX options hedge to earn $43,634 in profit.

Hedging With Long VIX Call Spreads

Alternatively, you could also buy VIX Call Spreads while VIX is at 15:

- Buy 1 Call at $20.

- Sell 1 Call at $40.

Even though the short Call at $40 could offset the cost of the long Call, the upside gain is capped. If VIX crosses beyond 40 or even skyrockets to 80, the strategy will miss out on those gains.

A long Call Spread also has less leverage than Call Ratio Backspreads, so you would need to open more trades at a net debit with higher transaction costs.

Therefore, we don’t suggest the usage of long Call Spreads for portfolio hedging. We’ll discuss an alternate way to hedging by VIX futures.

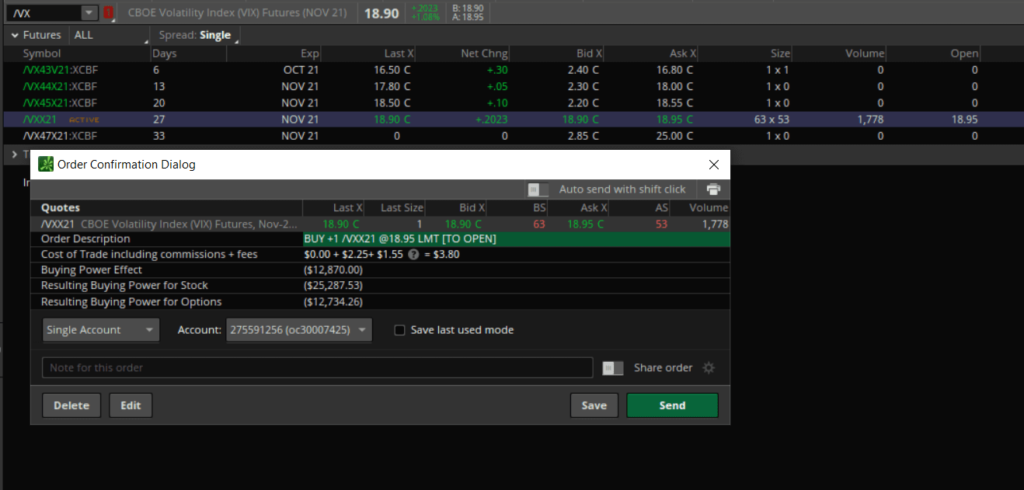

What Are VIX Futures?

The VIX futures (/VX) reflect the market expectation of the VIX value at a certain future point in time. The notional value of a VIX futures contract is $1000 for each 1 point. While the VIX is at 15.01, the VIX futures stand at 18.90, reflecting the market assumptions of where the VIX will be in the future. This means the market expects the volatility to increase to 18.90. It requires about $13,000 buying power to buy a single contract at this time.

VIX futures are usually traded in contango, which means longer-dated futures contracts trade at a higher price. It means the further we go out in time, the more likely a surge of volatility is to happen.

On rare occasions, VIX futures may trade in backwardation, with longer-dated contracts trading at a lower price. It usually happens after market crashes like in 2008 or 2020, when volatility spiked to 30-80. Then the market would expect the volatility to revert to its historical mean of 11-20 range afterwards.

We believe VIX futures should not be held to expiration but rolled into the next expiration cycle just like VIX options.

Hedging With VIX Futures

If we buy a /VX contract while VIX is 15, the buying power required is $13,000, with a notional value of $15,000. When the market crash leads to the VIX expanding to 40, the notional value of the /VX contract expands to $40,000, leading to a profit of $25,000.

Similar VIX futures with 1/10 the contract size are also available as the VIX mini futures (/VXM), which allows traders with smaller accounts to participate in VIX futures trading.

As in the case of VIX hedging with options, you should buy /VX futures with 3 months to maturity for the best protection.

Hedging With VIX-Correlated Asset Classes

In finance, we describe the offset between different asset classes as arbitrage, and the relationships between related asset classes as either positive or negative correlation with each other.Naturally, people would argue that gold (GLD) has an inverse relationship to market crashes. However, GLD doesn’t have a strong correlation with the S&P 500.

To protect our portfolio, we need a hedge that both correlates with S&P 500 and kicks in in a timely fashion as well, such as the forex pairing of AUDJPY. The global forex market is about ten times larger than all stock markets combined, and allows large financial institutions to park their money in times of market turmoil.

The Japanese Yen is considered a safe haven currency and sees a large inflow of money during market crashes. It is also dubbed as a risk-off currency. The Australian dollar is largely backed by the country’s wealth of natural resources highly demanded during global economic growth and despised in recessions.

Currency pairs reflect the strength ratio of the two countries. When the market crashes, the AUD/JPY currency pair becomes stressed on both sides, causing it to perform large long-lasting cyclical moves. On 2020/1/20 the AUD/JPY pair triggered a short signal at 75.50 and moved down to 60 by 2020/3/20, for 1550 pips.

We could use a buying power of $8000 to short the AUD/JPY on 2020/1/20 and risk 1% ($80 or AUD 120) to hedge our investment. If we caught 80% of the 1550 pip move by 2020/3/20, around 1240 pips, the short on AUD/JPY would profit $80 x 1240 = $99,200.

If we risked 3% instead, the short AUD/JPY would make $297,600 by 2020/3/20.

We like to use AUD/JPY as a hedge because not only does it make money when the market falls heavily, it is very responsive to the moves of the S&P 500, and it doesn’t require as precise timing as with VIX options.

Even though delta hedging strategies provide simple protection that requires fewer adjustments, but they have a few drawbacks that lead to higher cost of trade:

- Theta decays the delta hedging options.

- If the market moves sideways for a long period, we will not benefit from gamma offsetting theta decay, causing our Put options to expire worthless at a loss.

Therefore, they are particularly suited when the market is extremely overvalued and approaching a market top.

While VIX-based strategies are cheaper to execute, they require almost perfect timing to execute, which makes them difficult to handle.

SlashTraders vs S&P 500: 450% Outperformance, Verified Trades and How to Copy Every Alert

Hi, I would like to ask if I change to sell put spread to see if the VIX is not below a certain value, how does it compare to call ratio back spread? Or is it because the latter will have one more call contract so that the maximum profit is not limited? Thank you!

You can also sell Put spread, which requires less buying power and lower risk.

In the first scenario, if the VIX rises much higher than the Short call strike of $11, does it trigger an assign and if it is assigned, it's a loss not a profit

No, because the first option is a VIX Call Ratio Backspread.

It's Short Call x1.

Buy Call x2

If the VIX rises much higher than the Short call strike of $11, the Buy Call x2 contract will be very profitable!

If it is much higher than 11, will there be a situation where the short call will be exercised in the night session, before and after the market? After being exercised, the price fell back to 11 immediately before reaching the middle of the trading session, the 2 long calls are not in the middle of the trading session and can not be traded, if you want to exercise the right to exercise in the night session and before and after the trading session can not be exercised? If it must be in the middle of the trading session to exercise the right, or after the exercise of the right only with the opening price of the trading session, then this is not a loss of protection?

Suggest that the cut-off time for the options be lengthened.

If there is a long time to go before the deadline, the chance of early exercise is very low.

Thank you for the detailed explanation about how to trade VIX

You're welcome

Thanks for sharing the VIX hedge trade!

Recently, it seems that the U.S. stock market is going to start to fall, and I came across this VIX hedging article just in time.

That's right, a hedging strategy that uses the VIX can provide peace of mind when the stock market goes down.