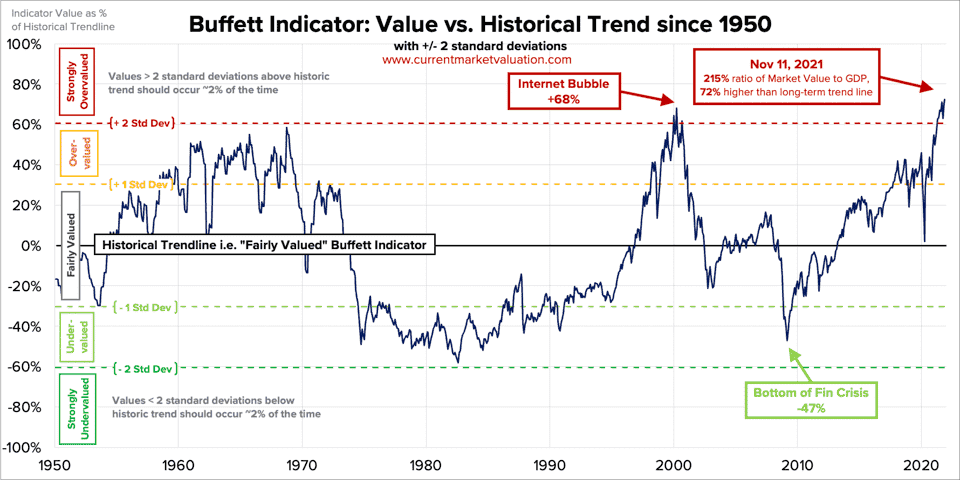

As lots of experts say, the market is in a bubble right now, and it may burst any time soon.

If we look back on history, the market made 77 record highs since 1995, before the infamous Internet Bubble burst in 2000. In more recent memory, immediately after the stock market crash in March 2020, the S&P 500 went on a massive, historical bull run, making more record highs than 20 years ago.

Experts say the market was overvalued before the 2020 crash, and even more so right now in 2021. Inflation is also causing bubbles in the stock market with plenty of cash looking for attractive returns.

The Buffett indicator shows the major recent market crashes were usually preceded by a historic bull trend.

At SlashTraders, we always look at the market as a probability system. Despite the market being unpredictable most times, the market has proven to consistently do two things with a high probability:

- Mean reversion to fair valuations.

- Mean reversion to historical volatility levels.

Since the current market is likely to be overvalued, we can expect it to revert the mean, or correct downwards soon.

Whether the market is overvalued or not, it is our opinion that you should always have protection in place with your investment portfolio.

What Is Hedging?

Hedging is a strategy that limits risks in your investment in case the market goes against your expectation. It is like insurance coverage for your hard-earned money.

The market has an upward bias that goes up 70-80% of the time. But there are pullbacks (-5% to -10% two to three times a year), corrections (-10% to -20% every two years), bear markets (-20% or more every 5-6 years) along the way that we want to hedge against.

It may only take 4 weeks for the market to go down 50%, but it may take 2 years to recover from such a loss. Many people think that you need a 50% gain to recover a 50% drop, but the truth is that you need a 100% profit to recover a 50% loss.

Earning money on the way down allows us to buy high-quality stocks at massive discounts when other market participants lose a lot of their portfolio value or are severely damaged by margin calls. This can boost our portfolio valuation significantly and outperform the S&P 500 eventually.

What Is Delta Hedging?

Delta hedging is an options trading strategy that aims to reduce the directional risk of the underlying by creating a delta neutral portfolio.

Delta is the changes to options price with respect to changes in the underlying price.

The Black-Scholes formula was developed and discovered on the background of hedging using any kind of financial derivatives, not specifically related to option pricing only.

A perfect hedging strategy is achieved when the following Black-Scholes equation is satisfied:

- V = options value

- σ = IV

- S = stock price

- r = risk-free interest rate

On the left side of the equation, the first term consists of the time value, theta, of the option value, and a second term reflecting gamma, the convexity of the option value relative to the underlying value.

Gamma is the changes to delta with respect to changes in stock price. It is also the acceleration to options prices with respect to changes in stock price.

Convexity with respect to options refers to the fact that with each $1 move of the stock price, the option value changes exponentially. It can be said that the P/L of the derivative is quadratic to the underlying move.

Theta is negative because it reflects the time decay of the option's value, while gamma and vega are positively reflecting the rate at which the option's value changes relative to the underlying.

Theta is the changes to options value with respect to changes in time.

On the right side of the equation, the first term is the risk-free return of owning the options and the second term is a short position of the underlying.

Therefore, we can summarise that theta loss and gamma gain must offset each other in such a way that the result equals the return at the risk-free rate.

Theta + Gamma = Risk-Free Return on Derivative - Short Position on Underlying

A second principle is that the hedging only pays for itself when the gamma gains outpace theta decay.

You might notice there is no mentioning of delta in the formula. The total delta of the stock position must be offset by the options delta.

In such circumstances, we have performed volatility engineering resulting in a pure volatility position gaining in value due to gamma or vega expansion.

How to Use Gamma and Vega to Hedge Your Position?

When the hedging strategy is delta-neutral or delta hedged, it is not a directional but a volatility trade.

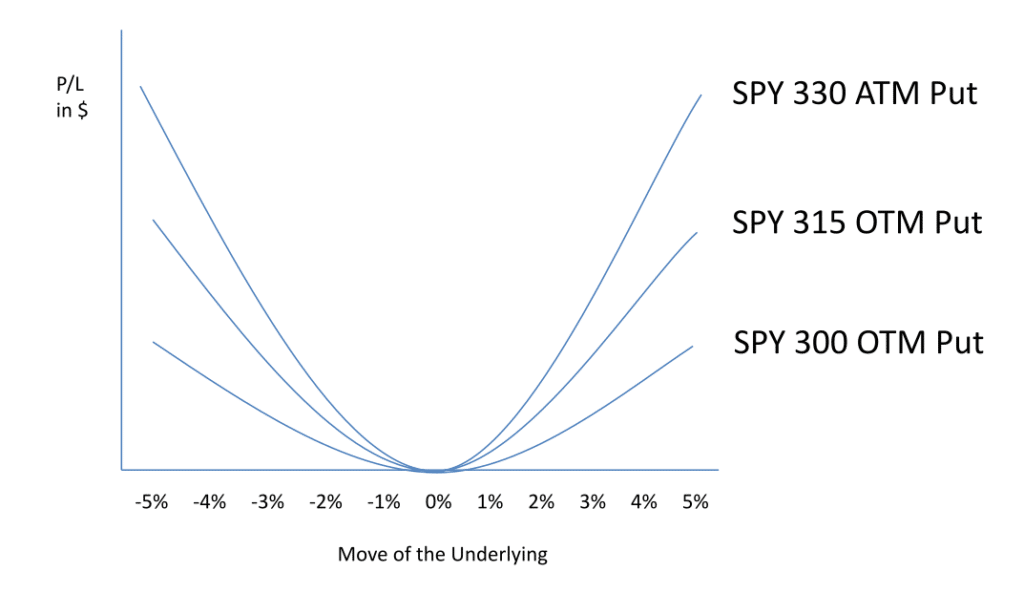

We can purchase ATM options to hedge the stocks with gamma and vega:

- Long Put options to hedge against long 100 shares.

- Long Call options to hedge against short 100 shares.

Long Put Options With Long 100 Shares

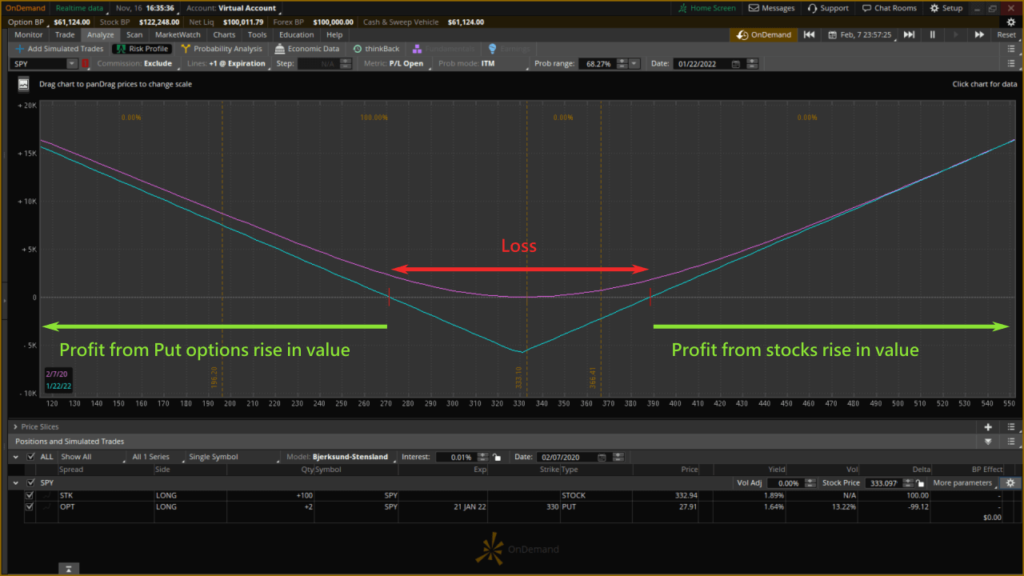

We can use the ThinkOnDemand feature in thinkorswim to turn back time 2020/2/8, just before the flash crash, to see the effects of a long Put hedge.

We simulate the purchase of 100 shares of SPY at $332.94 (100 delta), and then the purchase of two price-equal $330 SPY Put contracts to expire two years later on 2022/1/21 (roughly -100 delta).

| Options | Expiration date | Strike price | Bid | Ask | Delta | Gamma | Theta | Vega |

|---|---|---|---|---|---|---|---|---|

| put | 2020/3/20 | $330 | 5.71 | 5.72 | -0.49 | 0.03 | -0.07 | 0.46 |

| put | 2020/4/17 | $330 | 6.25 | 6.29 | -0.44 | 0.02 | -0.06 | 0.58 |

| put | 2020/6/19 | $330 | 9.54 | 9.56 | -0.45 | 0.01 | -0.04 | 0.8 |

| put | 2021/1/15 | $330 | 17.5 | 17.67 | -0.48 | 0.01 | -0.03 | 1.27 |

| put | 2022/1/21 | $330 | 26.87 | 27.83 | -0.49 | 0.01 | -0.02 | 1.81 |

As you can see from the option chain, the longer we go out in time for the same strike price, theta decreases and vega increases exponentially.

Vega is the changes to options value with respect to changes in IV.

We want to own as much vega as possible to offset theta when the volatility increases.

If we choose to buy OTM Put options for cheaper protection, we have to be aware that the extent of convexity decreases and hence less benefit from a volatility expansion.

So the combination of long 100 stocks and long 2 Puts gives us a near delta neutral position.

| Position | Delta | Theta | Vega | Gamma |

|---|---|---|---|---|

| 100 stocks | 100 | 0 | 0 | 0 |

| 2 ATM Puts | -99.07 | -4.80 | 360 | 1.25 |

| Total | 0.93 | -4.80 | 360 | 1.25 |

The theta of -4.80 means the Puts’ value decay -$4.80/day, while the vega is 360 and the gamma is 1.25.

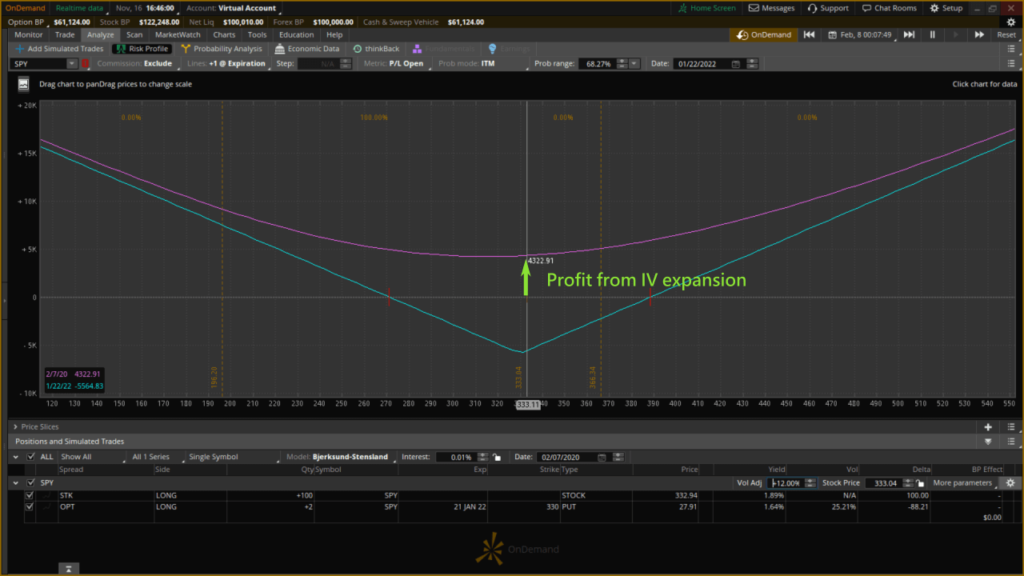

We have built a delta-hedged position, with a risk profile, analysed through thinkorswim, below.

The risk profile shows the convexity of the position. The portfolio earns money when SPY goes up (beyond $388) as well as when SPY drops (below $271). If the price remains unchanged at $330 when the options expire on 2022/1/21, the Put options expire worthlessly and we lose $5,582.

The reason we can potentially earn on both upside and downside is rooted in the fact that:

- When SPY climbs higher, our long position gains more than our Put option loses money.

- When SPY drops rapidly, the convexity of gamma causes the Put contracts to appreciate more than SPY long stocks lose value.

As you remember, Black-Scholes says that volatility must offset theta in a delta-hedged position to profit from hedging.

To demonstrate how the pure volatility position would affect the P/L chart, we increased volatility by 12% to simulate the IV increase during the 2020/3 crash.

Assuming that SPY price remained the same and we only benefit from rising volatility, we would have gained $4,322.91 through vega expansion.

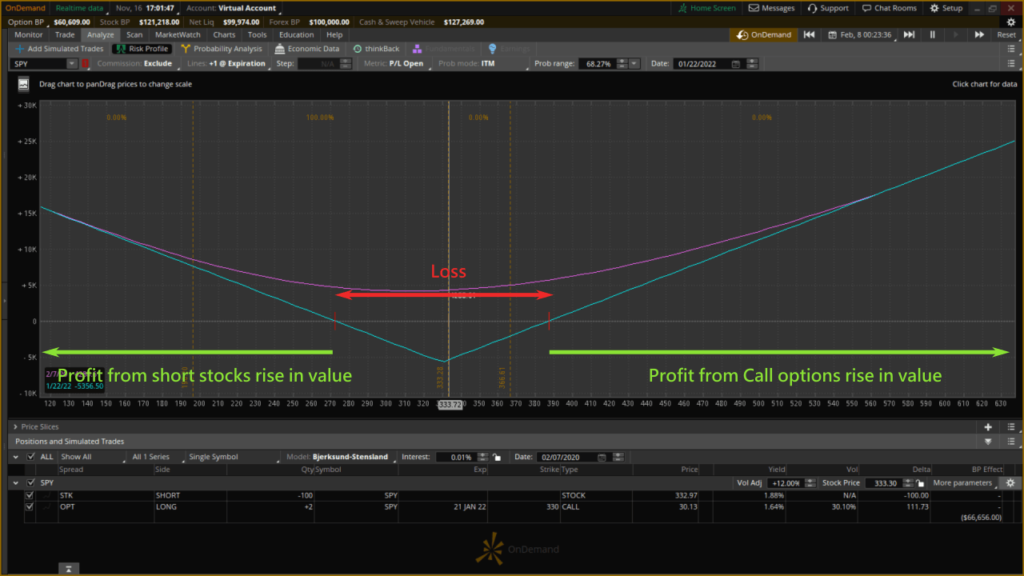

Long Call Options With Short 100 Shares

Shorting 100 SPY shares and offset delta by buying 2 long-dated Call options result in the same convexity chart and almost the same profit due to the expansion of volatility.

When the market drops, our SPY shares drop faster than the Call option loses value, and when the market climbs up our Call option gains more value than our shorted SPY shares lose money.

We earn money as long as volatility offsets theta decay for any delta-hedged position.

The reasons for buying Put or Call options that expire more than 1 year away to offset portfolio delta:

- The longer the expiration, the higher vega will be, so any increase in IV lead to higher options value in the future, contango.

- Theta is low giving our hedge more time and a higher probability of success.

So, buying options that expire 1-2 years out in the future allows us to benefit materially from any significant volatility expansions within that timeframe. On the other hand, near-dated SPY options have low vega and have high theta, giving us less time to hedge and a lesser probability of success.

We also like to buy these long-dated options during low market volatility at a low price before a market crash.

Simulation of Hedging During the 2020 COVID-19 Flash Crash

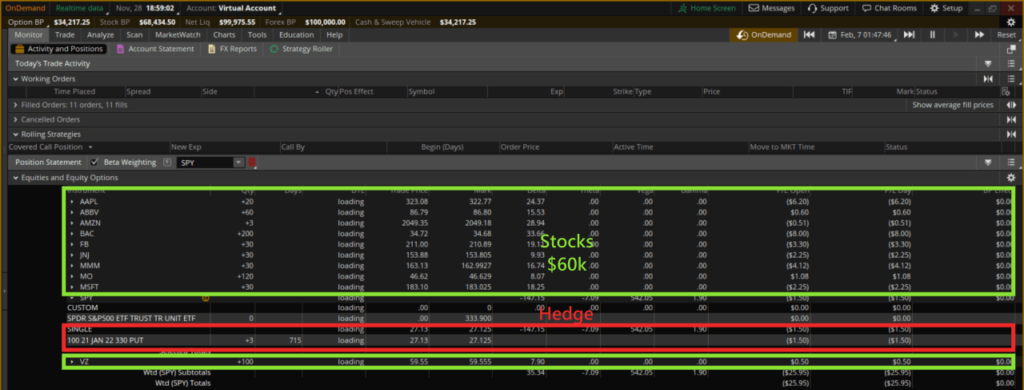

Let us simulate a $100k account in 2020/2/7 with a $60k portfolio in growth stocks (30%) and dividend stocks (70%).

| Stocks | Stock price | Quantity | Position |

|---|---|---|---|

| AAPL | $323.08 | 20 | $6,461.60 |

| ABBV | $86.79 | 60 | $5,207.40 |

| AMZN | $2049.35 | 3 | $6,148.05 |

| BAC | $34.72 | 200 | $6,944.00 |

| FB | $211.00 | 30 | $6,330.00 |

| JNJ | $153.88 | 30 | $4,616.40 |

| MMM | $163.13 | 30 | $4,893.90 |

| MO | $46.62 | 120 | $5,594.40 |

| MSFT | $183.10 | 30 | $5,493.00 |

| VZ | $59.55 | 100 | $5,955,00 |

| Total | $57,643.75 |

The remaining $40k could be used to hedge and protect our portfolio during the 2020 flash crash.

After beta weighting the delta of all positions with SPY, we could neutralise delta by buying 3 contracts of $330 SPY Put options expiring on 2022/1/21, which cost around $8,139.

Cost of 3 SPY $330 Puts (expiring in 2022/1/21) = $2,713 x 3 = $8,139.

The nominal value of the 3 SPY Puts, $99,000, provides more than 165% protection for our $60k portfolio.

Nominal value of 3 SPY Puts = $330 x 300 = $99,000

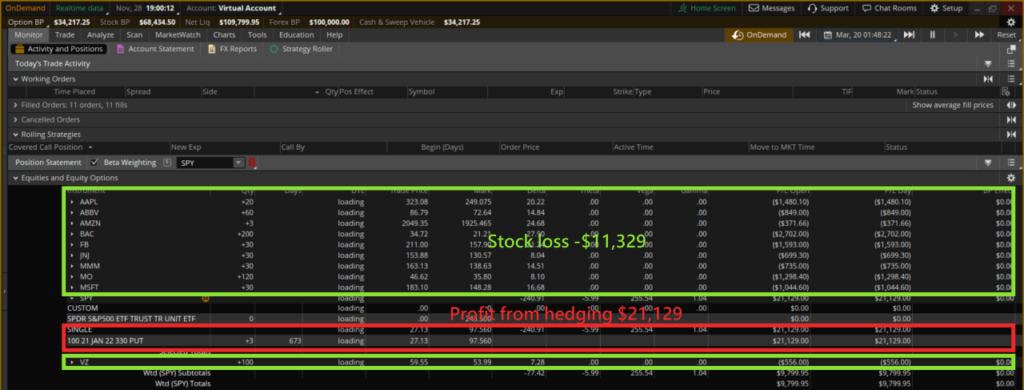

When 2020/3/30 rolled around, the investment portfolio dropped around $11,329 in value, while our Put options resulted in a gain of $21,129. The total account value increased by $9,799.95, around 16%, when the market dropped more than 40%!

All our positions lost significantly during the market crash but the losses were more than offset by the gains of the hedging Put options. The profits allow us to aggressively buy high-quality stocks at massive discounts.

The table below shows the relationship between the level of protection and the P/L after the crash.

| Level of protection | 0% | -5% | -10% | |||

|---|---|---|---|---|---|---|

| Strike price | $330 | $315 | $300 | |||

| P/L after market crash | Cost of Put | P/L after market crash | Cost of Put | P/L after market crash | Cost of Put | |

| 1 Put - about 50% of portfolio | -$2,300 | $2,713 | $-3,000 | $2,190 | -$3,400 | $1,750 |

| 2 Puts - about 100% of portfolio | $4,500 | $5,426 | $3,300 | $4,380 | $2,300 | $3,500 |

| 3 Puts - about 150% of portfolio | $9,800 | $8,139 | $9,500 | $6,570 | $8,000 | $5,250 |

| No protection | -$11,329 |

To minimise the cost of hedging, we suggest a 100% portfolio value is sufficient at a -10% level of protection. Generally speaking, we want to be protected against catastrophic events such as the 2020 market crash and are less concerned about 5%-10% market corrections.

Hedging Adjustment Tips

Once you have incorporated the Put options into your portfolio, you have to manage them actively to stay protected.

When the market climbs higher you have to roll the options upwards, usually to the next month. If you don’t move the Puts upward, your level of protection decreases and kicks in later than you intended.

When the market drops the first 5% and pierces through your strike price, you should roll the 2 year DTE Put in to 1-2 months DTE for a net profit. In this case, you would have cashed in the first gains from vega expansion (vega scalping). As the market continues to make significant moves lower, we can benefit from the gamma expansion (gamma scalping) when the Puts become more valuable ITM. The other reason is that we don’t want to give up our vega gains once the market starts rebounding.

If the bearish trend leads the market to be down 30-40%, you can consider closing your Puts before theta causes more decay. If the market moves in the normal ranges of pullbacks and corrections, you roll in, roll out, roll up and roll down as needed, to take advantage of vega scalping and gamma scalping repeatedly.

For example, when SPY dropped to $316 (-5% from $333) by 2020/2/27, our Put options’ value increased from $27 to about $48. We could then roll in and down the Put from the strike price of $330 to $315, and shorten the expiration from 2 years to 2020/3/20, a month away. This roll would be profitable for a net credit of $29 per Put option.

By 2020/3/29, the $315 Put option price had increased from $17 to $76, resulting in a total gain of $49 + $29 = $78 per Put option.

Total gain of rolling 3 Puts = $78 x 100 x 3 = $23,400

If we did not roll in the expiration of the original 2022/1 Puts, the Puts value would only become $96 per contract on 2020/3/20.

Total gain of 3 unrolled Puts = ($96 – $27) x 100 x 3 = $20,400

Due to rolling in and exposing our Put options to gamma scalping, we earned an additional $3000 and prevented us from giving up gains on the rebound of the SPY.

How to Finance the Hedge?

The 3 Put options cost us $8,139 to protect our portfolio for 24 months. If the market doesn’t go down, the cost of the hedging strategy is spent.

One way to finance the hedging strategy is to use the wheel strategy to offset the monthly decay of $339.

Monthly decay of Put options = $8,139/24 = $339.125

High Probability Bearish Trades Right Now

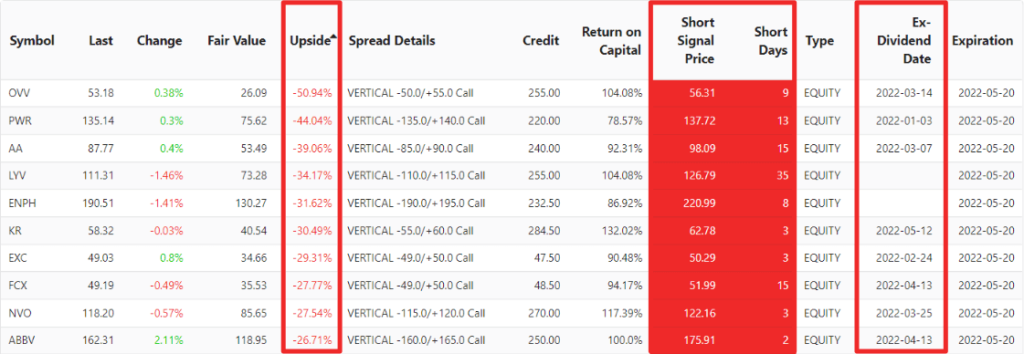

The Bear Call Spread Screener uses chart analysis to find overvalued stocks with a high probability of a downward correction that we can sell Bear Call Spreads to open.

We want to find heavily overvalued underlying that have a high probability of going down.

- The options screener uses fundamental analysis to calculate the Fair Value of the underlying then compare that with the Last value to find the potential Upside of the stock. When the Upside is less than -30%, we have high confidence in a bearish outlook.

- Short Signal Price shows the topped out price from our technical analysis. So we know the stock price will not rise beyond this price in the short term.

- Short Days indicate the number of trading days has passed since the last short signal. As soon as the short signal appears, there is a high probability of a bearish move.

- We also need to avoid Ex-Dividend Date before options expiration. On one hand Ex-Dividend Date usually lead to rising prices and assignment. On the other hand, if you get assigned, you might need to pay dividends for shorting the stock.

Since we are strongly bearish about our trade, we can use -0.50 delta ATM Bear Call Spread to calculate Return on Capital. This gives us the highest return when we are right, and the lowest maximum loss if we are wrong.

So we can look at the screener for the best ATM Bear Call Spread ideas.

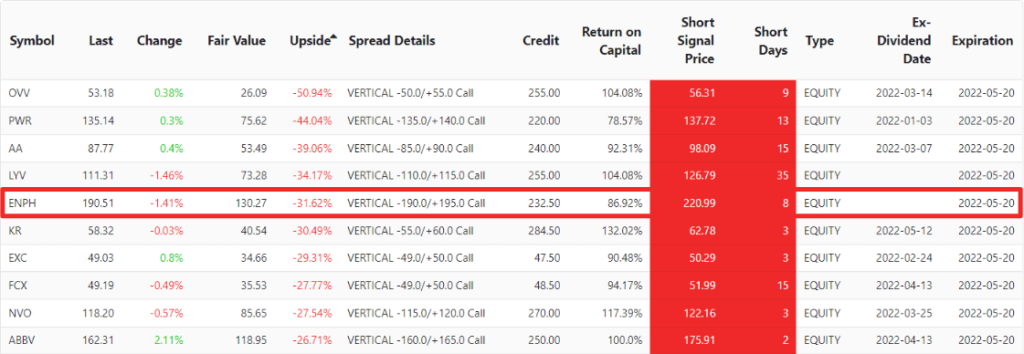

By combining Upside and Short Days, we see ENPH is one of the most overvalued stocks, and has a short signal 8 trading days ago. It doesn't have an Ex-Dividend Date coming up. So it has a high probability of a bearish trend.

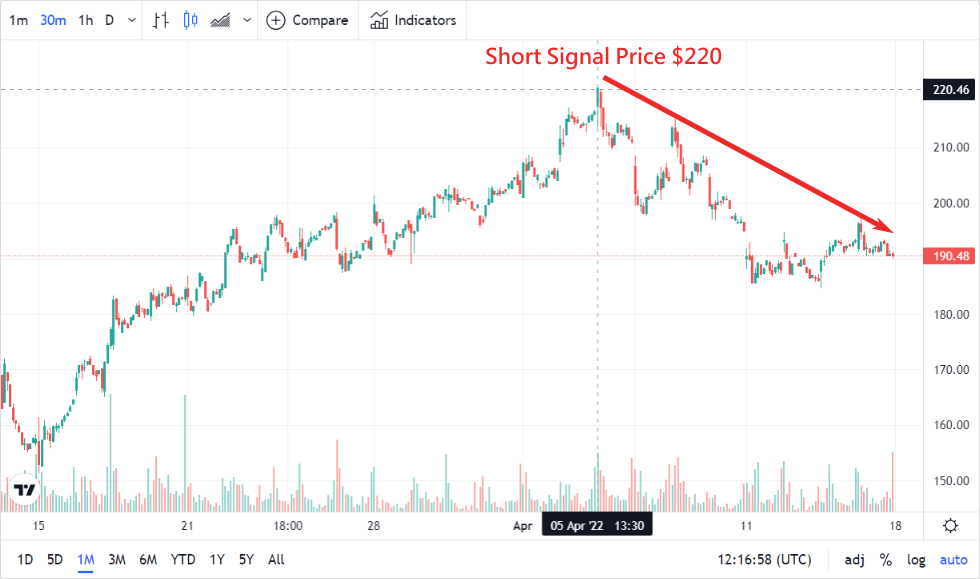

By checking the Enphase price trends, we confirm ENPH reached a high point at $220, similar to the Short Signal Price in our Bear Call Spread list, 8 trading days ago, and has been bearish ever since. We expect ENPH to stay below Short Signal Price in the short term.

We can sell an ENPH ATM Call Spread option that expires in 35 days. If the ENPH stock price does not rise before expiration, we have the potential to profit 86% from the trade.

SlashTraders vs S&P 500: 450% Outperformance, Verified Trades and How to Copy Every Alert

If the market climbs higher, roll the options upwards, usually to the next month .... can you give an example.

By rolling, you close the losing option contract, and open a new option with a longer expiration.

The longer expiration usually has a higher premium to offset the loss from closing the previous contract.

Check out this post for more details. https://slashtraders.com/en/blog/roll-options/

Now it's clear. Thank you, Tony. This helps a lot.

It turns out that delta can be used to hedge portfolios.

Thank you, sir.

Yes, as long as you do a good job of hedging, you won't be afraid of a big drop in the stock market.

Thank you for providing such a clear and good hedging instruction.

Finally, we know how to protect our long-term investments.

That's right.