When trading options for profit, a rule of thumb is to sell options when the Implied Volatility is high, and buy options when the IV is lower.

But do you know what market volatility represents in general and how differences in volatility can affect options prices?

In this article, we'll try to provide an in-depth explanation of what market volatility is, because a solid understanding of volatility is important to trading options for consistent income. We also share the differences between Historical Volatility (HV) and Implied Volatility (IV).

What Is Volatility?

Volatility is the fluctuations and dispersion of data points, and we can use it to indicate the fluctuation of stock prices in the market. Mathematically speaking, volatility is the deviation of the data dispersion.

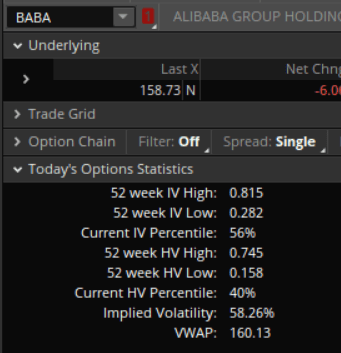

Thinkorswim shares various market volatility data in the Options Statistics. The most important of them all are Historical Volatility (HV) and Implied Volatility (IV).

What Are the Differences Between HV and IV?

HV is the backward-looking volatility of the underlying, while IV is forward-looking for the theoretically expected future moves.

How to Calculate Historical Volatility?

In case you have left your high school years long behind you, we’ll take it step by step through the process of calculating volatility.

We calculated the volatility of the stock price with reference to a series of recent BABA closing prices. Volatility calculated using historical data is commonly referred to as historical volatility (HV).

We first calculate the daily changes of 10 recent BABA closing prices.

| Trading days | Last | Daily change |

|---|---|---|

| 10/4 | 139.63 | |

| 10/5 | 143.14 | 2.5% |

| 10/6 | 144.10 | 0.7% |

| 10/7 | 156.00 | 8.3% |

| 10/8 | 161.52 | 3.5% |

| 10/11 | 163.95 | 1.5% |

| 10/12 | 163.00 | -0.6% |

| 10/13 | 167.40 | 2.7% |

| 10/14 | 166.78 | -0.4% |

| 10/15 | 168.00 | 0.7% |

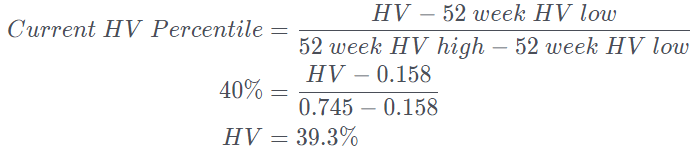

The standard deviation of these 10 daily changes is 2.54%

Since there are around 252 trading days each year, we can transform the 2.54% standard deviation into an annualised number of 40.3%, which is HV.

Then we can compare our HV number with the Thinkorswim HV data.

We deduce the Thinkorswim HV from the HV Percentile formula to get a similar number to our calculated HV.

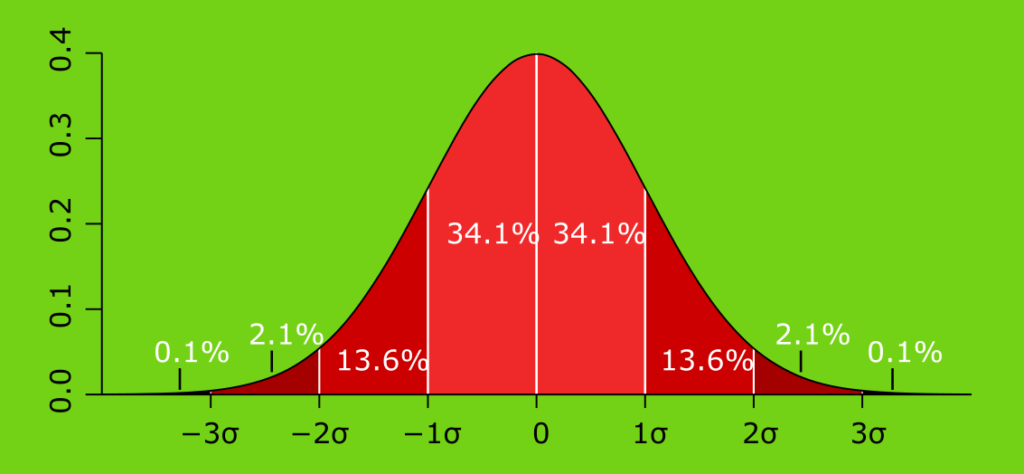

The famous Gaussian normal distribution describes the random outcomes of a data set in our real world where 50% of all outcomes fall on the left side of the mean and the other 50% on the right side of the mean.

1 standard deviation (σ) on either side of the mean mark the range in which 68% of all fluctuations of the given process would fall. While +/-2σ mark the probability of 95%.

The current closing price for BABA is $158.73, while HV is 40%. So we have a 68% confidence that BABA closing prices will stay within $95.24 and $222.22 in the following year.

If BABA’s closing prices fluctuated more with a bigger standard deviation, its HV would be high.

If the closing prices fluctuated less with a smaller standard deviation, the HV would be low.

How Does IV Affect Options Prices?

Option prices are a function of IV, which is the expected move of the underlying. IV is also calculated from the options pricing model.

Options provide us with rights to sell or buy an asset at a certain price. Such right is inherently associated with a certain cash inflow or outflow and has to be discounted by interest and dividends.

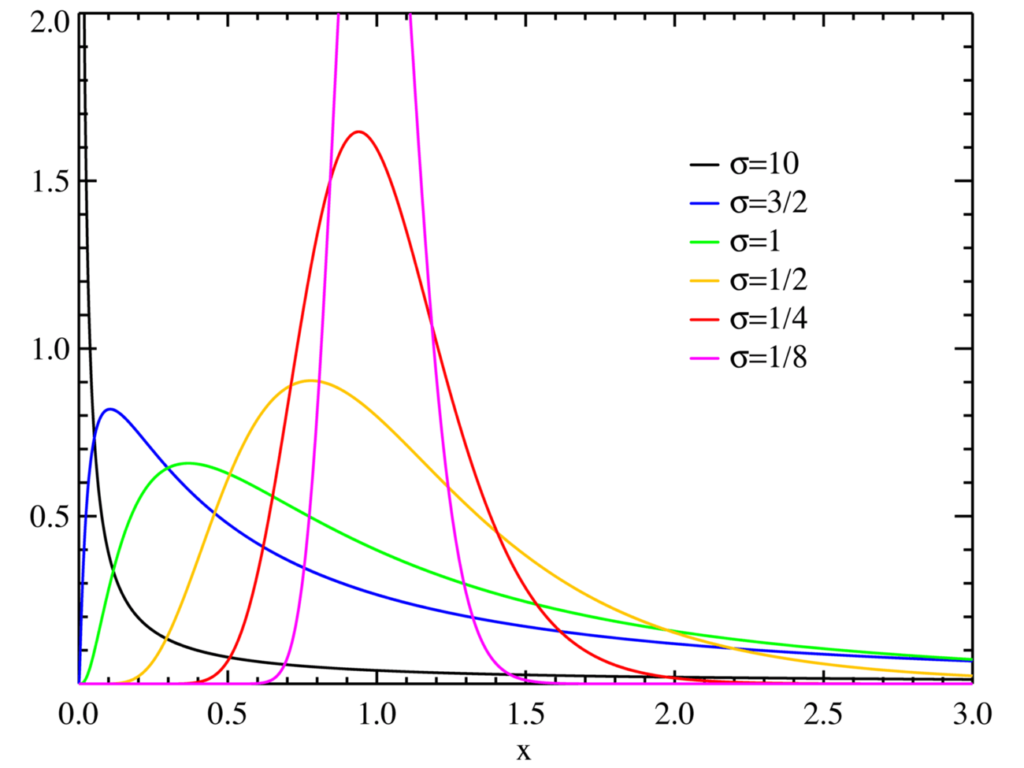

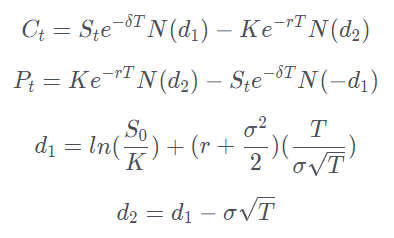

The famous Black Scholes option pricing model was rewarded with a Nobel Prize and provides us with a set of elaborate formulas that allows us to calculate Call and Put option prices. It uses a log-normal distribution model because the price can't go lower than 0, and has a long tail as prices approach infinity.

Call and Put option prices are calculated as follows:

- σ = IV

- δ = dividends

- S = stock price

- K = strike price

- r = risk-free interest rate

- T = time to expiration (year)

- N = normal distribution

- N(d1) = the expected value of cash/stock inflow if option expires ITM

- N(d2) = the probability the option expires ITM

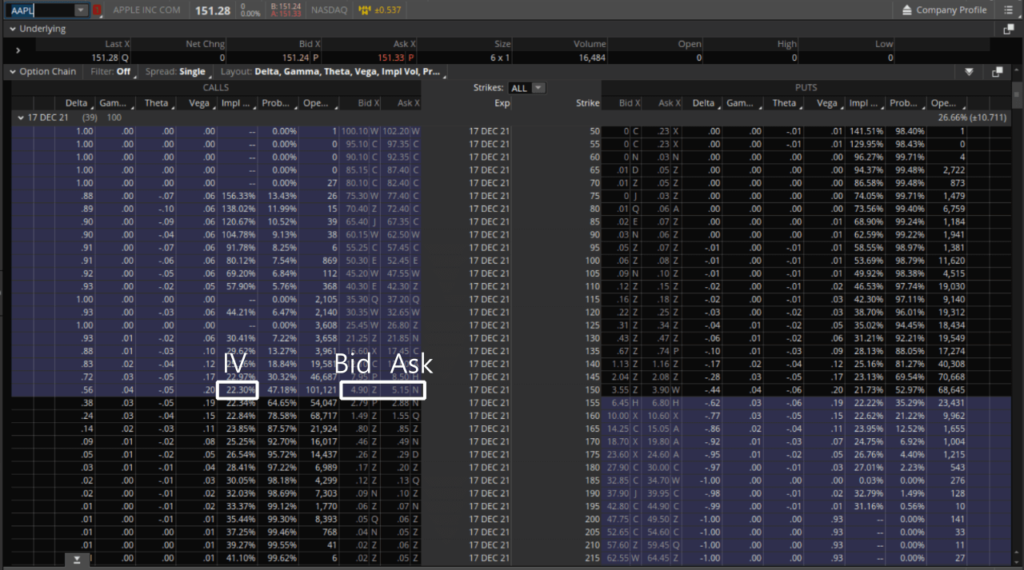

We used the AAPL stock price as an example to calculate the Call for price parity $150, 39 days after cutoff, and used Thinkorswim's option chain to validate our calculations.

- σ = 22.38%

- S = $151.28

- K = $150

- r = 0.04%

- t = 39/365 = 0.106849

- d1 = 0.153314

- d2 = 0.080158

- N(d1) = 0.56

- N(d2) = 0.53

- C(39) = $5.05

As you may notice, the calculated option price of $5.05 is between the bid price of $4.90 and the ask price of $5.15 shown in Thinkorswim.

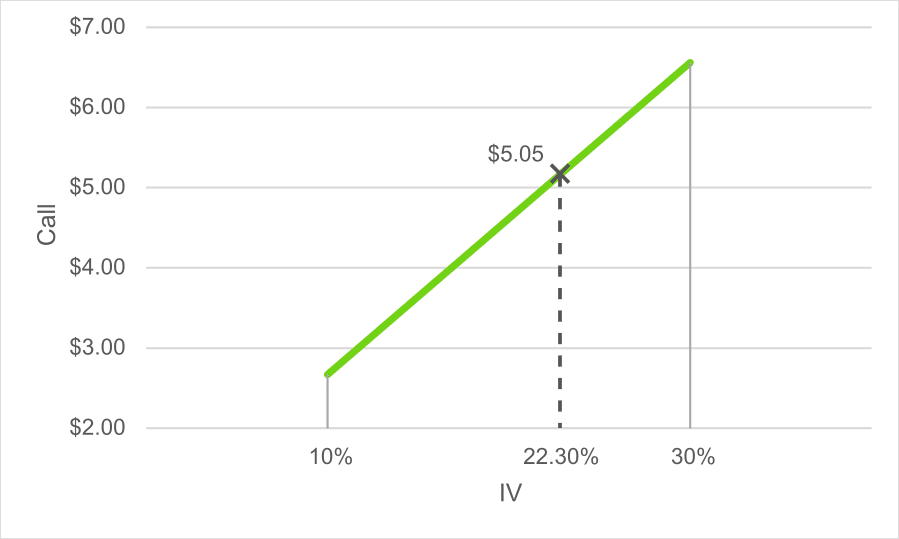

So IV and option prices, which comes first?

The Market Maker collects all order flows from brokers, such as TD Ameritrade, Firstrade, Interactive Brokers, then derive ATM option prices based on the increase and decrease of supply and demand for Put and Call options as well as the underlying itself.

Once, you have the ATM options price, you can calculate the IV based on the option pricing model. We have to do some trial and error to approximate the IV value to match the AAPL Call price.

| IV | Call prices |

|---|---|

| 10% | 2.67 |

| 30% | 6.56 |

| 50% | 10.47 |

| 70% | 14.37 |

| 90% | 18.27 |

We see the IV between 10%-30% give results closest to $5.05.

We interpolate the IV between 10% and 30% to find the correct IV as 22.30%, which is the market expectation of future price moves.

Stocks With the Highest IV

| Symbol | IV | IV Perc | IV Rank | Total Options Volume | Call Options Volume | Put Options Volume | Open Interest | Days To/Since Earnings | Earnings Date | ||

|---|---|---|---|---|---|---|---|---|---|---|---|

| AA | 53% | 26% | 27% | 14,181 | 8,097 | 6,084 | 165,390 | 76 | 2026-10-21 | 2026-10-16 | 2026-08-06 |

| AAPL | 28% | 67% | 1% | 1,596,069 | 1,172,119 | 423,950 | 4,261,968 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| ABBV | 30% | 56% | 9% | 14,726 | 7,723 | 7,003 | 194,656 | 78 | 2026-10-23 | 2026-10-16 | 2026-08-06 |

| ABNB | 59% | 92% | 65% | 9,450 | 4,777 | 4,673 | 101,577 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| ABT | 30% | 71% | 0% | 4,354 | 2,452 | 1,902 | 107,721 | 76 | 2026-10-21 | 2026-10-16 | 2026-08-06 |

| ABVX | 71% | 20% | 99% | 7,025 | 6,229 | 796 | 61,751 | 46 | 2026-09-21 | 2026-10-16 | 2026-08-06 |

| ACI | 41% | 55% | 100% | 2,839 | 1,899 | 940 | 67,490 | 75 | 2026-10-20 | 2026-10-16 | 2026-08-06 |

| ACN | 67% | 94% | 3% | 8,364 | 3,806 | 4,558 | 108,812 | 56 | 2026-10-01 | 2026-10-16 | 2026-08-06 |

| ADBE | 53% | 82% | 48% | 31,754 | 21,821 | 9,933 | 389,313 | 35 | 2026-09-10 | 2026-10-16 | 2026-08-06 |

| ADM | 37% | 63% | 97% | 3,975 | 2,935 | 1,040 | 40,308 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| AEM | 68% | 98% | 78% | 13,580 | 9,225 | 4,355 | 90,795 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| AFRM | 69% | 48% | 30% | 14,733 | 7,988 | 6,745 | 108,850 | 14 | 2026-08-20 | 2026-10-16 | 2026-08-06 |

| AG | 79% | 44% | 41% | 62,064 | 51,020 | 11,044 | 764,373 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| ALAB | 121% | 85% | 57% | 48,740 | 32,377 | 16,363 | 134,514 | 96 | 2026-11-10 | 2026-10-16 | 2026-08-06 |

| ALB | 74% | 85% | 61% | 7,820 | 4,161 | 3,659 | 45,553 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| ALK | 62% | 52% | 3% | 14,494 | 14,112 | 382 | 49,026 | 70 | 2026-10-15 | 2026-10-16 | 2026-08-06 |

| AMAT | 97% | 94% | 0% | 30,103 | 17,402 | 12,701 | 239,138 | 7 | 2026-08-13 | 2026-10-16 | 2026-08-06 |

| AMD | 71% | 72% | 86% | 1,031,822 | 568,227 | 463,595 | 2,430,792 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| AMGN | 42% | 97% | 71% | 19,622 | 10,865 | 8,757 | 76,867 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| AMPX | 111% | 50% | 97% | 21,272 | 18,759 | 2,513 | 180,220 | 91 | 2026-11-05 | 2026-10-16 | 2026-08-06 |

| AMT | 28% | 35% | 100% | 5,677 | 3,194 | 2,483 | 38,487 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| AMZN | 35% | 67% | 32% | 1,043,325 | 627,790 | 415,535 | 4,367,873 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| ANET | 65% | 73% | 42% | 83,681 | 58,407 | 25,274 | 262,323 | 88 | 2026-11-02 | 2026-10-16 | 2026-08-06 |

| APA | 57% | 73% | 49% | 10,527 | 8,910 | 1,617 | 65,719 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| APH | 51% | 60% | 1% | 8,237 | 5,727 | 2,510 | 73,080 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| APLD | 97% | 14% | 28% | 39,682 | 31,543 | 8,139 | 522,818 | 69 | 2026-10-14 | 2026-10-16 | 2026-08-06 |

| APO | 38% | 27% | 26% | 5,791 | 1,523 | 4,268 | 73,815 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| ARM | 92% | 76% | 58% | 57,040 | 33,166 | 23,874 | 370,352 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| ASML | 63% | 90% | 67% | 13,553 | 6,851 | 6,702 | 67,246 | 69 | 2026-10-14 | 2026-10-16 | 2026-08-06 |

| ASST | 88% | 2% | 91% | 4,846 | 3,332 | 1,514 | 458,362 | 27 | 2026-09-02 | 2026-10-16 | 2026-08-06 |

| ASTS | 117% | 73% | 57% | 131,685 | 94,556 | 37,129 | 904,917 | 4 | 2026-08-10 | 2026-10-16 | 2026-08-06 |

| AU | 62% | 49% | 32% | 5,138 | 3,764 | 1,374 | 32,879 | 91 | 2026-11-05 | 2026-10-16 | 2026-08-06 |

| AVGO | 51% | 64% | 33% | 226,613 | 125,214 | 101,399 | 1,535,601 | 27 | 2026-09-02 | 2026-10-16 | 2026-08-06 |

| AVTR | 59% | 27% | 11% | 960 | 622 | 338 | 119,063 | 78 | 2026-10-23 | 2026-10-16 | 2026-08-06 |

| AXP | 24% | 11% | 21% | 10,092 | 3,955 | 6,137 | 135,081 | 78 | 2026-10-23 | 2026-10-16 | 2026-08-06 |

| AZN | 33% | 69% | 94% | 13,289 | 11,112 | 2,177 | 55,932 | 85 | 2026-10-30 | 2026-10-16 | 2026-08-06 |

| B | 67% | 98% | 100% | 36,252 | 28,590 | 7,662 | 570,008 | 4 | 2026-08-10 | 2026-10-16 | 2026-08-06 |

| BA | 42% | 94% | 82% | 94,151 | 53,227 | 40,924 | 620,341 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| BABA | 46% | 56% | 47% | 87,847 | 59,835 | 28,012 | 1,476,815 | 22 | 2026-08-28 | 2026-10-16 | 2026-08-06 |

| BAC | 24% | 33% | 0% | 68,790 | 38,978 | 29,812 | 1,251,886 | 69 | 2026-10-14 | 2026-10-16 | 2026-08-06 |

| BE | 124% | 62% | 38% | 108,473 | 28,542 | 79,931 | 838,375 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| BIDU | 55% | 65% | 48% | 22,662 | 14,134 | 8,528 | 188,871 | 12 | 2026-08-18 | 2026-10-16 | 2026-08-06 |

| BILI | 70% | 77% | 51% | 3,594 | 2,804 | 790 | 55,017 | 7 | 2026-08-13 | 2026-10-16 | 2026-08-06 |

| BKNG | 42% | 66% | 40% | 38,253 | 23,605 | 14,648 | 261,708 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| BKR | 58% | 77% | 98% | 790 | 658 | 132 | 35,662 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| BMY | 29% | 36% | 30% | 27,409 | 14,235 | 13,174 | 512,470 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| BP | 35% | 73% | 10% | 19,135 | 12,249 | 6,886 | 304,518 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| BRK-B | 17% | 58% | 54% | 19,380 | 10,566 | 8,814 | 296,052 | 2026-10-16 | 2026-08-06 | ||

| BROS | 95% | 93% | 100% | 7,209 | 4,529 | 2,680 | 34,030 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| BX | 42% | 52% | 94% | 17,467 | 4,602 | 12,865 | 252,147 | 70 | 2026-10-15 | 2026-10-16 | 2026-08-06 |

| C | 30% | 36% | 0% | 39,258 | 25,949 | 13,309 | 541,147 | 68 | 2026-10-13 | 2026-10-16 | 2026-08-06 |

| CART | 87% | 98% | 52% | 1,645 | 1,086 | 559 | 47,500 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| CAT | 49% | 88% | 58% | 33,100 | 16,620 | 16,480 | 181,837 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| CAVA | 89% | 92% | 59% | 13,225 | 2,924 | 10,301 | 68,689 | 5 | 2026-08-11 | 2026-10-16 | 2026-08-06 |

| CBRS | 129% | 75% | 53% | 14,360 | 8,430 | 5,930 | 135,336 | 6 | 2026-08-12 | 2026-10-16 | 2026-08-06 |

| CC | 80% | 52% | 100% | 40,812 | 37,199 | 3,613 | 60,316 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| CCJ | 58% | 46% | 30% | 25,054 | 20,953 | 4,101 | 290,087 | 85 | 2026-10-30 | 2026-10-16 | 2026-08-06 |

| CCL | 45% | 37% | 0% | 30,166 | 15,778 | 14,388 | 743,624 | 42 | 2026-09-17 | 2026-10-16 | 2026-08-06 |

| CELH | 112% | 97% | 86% | 49,282 | 35,190 | 14,092 | 437,393 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| CHTR | 85% | 88% | 52% | 4,608 | 2,276 | 2,332 | 75,346 | 85 | 2026-10-30 | 2026-10-16 | 2026-08-06 |

| CHWY | 82% | 94% | 69% | 9,424 | 7,066 | 2,358 | 155,412 | 27 | 2026-09-02 | 2026-10-16 | 2026-08-06 |

| CI | 37% | 62% | 4% | 2,650 | 1,777 | 873 | 39,161 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| CIFR | 131% | 81% | 48% | 137,836 | 122,384 | 15,452 | 1,151,101 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| CLF | 81% | 81% | 0% | 89,513 | 37,832 | 51,681 | 552,617 | 81 | 2026-10-26 | 2026-10-16 | 2026-08-06 |

| CLS | 90% | 77% | 54% | 4,495 | 1,795 | 2,700 | 54,924 | 81 | 2026-10-26 | 2026-10-16 | 2026-08-06 |

| CLX | 48% | 87% | 0% | 4,753 | 1,294 | 3,459 | 86,451 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| CMCSA | 39% | 67% | 3% | 36,726 | 23,257 | 13,469 | 512,927 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| CNC | 44% | 15% | 0% | 10,518 | 5,040 | 5,478 | 106,019 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| CNQ | 43% | 86% | 84% | 2,782 | 1,909 | 873 | 77,146 | -1 | 2026-08-05 | 2026-10-16 | 2026-08-06 |

| COHR | 126% | 96% | 88% | 18,998 | 8,507 | 10,491 | 135,695 | 6 | 2026-08-12 | 2026-10-16 | 2026-08-06 |

| COIN | 73% | 65% | 44% | 79,391 | 48,154 | 31,237 | 590,065 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| COP | 42% | 94% | 59% | 11,915 | 7,020 | 4,895 | 162,738 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| COPX | 48% | 37% | 49% | 13,927 | 8,517 | 5,410 | 193,096 | 2026-10-16 | 2026-08-06 | ||

| COST | 25% | 72% | 41% | 36,906 | 18,011 | 18,895 | 185,236 | 49 | 2026-09-24 | 2026-10-16 | 2026-08-06 |

| CRCL | 95% | 71% | 49% | 102,219 | 66,272 | 35,947 | 576,384 | 104 | 2026-11-18 | 2026-10-16 | 2026-08-06 |

| CRDO | 126% | 90% | 64% | 20,175 | 11,185 | 8,990 | 115,975 | 34 | 2026-09-09 | 2026-10-16 | 2026-08-06 |

| CRM | 54% | 85% | 97% | 42,410 | 22,712 | 19,698 | 767,935 | 27 | 2026-09-02 | 2026-10-16 | 2026-08-06 |

| CRSP | 75% | 70% | 45% | 4,934 | 3,954 | 980 | 36,666 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| CRWD | 57% | 73% | 43% | 53,539 | 28,500 | 25,039 | 572,114 | 20 | 2026-08-26 | 2026-10-16 | 2026-08-06 |

| CRWV | 114% | 84% | 48% | 122,345 | 65,268 | 57,077 | 1,774,925 | 5 | 2026-08-11 | 2026-10-16 | 2026-08-06 |

| CSCO | 56% | 97% | 97% | 42,250 | 27,606 | 14,644 | 576,487 | 13 | 2026-08-19 | 2026-10-16 | 2026-08-06 |

| CSIQ | 111% | 67% | 74% | 3,931 | 1,270 | 2,661 | 64,011 | 21 | 2026-08-27 | 2026-10-16 | 2026-08-06 |

| CVE | 56% | 74% | 56% | 3,002 | 2,720 | 282 | 46,442 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| CVX | 29% | 61% | 30% | 46,521 | 28,715 | 17,806 | 407,494 | 78 | 2026-10-23 | 2026-10-16 | 2026-08-06 |

| D | 24% | 33% | 25% | 2,160 | 1,849 | 311 | 42,663 | 85 | 2026-10-30 | 2026-10-16 | 2026-08-06 |

| DAX | -1% | 0% | 0% | 3 | 2 | 1 | 0 | 2026-10-16 | 2026-08-06 | ||

| DBX | 143% | 99% | 5% | 1,514 | 804 | 710 | 34,739 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| DDOG | 123% | 99% | 91% | 57,361 | 25,084 | 32,277 | 128,832 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| DELL | 97% | 99% | 79% | 94,200 | 45,576 | 48,624 | 302,412 | 28 | 2026-09-03 | 2026-10-16 | 2026-08-06 |

| DHT | 53% | 46% | 0% | 21,746 | 20,709 | 1,037 | 36,854 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| DIA | 14% | 46% | 24% | 95,286 | 49,290 | 45,996 | 279,276 | 2026-10-16 | 2026-08-06 | ||

| DIS | 28% | 51% | 99% | 95,541 | 66,348 | 29,193 | 614,033 | 98 | 2026-11-12 | 2026-10-16 | 2026-08-06 |

| DLO | 89% | 71% | 3% | 549 | 448 | 101 | 70,218 | 7 | 2026-08-13 | 2026-10-16 | 2026-08-06 |

| DOCN | 98% | 61% | 9% | 7,847 | 4,628 | 3,219 | 47,146 | 95 | 2026-11-09 | 2026-10-16 | 2026-08-06 |

| DOW | 44% | 18% | 54% | 10,011 | 5,566 | 4,445 | 262,707 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| DUK | 29% | 69% | 100% | 4,158 | 3,175 | 983 | 49,145 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| DVA | 39% | 45% | 96% | 29,672 | 24,521 | 5,151 | 32,461 | 78 | 2026-10-23 | 2026-10-16 | 2026-08-06 |

| DVN | 46% | 84% | 99% | 21,658 | 14,212 | 7,446 | 373,995 | 96 | 2026-11-10 | 2026-10-16 | 2026-08-06 |

| EBAY | 82% | 99% | 97% | 24,033 | 12,742 | 11,291 | 40,865 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| ECHO | 68% | 52% | 34% | 13,256 | 7,688 | 5,568 | 293,794 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| EEM | 32% | 69% | 0% | 45,354 | 15,530 | 29,824 | 2,206,575 | 2026-10-16 | 2026-08-06 | ||

| EFA | 20% | 66% | 32% | 8,760 | 4,012 | 4,748 | 317,634 | 2026-10-16 | 2026-08-06 | ||

| EGO | 113% | 97% | 80% | 3,381 | 2,825 | 556 | 37,052 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| EIDO | 15% | 11% | 99% | 25 | 2 | 23 | 0 | 2026-10-16 | 2026-08-06 | ||

| EIX | 40% | 68% | 0% | 6,116 | 3,613 | 2,503 | 45,552 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| EL | 53% | 60% | 30% | 2,735 | 1,167 | 1,568 | 32,867 | 13 | 2026-08-19 | 2026-10-16 | 2026-08-06 |

| ELF | 127% | 98% | 91% | 19,863 | 10,399 | 9,464 | 100,200 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| ENB | 22% | 27% | 99% | 3,590 | 2,089 | 1,501 | 36,448 | 85 | 2026-10-30 | 2026-10-16 | 2026-08-06 |

| ENPH | 95% | 75% | 55% | 20,184 | 14,649 | 5,535 | 261,393 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| EOG | 45% | 92% | 48% | 12,504 | 5,136 | 7,368 | 64,943 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| EQNR | 47% | 72% | 0% | 3,325 | 247 | 3,078 | 52,841 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| EQX | 163% | 92% | 93% | 42,446 | 29,488 | 12,958 | 146,946 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| ERAS | 115% | 24% | 23% | 497 | 347 | 150 | 44,491 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| ERO | 113% | 69% | 86% | 8,644 | 8,229 | 415 | 73,084 | 96 | 2026-11-10 | 2026-10-16 | 2026-08-06 |

| ET | 25% | 51% | 0% | 40,742 | 38,696 | 2,046 | 705,375 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| ETN | 50% | 85% | 46% | 14,206 | 3,666 | 10,540 | 44,381 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| ETSY | 122% | 99% | 41% | 35,705 | 21,315 | 14,390 | 69,222 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| EWJ | 29% | 67% | 44% | 4,382 | 2,942 | 1,440 | 11,301 | 2026-10-16 | 2026-08-06 | ||

| EWM | 4 | 4 | 0 | 2 | 2026-10-16 | 2026-08-06 | |||||

| EWY | 79% | 76% | 62% | 117,840 | 29,747 | 88,093 | 895,588 | 2026-10-16 | 2026-08-06 | ||

| EWZ | 30% | 53% | 15% | 90,093 | 68,610 | 21,483 | 2,398,873 | 2026-10-16 | 2026-08-06 | ||

| EXE | 41% | 54% | 20% | 7,773 | 5,269 | 2,504 | 94,294 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| EZA | 57% | 52% | 0% | 12 | 1 | 11 | 1 | 2026-10-16 | 2026-08-06 | ||

| F | 42% | 65% | 0% | 46,951 | 31,902 | 15,049 | 1,306,583 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| FCEL | 153% | 30% | 23% | 8,758 | 6,743 | 2,015 | 90,485 | 33 | 2026-09-08 | 2026-10-16 | 2026-08-06 |

| FCX | 60% | 86% | 76% | 105,791 | 79,048 | 26,743 | 814,472 | 70 | 2026-10-15 | 2026-10-16 | 2026-08-06 |

| FIG | 151% | 98% | 100% | 102,660 | 64,156 | 38,504 | 399,616 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| FIVN | 89% | 49% | 38% | 1,510 | 1,281 | 229 | 53,345 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| FLEX | 93% | 91% | 46% | 1,453 | 670 | 783 | 37,393 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| FLR | 88% | 92% | 67% | 9,118 | 8,291 | 827 | 55,284 | 1 | 2026-08-07 | 2026-10-16 | 2026-08-06 |

| FMC | 167% | 92% | 100% | 2,420 | 1,972 | 448 | 40,271 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| FOUR | 102% | 85% | 17% | 2,970 | 1,798 | 1,172 | 36,871 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| FSLR | 99% | 98% | 92% | 28,867 | 18,776 | 10,091 | 282,213 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| FTNT | 52% | 72% | 30% | 7,658 | 4,232 | 3,426 | 71,564 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| FXI | 26% | 57% | 15% | 94,347 | 31,897 | 62,450 | 1,637,445 | 2026-10-16 | 2026-08-06 | ||

| GDX | 43% | 37% | 38% | 518,774 | 239,414 | 279,360 | 1,715,545 | 2026-10-16 | 2026-08-06 | ||

| GE | 35% | 51% | 35% | 10,349 | 4,542 | 5,807 | 128,603 | 75 | 2026-10-20 | 2026-10-16 | 2026-08-06 |

| GEV | 64% | 86% | 55% | 9,675 | 3,742 | 5,933 | 94,754 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| GFI | 53% | 17% | 98% | 14,971 | 13,197 | 1,774 | 37,145 | 19 | 2026-08-25 | 2026-10-16 | 2026-08-06 |

| GFS | 49% | 10% | 96% | 9,535 | 7,993 | 1,542 | 78,262 | 96 | 2026-11-10 | 2026-10-16 | 2026-08-06 |

| GILD | 34% | 60% | 32% | 18,184 | 11,685 | 6,499 | 123,069 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| GIS | 62% | 91% | 1% | 8,902 | 3,006 | 5,896 | 129,024 | 48 | 2026-09-23 | 2026-10-16 | 2026-08-06 |

| GLD | 23% | 66% | 32% | 564,472 | 414,944 | 149,528 | 2,800,130 | 2026-10-16 | 2026-08-06 | ||

| GLW | 82% | 78% | 13% | 31,437 | 17,497 | 13,940 | 432,112 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| GLXY | 109% | 75% | 16% | 72,744 | 45,937 | 26,807 | 345,146 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| GME | 47% | 51% | 32% | 119,813 | 86,168 | 33,645 | 1,390,018 | 34 | 2026-09-09 | 2026-10-16 | 2026-08-06 |

| GOOG | 39% | 83% | 41% | 317,712 | 209,495 | 108,217 | 1,469,330 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| GOOGL | 33% | 54% | 31% | 941,463 | 580,044 | 361,419 | 2,655,926 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| GPN | 43% | 25% | 0% | 4,020 | 1,290 | 2,730 | 50,824 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| GRPN | 133% | 85% | 100% | 10,882 | 10,713 | 169 | 61,349 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| GS | 39% | 84% | 65% | 31,732 | 16,066 | 15,666 | 200,095 | 68 | 2026-10-13 | 2026-10-16 | 2026-08-06 |

| GTLB | 85% | 73% | 33% | 2,482 | 1,937 | 545 | 59,629 | 33 | 2026-09-08 | 2026-10-16 | 2026-08-06 |

| GXO | 61% | 77% | 100% | 11,376 | 8,073 | 3,303 | 32,034 | 96 | 2026-11-10 | 2026-10-16 | 2026-08-06 |

| HAL | 38% | 35% | 43% | 9,841 | 4,209 | 5,632 | 256,142 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| HD | 38% | 96% | 0% | 14,182 | 8,690 | 5,492 | 143,625 | 12 | 2026-08-18 | 2026-10-16 | 2026-08-06 |

| HIMS | 111% | 88% | 56% | 46,182 | 23,784 | 22,398 | 616,983 | 4 | 2026-08-10 | 2026-10-16 | 2026-08-06 |

| HOOD | 66% | 46% | 33% | 147,640 | 99,695 | 47,945 | 1,223,033 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| HPQ | 60% | 90% | 2% | 45,557 | 10,258 | 35,299 | 280,358 | 26 | 2026-09-01 | 2026-10-16 | 2026-08-06 |

| HUT | 154% | 98% | 54% | 35,311 | 28,350 | 6,961 | 168,055 | 104 | 2026-11-18 | 2026-10-16 | 2026-08-06 |

| IBM | 42% | 68% | 45% | 59,763 | 42,758 | 17,005 | 547,280 | 76 | 2026-10-21 | 2026-10-16 | 2026-08-06 |

| IEF | 6% | 28% | 100% | 20,525 | 11,165 | 9,360 | 253,556 | 2026-10-16 | 2026-08-06 | ||

| INFQ | 99% | 7% | 33% | 4,295 | 3,052 | 1,243 | 179,974 | 6 | 2026-08-12 | 2026-10-16 | 2026-08-06 |

| INFY | 75% | 86% | 49% | 3,038 | 1,026 | 2,012 | 230,594 | 78 | 2026-10-23 | 2026-10-16 | 2026-08-06 |

| INTC | 87% | 78% | 56% | 801,044 | 550,651 | 250,393 | 4,517,075 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| INTU | 68% | 93% | 61% | 6,524 | 2,987 | 3,537 | 73,332 | 19 | 2026-08-25 | 2026-10-16 | 2026-08-06 |

| IONQ | 119% | 86% | 70% | 82,202 | 47,112 | 35,090 | 552,715 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| IOT | 65% | 47% | 26% | 4,281 | 3,554 | 727 | 68,249 | 21 | 2026-08-27 | 2026-10-16 | 2026-08-06 |

| IREN | 117% | 60% | 42% | 141,821 | 82,678 | 59,143 | 2,213,619 | 41 | 2026-09-16 | 2026-10-16 | 2026-08-06 |

| ISRG | 43% | 78% | 37% | 5,210 | 2,696 | 2,514 | 51,595 | 75 | 2026-10-20 | 2026-10-16 | 2026-08-06 |

| IWM | 17% | 10% | 18% | 1,429,936 | 578,172 | 851,764 | 6,527,846 | 2026-10-16 | 2026-08-06 | ||

| IYR | 19% | 64% | 1% | 1,375 | 281 | 1,094 | 21,440 | 2026-10-16 | 2026-08-06 | ||

| JCI | 42% | 67% | 5% | 2,422 | 2,280 | 142 | 49,543 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| JD | 48% | 79% | 60% | 20,363 | 11,163 | 9,200 | 671,749 | 7 | 2026-08-13 | 2026-10-16 | 2026-08-06 |

| JNJ | 28% | 85% | 40% | 22,989 | 10,885 | 12,104 | 285,051 | 75 | 2026-10-20 | 2026-10-16 | 2026-08-06 |

| JPM | 20% | 7% | 14% | 35,197 | 15,716 | 19,481 | 431,056 | 68 | 2026-10-13 | 2026-10-16 | 2026-08-06 |

| KEY | 41% | 74% | 98% | 539 | 369 | 170 | 33,600 | 75 | 2026-10-20 | 2026-10-16 | 2026-08-06 |

| KGC | 66% | 89% | 58% | 10,745 | 9,151 | 1,594 | 121,053 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| KHC | 32% | 68% | 65% | 92,353 | 85,228 | 7,125 | 314,105 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| KKR | 38% | 23% | 26% | 2,969 | 1,954 | 1,015 | 151,922 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| KLAR | 97% | 53% | 21% | 9,556 | 6,479 | 3,077 | 79,101 | 12 | 2026-08-18 | 2026-10-16 | 2026-08-06 |

| KMB | 40% | 96% | 67% | 3,033 | 1,787 | 1,246 | 50,815 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| KO | 17% | 29% | 0% | 43,307 | 32,083 | 11,224 | 555,745 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| KR | 28% | 38% | 2% | 5,612 | 3,502 | 2,110 | 77,213 | 29 | 2026-09-04 | 2026-10-16 | 2026-08-06 |

| KRE | 22% | 4% | 11% | 249,400 | 206,268 | 43,132 | 895,920 | 2026-10-16 | 2026-08-06 | ||

| KSS | 74% | 43% | 19% | 3,679 | 2,370 | 1,309 | 35,194 | 20 | 2026-08-26 | 2026-10-16 | 2026-08-06 |

| KVYO | 146% | 92% | 54% | 7,368 | 4,284 | 3,084 | 42,810 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| LBTYA | 193% | 87% | 78% | 5,132 | 5,124 | 8 | 35,819 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| LITE | 126% | 92% | 72% | 22,017 | 8,188 | 13,829 | 113,028 | 5 | 2026-08-11 | 2026-10-16 | 2026-08-06 |

| LLY | 39% | 70% | 35% | 86,997 | 48,623 | 38,374 | 207,717 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| LOW | 30% | 50% | 40% | 7,162 | 4,076 | 3,086 | 66,117 | 13 | 2026-08-19 | 2026-10-16 | 2026-08-06 |

| LQD | 7% | 58% | 100% | 4,752 | 2,271 | 2,481 | 451,094 | 2026-10-16 | 2026-08-06 | ||

| LQDA | 155% | 81% | 36% | 10,012 | 6,111 | 3,901 | 61,881 | 6 | 2026-08-12 | 2026-10-16 | 2026-08-06 |

| LRCX | 86% | 88% | 66% | 53,334 | 26,139 | 27,195 | 347,910 | 76 | 2026-10-21 | 2026-10-16 | 2026-08-06 |

| LVS | 43% | 66% | 8% | 5,184 | 2,977 | 2,207 | 59,077 | 76 | 2026-10-21 | 2026-10-16 | 2026-08-06 |

| LYFT | 93% | 91% | 89% | 18,898 | 11,968 | 6,930 | 430,879 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| MA | 27% | 54% | 52% | 5,316 | 2,834 | 2,482 | 52,884 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| MAR | 37% | 76% | 58% | 5,163 | 3,037 | 2,126 | 32,919 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| MAT | 47% | 45% | 36% | 9,585 | 8,850 | 735 | 47,443 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| MCD | 23% | 73% | 95% | 46,943 | 33,199 | 13,744 | 231,025 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| MCHP | 87% | 93% | 100% | 27,848 | 9,920 | 17,928 | 255,599 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| MDT | 25% | 59% | 100% | 13,201 | 4,774 | 8,427 | 119,394 | 26 | 2026-09-01 | 2026-10-16 | 2026-08-06 |

| META | 39% | 74% | 34% | 600,406 | 412,016 | 188,390 | 2,593,006 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| MMM | 25% | 12% | 17% | 11,294 | 8,334 | 2,960 | 65,242 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| MRK | 33% | 76% | 48% | 15,300 | 10,235 | 5,065 | 264,899 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| MRNA | 87% | 77% | 100% | 23,170 | 10,900 | 12,270 | 311,630 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| MRVL | 101% | 85% | 61% | 100,239 | 62,620 | 37,619 | 1,123,959 | 21 | 2026-08-27 | 2026-10-16 | 2026-08-06 |

| MS | 34% | 62% | 100% | 11,277 | 6,008 | 5,269 | 151,612 | 69 | 2026-10-14 | 2026-10-16 | 2026-08-06 |

| MSFT | 30% | 63% | 28% | 710,747 | 401,499 | 309,248 | 3,908,840 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| MSTR | 74% | 58% | 28% | 337,470 | 262,013 | 75,457 | 1,788,342 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| NBIS | 148% | 95% | 73% | 137,642 | 61,016 | 76,626 | 1,064,336 | 6 | 2026-08-12 | 2026-10-16 | 2026-08-06 |

| NEM | 46% | 40% | 3% | 37,141 | 27,660 | 9,481 | 338,510 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| NFLX | 40% | 77% | 32% | 304,802 | 232,490 | 72,312 | 3,694,571 | 75 | 2026-10-20 | 2026-10-16 | 2026-08-06 |

| NKE | 19052% | 100% | 100% | 67,530 | 45,134 | 22,396 | 1,347,221 | 49 | 2026-09-24 | 2026-10-16 | 2026-08-06 |

| NLY | 23% | 28% | 64% | 4,194 | 1,679 | 2,515 | 94,728 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| NNE | 111% | 66% | 12% | 3,906 | 2,239 | 1,667 | 32,196 | 7 | 2026-08-13 | 2026-10-16 | 2026-08-06 |

| NOW | 63% | 77% | 43% | 107,031 | 80,316 | 26,715 | 1,087,350 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| NTSK | 61% | 7% | 82% | 1,698 | 1,597 | 101 | 33,641 | 55 | 2026-09-30 | 2026-10-16 | 2026-08-06 |

| NU | 44% | 48% | 18% | 22,979 | 14,816 | 8,163 | 1,025,928 | 7 | 2026-08-13 | 2026-10-16 | 2026-08-06 |

| NVDA | 37% | 32% | 0% | 6,216,386 | 4,334,082 | 1,882,304 | 12,609,488 | 20 | 2026-08-26 | 2026-10-16 | 2026-08-06 |

| NVO | 39% | 21% | 18% | 92,165 | 62,304 | 29,861 | 1,201,426 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| NXE | 94% | 79% | 94% | 13,830 | 8,997 | 4,833 | 100,912 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| OIH | 34% | 29% | 22% | 99 | 27 | 72 | 2,659 | 2026-10-16 | 2026-08-06 | ||

| OKE | 33% | 35% | 100% | 2,107 | 1,655 | 452 | 73,017 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| OKLO | 113% | 75% | 47% | 22,476 | 12,983 | 9,493 | 415,840 | 1 | 2026-08-07 | 2026-10-16 | 2026-08-06 |

| ON | 93% | 91% | 60% | 20,121 | 12,419 | 7,702 | 192,687 | 88 | 2026-11-02 | 2026-10-16 | 2026-08-06 |

| ONON | 72% | 91% | 100% | 9,011 | 8,170 | 841 | 136,529 | 5 | 2026-08-11 | 2026-10-16 | 2026-08-06 |

| ORCL | 63% | 66% | 36% | 162,919 | 113,800 | 49,119 | 2,587,594 | 39 | 2026-09-14 | 2026-10-16 | 2026-08-06 |

| OSCR | 122% | 98% | 3% | 43,824 | 35,584 | 8,240 | 286,140 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| OWL | 109% | 98% | 87% | 40,816 | 28,246 | 12,570 | 919,924 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| OXY | 40% | 74% | 50% | 72,117 | 57,979 | 14,138 | 576,873 | 96 | 2026-11-10 | 2026-10-16 | 2026-08-06 |

| PAAS | 70% | 82% | 54% | 15,995 | 13,039 | 2,956 | 180,629 | 6 | 2026-08-12 | 2026-10-16 | 2026-08-06 |

| PANW | 62% | 86% | 4% | 37,865 | 11,646 | 26,219 | 266,432 | 26 | 2026-09-01 | 2026-10-16 | 2026-08-06 |

| PBR | 40% | 54% | 35% | 25,500 | 20,031 | 5,469 | 886,339 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| PCG | 49% | 79% | 89% | 124,675 | 111,893 | 12,782 | 1,330,880 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| PDD | 35% | 38% | 23% | 25,381 | 10,123 | 15,258 | 633,227 | 25 | 2026-08-31 | 2026-10-16 | 2026-08-06 |

| PENG | 131% | 74% | 44% | 3,372 | 2,902 | 470 | 46,517 | 68 | 2026-10-13 | 2026-10-16 | 2026-08-06 |

| PEP | 27% | 66% | 0% | 12,288 | 6,986 | 5,302 | 257,529 | 68 | 2026-10-13 | 2026-10-16 | 2026-08-06 |

| PFE | 21% | 9% | 0% | 88,890 | 54,418 | 34,472 | 2,194,444 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| PG | 22% | 42% | 13% | 44,331 | 25,517 | 18,814 | 294,107 | 76 | 2026-10-21 | 2026-10-16 | 2026-08-06 |

| PL | 93% | 29% | 22% | 6,862 | 4,148 | 2,714 | 119,047 | 39 | 2026-09-14 | 2026-10-16 | 2026-08-06 |

| PLTR | 53% | 45% | 30% | 653,258 | 391,681 | 261,577 | 3,431,460 | 95 | 2026-11-09 | 2026-10-16 | 2026-08-06 |

| PM | 33% | 63% | 0% | 5,689 | 2,500 | 3,189 | 72,806 | 75 | 2026-10-20 | 2026-10-16 | 2026-08-06 |

| PRMB | 55% | 43% | 0% | 2,950 | 2,756 | 194 | 54,418 | 91 | 2026-11-05 | 2026-10-16 | 2026-08-06 |

| PYPL | 26% | 2% | 9% | 22,537 | 16,006 | 6,531 | 1,335,064 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| PZZA | 100% | 86% | 0% | 8,337 | 4,927 | 3,410 | 70,724 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| QBTS | 111% | 67% | 100% | 36,522 | 22,711 | 13,811 | 364,805 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| QCOM | 63% | 74% | 100% | 55,002 | 31,104 | 23,898 | 725,373 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| QXO | 91% | 95% | 0% | 24,756 | 17,848 | 6,908 | 334,028 | 5 | 2026-08-11 | 2026-10-16 | 2026-08-06 |

| RARE | 93% | 73% | 83% | 11,048 | 4,359 | 6,689 | 42,522 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| RBLX | 74% | 65% | 33% | 24,345 | 10,915 | 13,430 | 235,134 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| RBRK | 96% | 82% | 57% | 5,077 | 4,182 | 895 | 59,000 | 39 | 2026-09-14 | 2026-10-16 | 2026-08-06 |

| RDDT | 72% | 50% | 27% | 34,727 | 17,273 | 17,454 | 318,894 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| RGTI | 122% | 79% | 49% | 48,413 | 27,862 | 20,551 | 445,943 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| RIO | 41% | 75% | 36% | 13,253 | 3,222 | 10,031 | 71,764 | 202 | 2027-02-24 | 2026-10-16 | 2026-08-06 |

| RIVN | 65% | 40% | 32% | 75,343 | 58,478 | 16,865 | 1,392,031 | 96 | 2026-11-10 | 2026-10-16 | 2026-08-06 |

| RKLB | 103% | 74% | 60% | 135,620 | 99,680 | 35,940 | 858,720 | 4 | 2026-08-10 | 2026-10-16 | 2026-08-06 |

| RKT | 82% | 86% | 29% | 54,096 | 31,439 | 22,657 | 554,033 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| RSI | 163% | 94% | 76% | 551 | 334 | 217 | 89,786 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| RTX | 29% | 50% | 100% | 13,547 | 9,065 | 4,482 | 125,676 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| RVMD | 61% | 50% | 41% | 2,916 | 2,456 | 460 | 40,388 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| SBUX | 31% | 37% | 21% | 15,313 | 9,352 | 5,961 | 289,060 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| SCHW | 29% | 46% | 100% | 15,488 | 6,796 | 8,692 | 291,993 | 70 | 2026-10-15 | 2026-10-16 | 2026-08-06 |

| SE | 83% | 94% | 72% | 5,387 | 3,390 | 1,997 | 90,197 | 5 | 2026-08-11 | 2026-10-16 | 2026-08-06 |

| SEDG | 110% | 62% | 41% | 21,869 | 12,769 | 9,100 | 138,724 | -1 | 2026-08-05 | 2026-10-16 | 2026-08-06 |

| SGHC | 63% | 35% | 18% | 13,978 | 10,247 | 3,731 | 76,142 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| SGI | 47% | 50% | 20% | 6,798 | 6,444 | 354 | 32,657 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| SHAZ | 148% | 57% | 44% | 4,956 | 4,092 | 864 | 34,817 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| SHEL | 32% | 81% | 1% | 4,099 | 2,993 | 1,106 | 90,218 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| SHOP | 62% | 58% | 32% | 175,930 | 99,653 | 76,277 | 773,059 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| SIRI | 35% | 26% | 0% | 20,909 | 20,142 | 767 | 187,910 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| SKHY | 113% | 0% | 0% | 85,461 | 30,368 | 55,093 | 809,172 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| SLS | 191% | 7% | 6% | 18,101 | 11,691 | 6,410 | 593,089 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| SLV | 45% | 48% | 0% | 560,339 | 438,879 | 121,460 | 4,759,806 | 2026-10-16 | 2026-08-06 | ||

| SNOW | 69% | 76% | 38% | 42,560 | 12,064 | 30,496 | 247,551 | 27 | 2026-09-02 | 2026-10-16 | 2026-08-06 |

| SOFI | 51% | 8% | 22% | 280,186 | 196,678 | 83,508 | 3,612,737 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| SONY | 29% | 14% | 1% | 2,649 | 2,274 | 375 | 82,595 | 96 | 2026-11-10 | 2026-10-16 | 2026-08-06 |

| SPCX | 112% | 74% | 41% | 2,210,697 | 1,021,729 | 1,188,968 | 4,469,236 | 118 | 2026-12-02 | 2026-10-16 | 2026-08-06 |

| SPOT | 53% | 69% | 41% | 16,156 | 11,949 | 4,207 | 83,009 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| STM | 73% | 76% | 38% | 37,964 | 34,466 | 3,498 | 137,095 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| STX | 116% | 95% | 79% | 21,978 | 8,839 | 13,139 | 97,427 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| STZ | 33% | 36% | 25% | 2,656 | 1,683 | 973 | 36,366 | 56 | 2026-10-01 | 2026-10-16 | 2026-08-06 |

| SU | 52% | 95% | 78% | 2,216 | 1,467 | 749 | 72,134 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| SWK | 46% | 62% | 100% | 1,190 | 690 | 500 | 60,328 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| T | 38% | 91% | 93% | 90,032 | 42,866 | 47,166 | 965,576 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| TAL | 55% | 24% | 99% | 160 | 91 | 69 | 36,447 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| TEAM | 144% | 99% | 91% | 15,726 | 7,806 | 7,920 | 87,201 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| TECK | 76% | 91% | 56% | 2,240 | 2,105 | 135 | 34,961 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| TEM | 75% | 34% | 84% | 11,560 | 6,169 | 5,391 | 219,997 | 96 | 2026-11-10 | 2026-10-16 | 2026-08-06 |

| TENX | 610% | 97% | 2% | 6,422 | 3,479 | 2,943 | 63,933 | 104 | 2026-11-18 | 2026-10-16 | 2026-08-06 |

| TFC | 37% | 65% | 27% | 1,006 | 596 | 410 | 54,299 | 71 | 2026-10-16 | 2026-10-16 | 2026-08-06 |

| TGT | 40% | 72% | 25% | 23,562 | 18,923 | 4,639 | 217,853 | 13 | 2026-08-19 | 2026-10-16 | 2026-08-06 |

| TJX | 23% | 42% | 29% | 4,760 | 2,662 | 2,098 | 60,658 | 13 | 2026-08-19 | 2026-10-16 | 2026-08-06 |

| TLT | 14% | 91% | 100% | 407,734 | 312,866 | 94,868 | 8,468,540 | 2026-10-16 | 2026-08-06 | ||

| TMDX | 64% | 36% | 0% | 11,873 | 8,615 | 3,258 | 47,794 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| TMUS | 37% | 75% | 5% | 5,393 | 3,123 | 2,270 | 87,509 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| TOST | 47% | 27% | 21% | 31,521 | 25,144 | 6,377 | 288,456 | 96 | 2026-11-10 | 2026-10-16 | 2026-08-06 |

| TSCO | 51% | 82% | 11% | 6,562 | 5,119 | 1,443 | 104,803 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| TSEM | 109% | 78% | 51% | 7,818 | 3,611 | 4,207 | 36,911 | 102 | 2026-11-16 | 2026-10-16 | 2026-08-06 |

| TSLA | 42% | 30% | 24% | 1,994,794 | 1,158,525 | 836,269 | 4,195,279 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| TSM | 45% | 56% | 100% | 118,911 | 59,490 | 59,421 | 1,481,301 | 70 | 2026-10-15 | 2026-10-16 | 2026-08-06 |

| TTD | 114% | 91% | 98% | 36,432 | 23,224 | 13,208 | 554,190 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| TTMI | 137% | 96% | 2% | 15,994 | 12,862 | 3,132 | 38,056 | 90 | 2026-11-04 | 2026-10-16 | 2026-08-06 |

| TXN | 57% | 83% | 0% | 16,729 | 7,415 | 9,314 | 137,937 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| UAL | 54% | 52% | 38% | 20,191 | 4,709 | 15,482 | 139,271 | 75 | 2026-10-20 | 2026-10-16 | 2026-08-06 |

| UBER | 41% | 67% | 44% | 302,993 | 188,759 | 114,234 | 1,092,666 | 84 | 2026-10-29 | 2026-10-16 | 2026-08-06 |

| UMC | 93% | 74% | 63% | 1,977 | 1,619 | 358 | 110,093 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| UNG | 40% | 8% | 33% | 14,789 | 8,520 | 6,269 | 236,335 | 2026-10-16 | 2026-08-06 | ||

| UNH | 30% | 32% | 2% | 65,124 | 40,671 | 24,453 | 664,143 | 64 | 2026-10-09 | 2026-10-16 | 2026-08-06 |

| UPS | 27% | 22% | 16% | 18,222 | 9,152 | 9,070 | 237,562 | 82 | 2026-10-27 | 2026-10-16 | 2026-08-06 |

| UPST | 78% | 44% | 21% | 49,670 | 36,312 | 13,358 | 235,136 | 96 | 2026-11-10 | 2026-10-16 | 2026-08-06 |

| URA | 47% | 13% | 99% | 7,644 | 6,115 | 1,529 | 170,216 | 2026-10-16 | 2026-08-06 | ||

| USB | 29% | 58% | 0% | 5,395 | 3,902 | 1,493 | 84,138 | 70 | 2026-10-15 | 2026-10-16 | 2026-08-06 |

| USO | 49% | 56% | 3% | 169,167 | 79,224 | 89,943 | 1,129,172 | 2026-10-16 | 2026-08-06 | ||

| UUUU | 86% | 18% | 13% | 19,833 | 9,430 | 10,403 | 353,267 | 85 | 2026-10-30 | 2026-10-16 | 2026-08-06 |

| V | 22% | 34% | 44% | 13,022 | 7,480 | 5,542 | 250,173 | 89 | 2026-11-03 | 2026-10-16 | 2026-08-06 |

| VKTX | 90% | 66% | 26% | 7,178 | 5,463 | 1,715 | 126,276 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| VOD | 56% | 59% | 6% | 1,107 | 642 | 465 | 97,684 | 96 | 2026-11-10 | 2026-10-16 | 2026-08-06 |

| VRT | 79% | 83% | 55% | 27,198 | 13,615 | 13,583 | 283,815 | 83 | 2026-10-28 | 2026-10-16 | 2026-08-06 |

| VSH | 139% | 84% | 53% | 5,534 | 4,423 | 1,111 | 47,172 | 97 | 2026-11-11 | 2026-10-16 | 2026-08-06 |

| VST | 72% | 93% | 72% | 57,894 | 50,356 | 7,538 | 323,522 | 1 | 2026-08-07 | 2026-10-16 | 2026-08-06 |

| VTRS | 59% | 72% | 31% | 21,408 | 1,008 | 20,400 | 49,319 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| VZ | 27% | 70% | 99% | 77,540 | 36,292 | 41,248 | 958,774 | 75 | 2026-10-20 | 2026-10-16 | 2026-08-06 |

| WBD | 23% | 24% | 42% | 103,860 | 29,520 | 74,340 | 1,677,247 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| WDC | 121% | 97% | 82% | 86,561 | 47,543 | 39,018 | 197,530 | 77 | 2026-10-22 | 2026-10-16 | 2026-08-06 |

| WFC | 33% | 76% | 53% | 27,424 | 18,902 | 8,522 | 579,570 | 68 | 2026-10-13 | 2026-10-16 | 2026-08-06 |

| WMB | 29% | 41% | 99% | 20,827 | 3,227 | 17,600 | 251,831 | 88 | 2026-11-02 | 2026-10-16 | 2026-08-06 |

| WMT | 34% | 88% | 1% | 134,023 | 46,968 | 87,055 | 838,088 | 14 | 2026-08-20 | 2026-10-16 | 2026-08-06 |

| WPM | 63% | 91% | 45% | 7,565 | 4,937 | 2,628 | 48,364 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

| WULF | 115% | 80% | 61% | 164,804 | 126,746 | 38,058 | 1,963,212 | 102 | 2026-11-16 | 2026-10-16 | 2026-08-06 |

| WYNN | 42% | 37% | 30% | 54,688 | 46,158 | 8,530 | 181,607 | 91 | 2026-11-05 | 2026-10-16 | 2026-08-06 |

| XE | 162% | 82% | 49% | 9,488 | 8,114 | 1,374 | 76,701 | 7 | 2026-08-13 | 2026-10-16 | 2026-08-06 |

| XLE | 26% | 59% | 7% | 177,386 | 87,050 | 90,336 | 2,421,009 | 2026-10-16 | 2026-08-06 | ||

| XLF | 16% | 38% | 30% | 214,654 | 44,469 | 170,185 | 3,257,065 | 2026-10-16 | 2026-08-06 | ||

| XLK | 41% | 96% | 77% | 32,765 | 7,141 | 25,624 | 306,661 | 2026-10-16 | 2026-08-06 | ||

| XLP | 16% | 63% | 32% | 180,165 | 5,300 | 174,865 | 286,087 | 2026-10-16 | 2026-08-06 | ||

| XLV | 23% | 93% | 75% | 21,143 | 12,622 | 8,521 | 237,700 | 2026-10-16 | 2026-08-06 | ||

| XLY | 23% | 38% | 45% | 3,592 | 2,643 | 949 | 251,959 | 2026-10-16 | 2026-08-06 | ||

| XME | 55% | 82% | 36% | 2,442 | 1,954 | 488 | 25,143 | 2026-10-16 | 2026-08-06 | ||

| XOM | 29% | 49% | 0% | 44,795 | 30,308 | 14,487 | 633,340 | 78 | 2026-10-23 | 2026-10-16 | 2026-08-06 |

| XOP | 39% | 71% | 47% | 8,053 | 2,618 | 5,435 | 118,833 | 2026-10-16 | 2026-08-06 | ||

| XPEV | 62% | 56% | 35% | 54,948 | 49,328 | 5,620 | 408,747 | 18 | 2026-08-24 | 2026-10-16 | 2026-08-06 |

| YPF | 61% | 83% | 18% | 1,135 | 664 | 471 | 36,077 | 4 | 2026-08-10 | 2026-10-16 | 2026-08-06 |

| ZIM | 56% | 44% | 40% | 6,542 | 4,964 | 1,578 | 100,985 | 13 | 2026-08-19 | 2026-10-16 | 2026-08-06 |

| ZTS | 64% | 94% | 100% | 23,698 | 11,451 | 12,247 | 108,548 | 0 | 2026-08-06 | 2026-10-16 | 2026-08-06 |

SlashTraders vs S&P 500: 450% Outperformance, Verified Trades and How to Copy Every Alert

Thanks for sharing the calculation of Option IV, it reminds me of my high school statistics course.

Just found out that Options Analyzer can really find a list of high IV stocks fast!

So I can find more Iron Condor trading opportunities.

Thank you, sir.

That's right.

You can trade LeSports and Woodhawks by understanding the relationship of volatility to option value.

Thanks for sharing the difference between IV and HV, it gives me more confidence in trading options!

HV and IV are both analyzing fluctuating data.

One is the standard deviation of the past.

One is the estimated future standard deviation