Do you know how to use the option Greeks to analyse the risks of your trades?

Today SlashTraders will discuss the major option Greeks (delta, gamma, theta and vega) so you have the tools to control risks when trading options.

What Is Delta?

Delta is the changes to options price with respect to changes in the underlying price. A positive delta indicates the trade will profit when the stock price goes up, and loses when the price goes down.

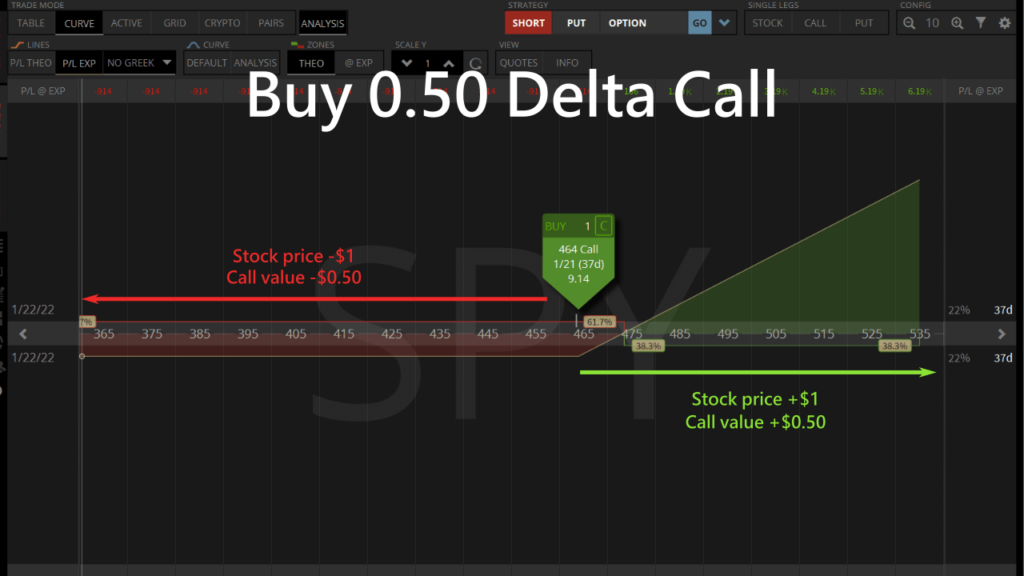

If we purchase a Call option at the market price, the trade is 0.50 delta. The Call option value goes up $0.50 for every $1 increase in market price. When the market price drops by $1, the Call option price lowers by $0.50.

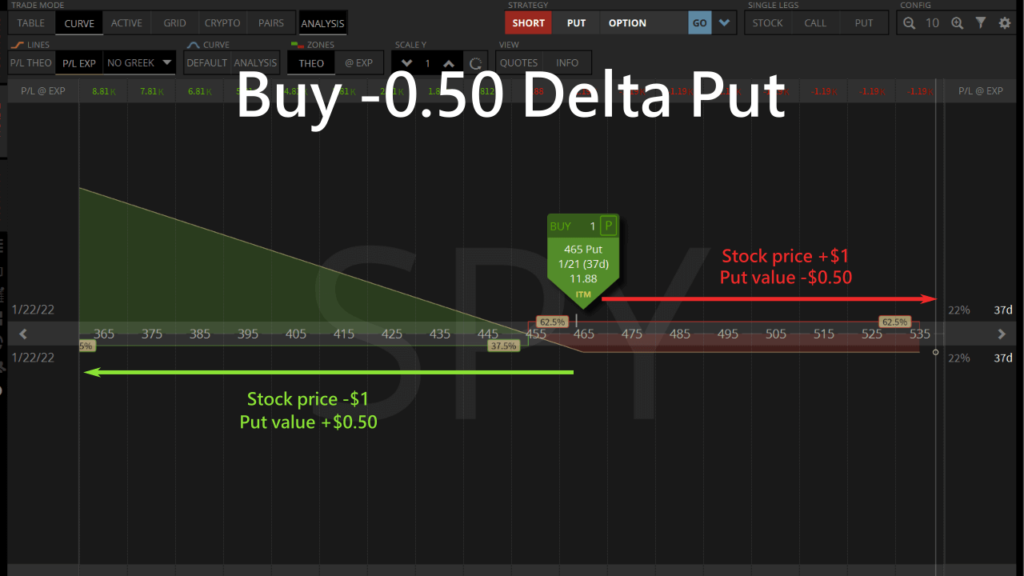

Buying an ATM Put option is -0.50 delta, which means the Put option value drops by $0.50 for every $1 rise in stock price. If the market price goes down by $1, the Put option value goes up by $0.50.

If we look at the long Call deltas at different strike prices:

- ATM Call is 0.50 delta.

- OTM Calls have a lower delta.

- ITM Calls have a greater delta.

Delta is a good way to estimate the chance of ITM at expiration.

| Delta | ITM chance |

|---|---|

| 0.75 | 75% |

| 0.50 | 50% |

| 0.25 | 25% |

Buying and selling different option types result in different signs of deltas.

| Options strategies | Delta | Direction to profit |

|---|---|---|

| Buy Call | Positive | Bullish stock price |

| Buy Put | Negative | Bearish stock price |

| Sell Call | Negative | Bearish stock price |

| Sell Put | Positive | Bullish stock price |

So we can use the combined delta to see whether we are bullish or bearish in our investment portfolio. We can use trades of opposite deltas to hedge and protect our investments.

Use Positive Delta for Bullish Trades

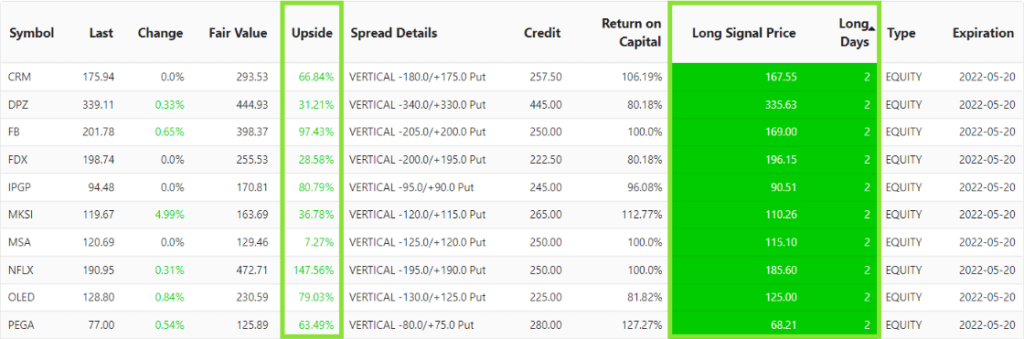

The Bull Put Spread Screener uses historical chart analysis to find bottom out stocks that have a high probability of an upward correction that we can sell Bull Put Spreads to profit from the dip.

We want to find heavily undervalued, bottomed out underlying that have a high probability of going up.

- Long Days indicates the number of trading days since the most recent bullish signal, based on technical analysis. A small number means we can enter the trade at the start of the bullish trend.

- Long Signal Price shows the recent dip based on technical analysis. We can be confident the stock price will not fall below this price level in the short term.

- Fundamental analysis shows us the Fair Value of the underlying. Then it compares with the Last value to find the potential Upside. The higher the Upside, the greater the confidence of the stock being undervalued.

We can combine the 3 bullish signals in the screener to execute high probability bullish trades. The screener also helps us find high Return on Capital 0.50 delta ATM Bull Put Spreads.

Then we can use the Spread Details to find the ATM Bull Put Spreads with the respective Return on Capital.

Let's pick the highest probability and high return Bull Put Vertical Spread entry points.

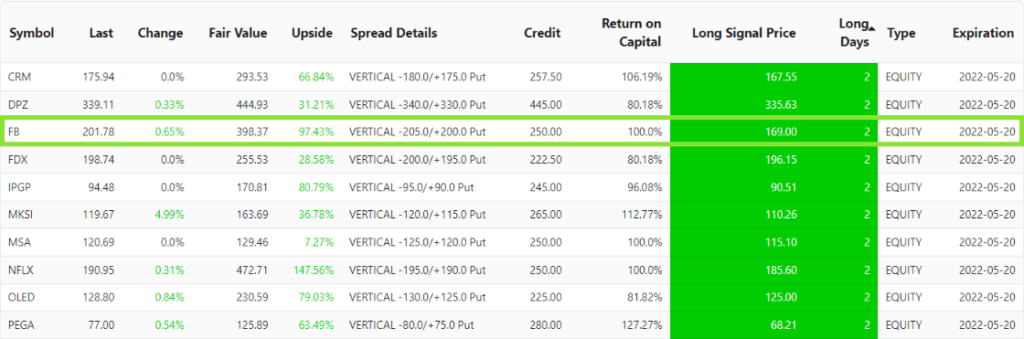

By combining Long Days and Upside, out of all bullish stocks that started within 2 trading days, FB is extremely undervalued with 97% upside. So it has a high probability of a bullish trend.

The FB price chart shows it reached a low point at Long Signal Price of $169 2 trading days ago, and has been bullish ever since.

Considering FB is heavily undervalued, we can be confident of a bullish outlook.

We can sell a FB Bull Put Spread option that expires next month. If the Meta stock price does not fall before expiration, we can profit 103% from the trade.

Use Negative Delta for Bearish Trades

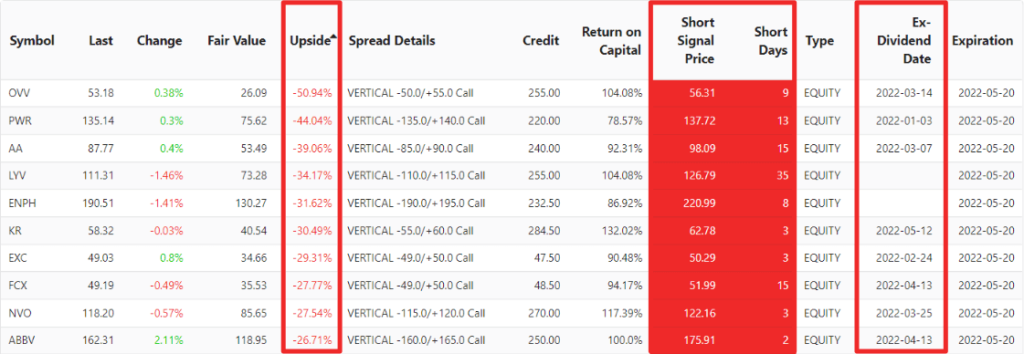

The Bear Call Spread Screener uses chart analysis to find overvalued stocks with a high probability of a downward correction that we can sell Bear Call Spreads to open.

We want to find heavily overvalued underlying that have a high probability of going down.

- The options screener uses fundamental analysis to calculate the Fair Value of the underlying then compare that with the Last value to find the potential Upside of the stock. When the Upside is less than -30%, we have high confidence in a bearish outlook.

- Short Signal Price shows the topped out price from our technical analysis. So we know the stock price will not rise beyond this price in the short term.

- Short Days indicate the number of trading days has passed since the last short signal. As soon as the short signal appears, there is a high probability of a bearish move.

- We also need to avoid Ex-Dividend Date before options expiration. On one hand Ex-Dividend Date usually lead to rising prices and assignment. On the other hand, if you get assigned, you might need to pay dividends for shorting the stock.

Since we are strongly bearish about our trade, we can use -0.50 delta ATM Bear Call Spread to calculate Return on Capital. This gives us the highest return when we are right, and the lowest maximum loss if we are wrong.

So we can look at the screener for the best ATM Bear Call Spread ideas.

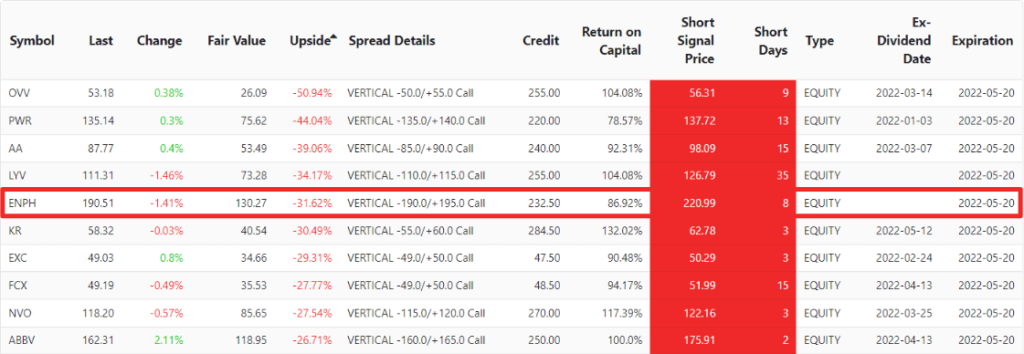

By combining Upside and Short Days, we see ENPH is one of the most overvalued stocks, and has a short signal 8 trading days ago. It doesn't have an Ex-Dividend Date coming up. So it has a high probability of a bearish trend.

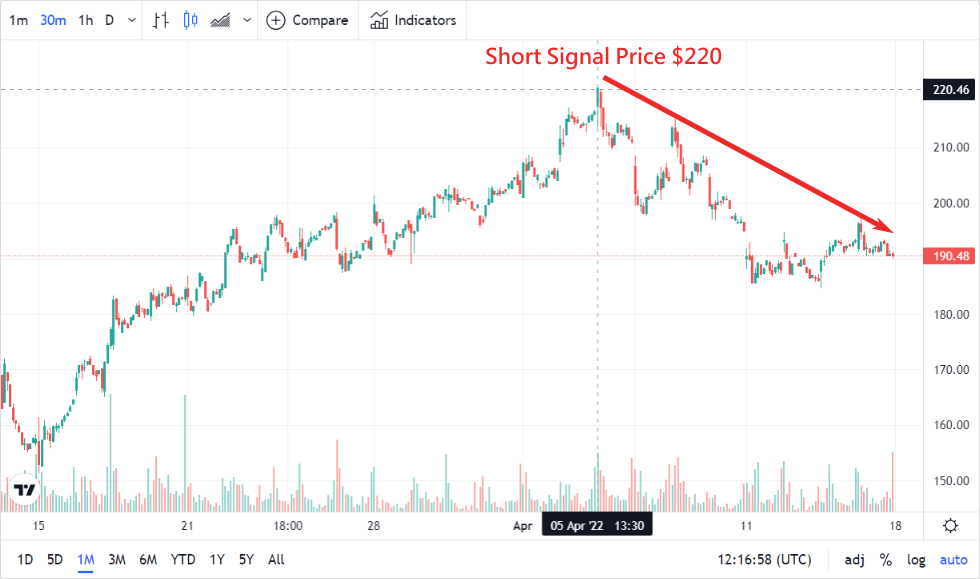

By checking the Enphase price trends, we confirm ENPH reached a high point at $220, similar to the Short Signal Price in our Bear Call Spread list, 8 trading days ago, and has been bearish ever since. We expect ENPH to stay below Short Signal Price in the short term.

We can sell an ENPH ATM Call Spread option that expires in 35 days. If the ENPH stock price does not rise before expiration, we have the potential to profit 86% from the trade.

What Is Gamma?

Gamma is the changes to delta with respect to changes in stock price. It is also the acceleration to options prices with respect to changes in stock price.

In the case of the current SPY Call, when the cutoff date is the same, the Call with the flat ATM has the highest gamma, and the farther the performance price is from the market price, the lower the gamma will be.

For options at identical strike prices, the closer to expiration the larger the gamma.

| Days to expiration | Gamma |

|---|---|

| 35 days | 1.26 |

| 6 days | 3.39 |

This means as an option gets closer to expiration, the gamma expansion increases the impact of delta to the options prices, leading to big unpredictable gains and losses with small price fluctuations.

So we usually close our options trades around 14 days before expiration to minimise gamma risk.

What Is Theta?

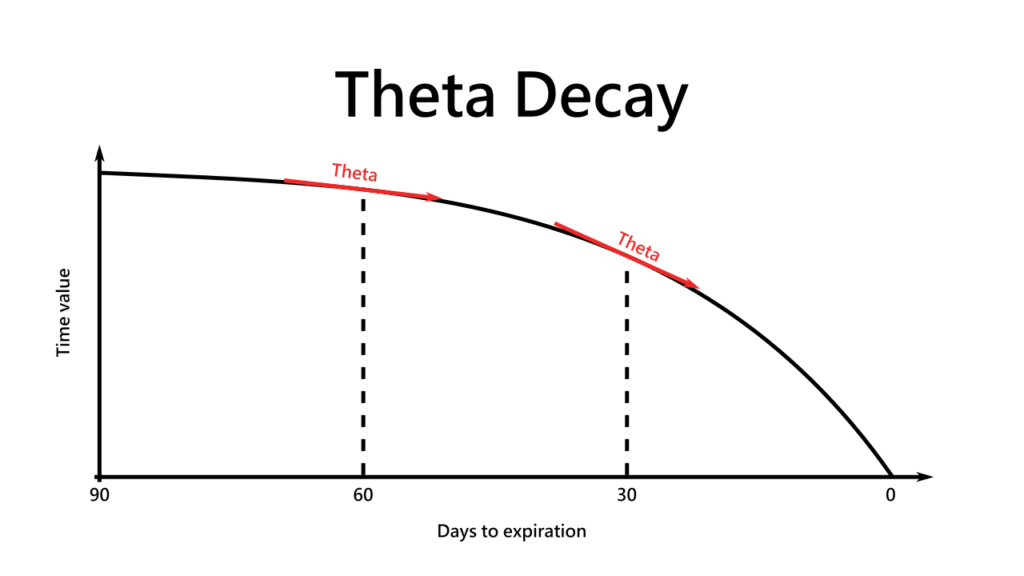

Theta is the changes to options value with respect to changes in time. Theta is negative because every passing day causes the option value to decay a little.

Here is the relationship between options time value and time to expiration. The gradient of the chart is theta.

We can see the theta decay is slower around 90 days to expiration, then the decay speed increases as time passes until the theta decay becomes quite large at less than 30 days to expiration.

This is the reason why we usually sell options that expire around 30 days, so the theta decay is fast enough for us to close the trade for a profit.

What Is Vega?

Vega is the changes to options value with respect to changes in IV. Vega helps us learn about changes to IV to buy low and sell high options for profit.

The Options Scanner shows SPY and MDB have similar stock prices at different IV values, leading to different option prices.

| Stocks | Stock price | IV | ATM Call value |

|---|---|---|---|

| SPY | $459.87 | 19% | $9.38 |

| MDB | $497.85 | 55% | $34.50 |

So we make money by selling expensive options at high IV, and buying cheap options at low IV.

| Strategies | Vega | Ways to profit |

|---|---|---|

| Buy options | Positive | Expanding IV |

| Sell options | Negative | Contracting IV |

Use Both Theta and Vega to Sell High-Return Strangles

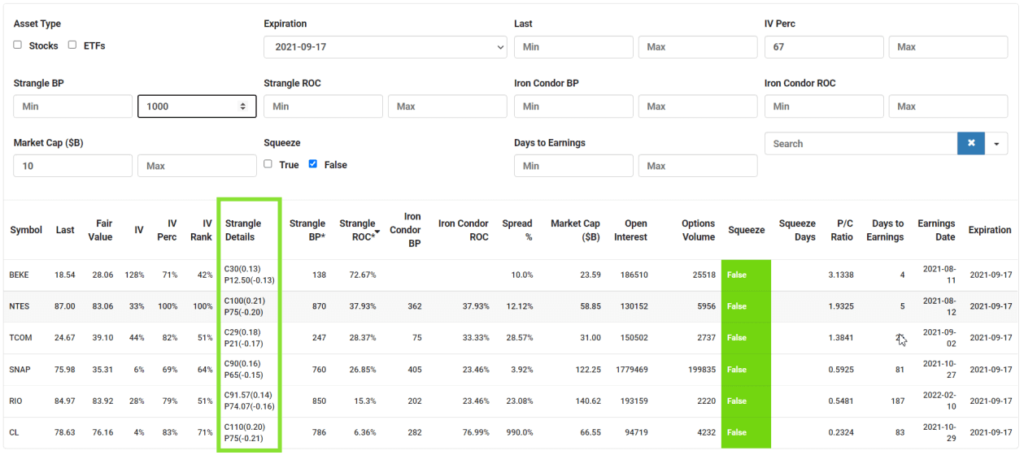

SlashTraders' Options Scanner is designed to find high probability and high return Strangles in seconds. Here are some tips to use the filtering function to find the best short Strangle entry points.

- We want to choose opportunities with longer than 30 DTE to get the safest theta decay.

- IV Perc is the relative position of current IV compared to the range of IVs in all the trading days in the previous year. We can filter IV Perc >67% to find stocks with IV higher than 2/3 of trading days in the past year. So they have a high chance of contracting IV and vega in our favour.

- Open Interest is the number of the total number of outstanding derivative contracts for the underlying. We can find stocks with Open Interests >100,000 to make sure the liquidity is good, so we get our trades filled easily.

- By choosing Market Cap ($B) larger than 10 billion, we avoid choosing stocks that can get manipulated and explode like GME.

- A good idea is to eliminate stocks with depressed price movement, because IV will expand soon after. So we need to choose Squeeze status as False.

- To further reduce risks, we can limit the Strangle BP to less than $1000, so we can easily diversify our portfolio.

Finally, we can sort the Strangles ROC by descending order to get a shortlist of the highest return Strangles.

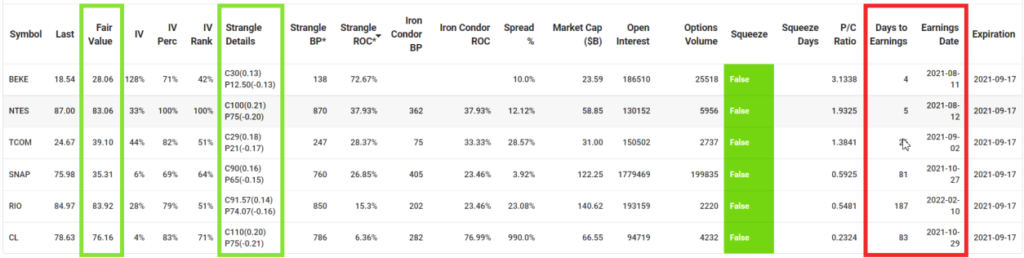

You can see the Fair Value and Earnings Date for every underlying to help us fine-tune the selection and get the best entry points.

If the Fair Value is very close to the strikes listed in the Strangle Details, we can be even more confident that the Strangles will be profitable.

Earnings Date is an event that can cause large price movements, so we want to avoid selling neutral options strategy past Earnings Date.

We can see the top 3 stocks with highest return have upcoming Earnings, so selling Strangles for them are quite risky.

SNAP's Fair Value is on the low side, but considering that SNAP has a robust social media platform like FB, consider trading SNAP's Strangles option.

If we sell to open a Strangle for SNAP that expires in 40 days, it has a 27% maximum return if SNAP stock price does not exceed the Put and Call strike prices before options expiration.

Now you know the characteristics of delta, gamma, theta and vega, you can use the option Greeks to analyse option strategies then buy low and sell high for a profit.

SlashTraders vs S&P 500: 450% Outperformance, Verified Trades and How to Copy Every Alert

I thought the Greek alphabet was complicated, but now I understand it.

Thank you, sir.

You're welcome.

Thank you for sharing.

Finally understand what gamma risk is when trading options.

Yes, you need to learn to avoid gamma risk in order to stabilize profits from trading options.

So there's a lot to learn about option risk management. Thank you.

Yes, once you understand the meaning of common Greek values, you can find a portfolio that provides long-term stable profits and diversified risk.

Thank you for the great explanation of the options greeks, now I'm more confident in managing my options trades.

Happy to help