Do you know even if the stock price doesn't move, you can still profit by trading options?

If you combine selling Put and Call options, you can define a range that the stock prices can move while still make a profit.

Today, SlashTraders will show you how to use the Options Scanner to find high probability and high profit Strangles options strategies, so you can trade neutral options strategies with confidence.

Contents

What Is the Strangle Options Strategy?

A Strangle options strategy works by selling a naked Put and a naked Call to define a range you can profit from. As long as the underlying price does not exceed or drop below the strike prices of Put and Call before expiration the two options contracts will depreciate and we profit as an options seller.

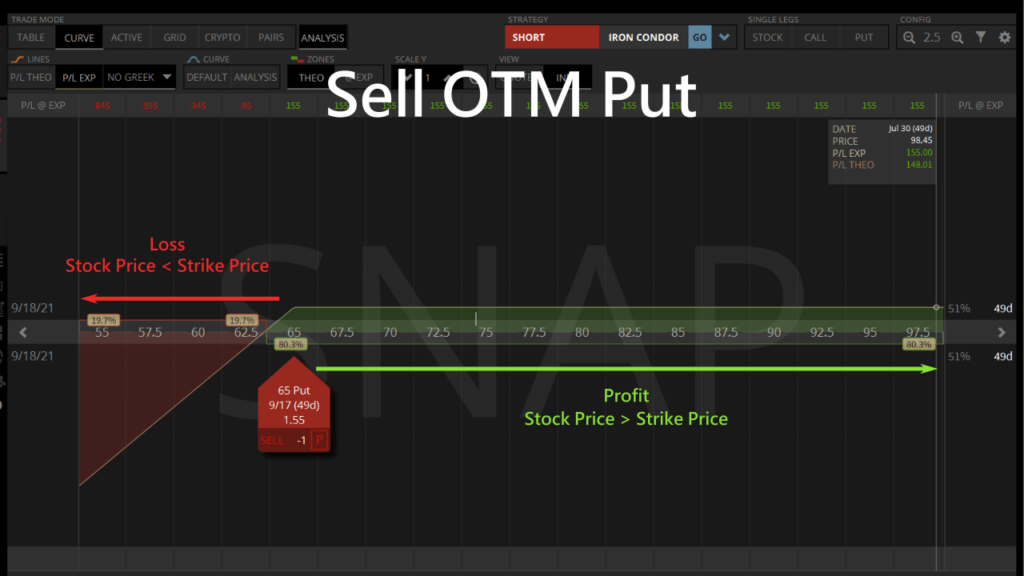

Let's recall the profit analyses of selling OTM Put and OTM Call options. We receive a premium when we sell the OTM Call. If the underlying price doesn't increase, the Call option value will depreciate and we earn a profit.

But if the stock price increases beyond the Call strike, the maximum loss is infinite.

We also receive a premium when we sell an OTM Put option. If the underlying price doesn't drop, the Put option value will depreciate and we earn a profit.

But if the stock price decreases below the Put strike, the maximum loss is infinite.

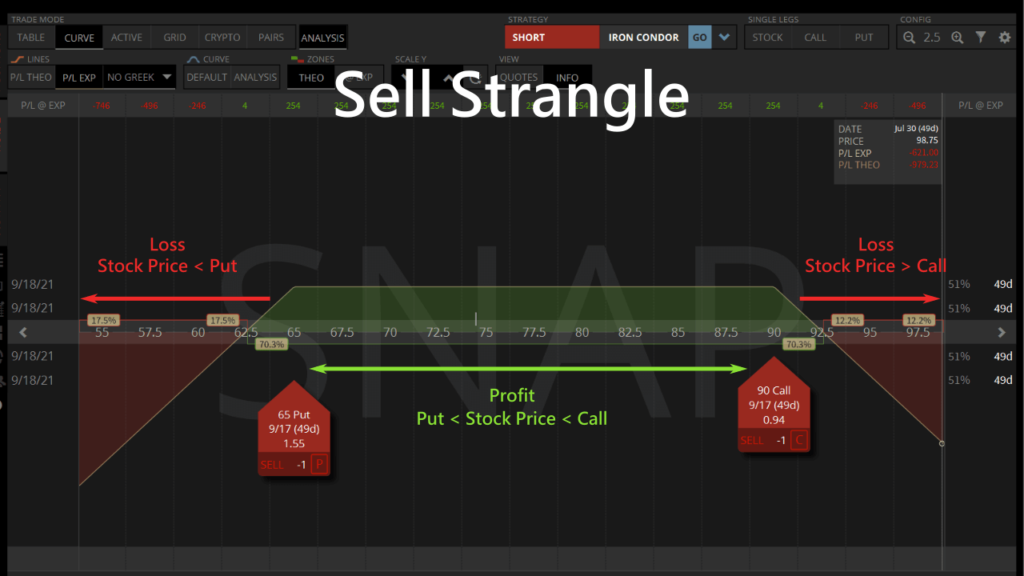

When we combine selling an OTM Call and an OTM Put we get a short Strangle strategy. The Put strike defines the lower boundary of the price movement, while the Call strike defines the upper boundary of the price movement.

If the underlying stock price doesn't move beyond the boundaries, the short Strangle will be profitable.

Is Short Strangle Risky?

A short Strangle is made up of a short naked Put and a short naked Call, so the short Strangle is similar to a short Straddle. So the risk of a short Strangle is that it can have unlimited losses when the stock price rises or falls in a big way.

| Price direction | Maximum loss to a short Strangle |

|---|---|

| Bullish | Unlimited |

| Bearish | Strike price x 100 - premium |

What Are the Key Points to Profitable Short Strangles?

When selling Strangles, we want both theta and vega to depreciate the options prices, so we can sell high price Strangles to open, and buy low price Strangles to close.

Theta is the changes to options value with respect to changes in time.

From our experience, selling options with more than 30 days to expiration have a consistent time value decay, and the gamma risk is lower. So we can be patient and earn a profit as time passes.

Vega is the changes to options value with respect to changes in IV.

Since we want to sell high and buy low, we need to sell to open at high IV, then buy to close when vega causes the option's value to decay at low IV.

We also need to find underlying opportunities with underrated volatilities. We can do that by picking stocks with price trends that rarely exceed Bollinger Bands, and also stocks with high market capitalisation to reduce the risk of manipulation.

If the Strangle is losing near expiration, we can consider rolling the Strangle to a later date to offset the losses with extra premium. Then we can patiently wait for our trade to become profitable.

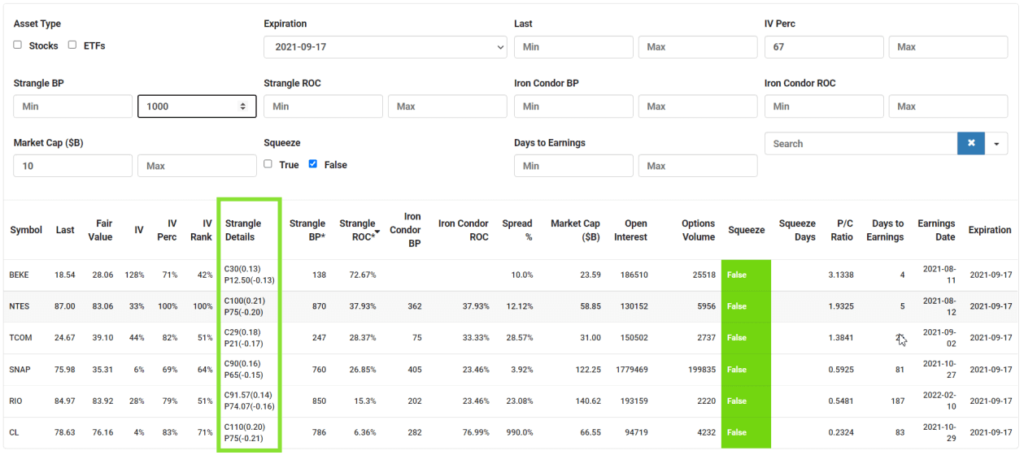

Options Scanner Settings to Find the Best Short Strangle Opportunities

SlashTraders' Options Scanner is designed to find high probability and high return Strangles in seconds. Here are some tips to use the filtering function to find the best short Strangle entry points.

- We want to choose opportunities with longer than 30 DTE to get the safest theta decay.

- IV Perc is the relative position of current IV compared to the range of IVs in all the trading days in the previous year. We can filter IV Perc >67% to find stocks with IV higher than 2/3 of trading days in the past year. So they have a high chance of contracting IV and vega in our favour.

- Open Interest is the number of the total number of outstanding derivative contracts for the underlying. We can find stocks with Open Interests >100,000 to make sure the liquidity is good, so we get our trades filled easily.

- By choosing Market Cap ($B) larger than 10 billion, we avoid choosing stocks that can get manipulated and explode like GME.

- A good idea is to eliminate stocks with depressed price movement, because IV will expand soon after. So we need to choose Squeeze status as False.

- To further reduce risks, we can limit the Strangle BP to less than $1000, so we can easily diversify our portfolio.

Finally, we can sort the Strangles ROC by descending order to get a shortlist of the highest return Strangles.

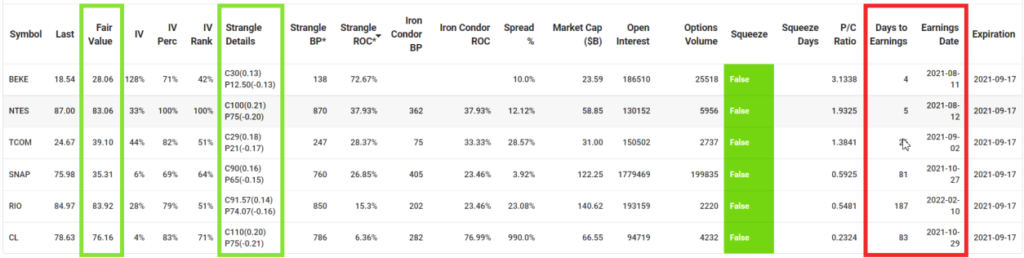

The Best Short Strangle Options Right Now

You can see the Fair Value and Earnings Date for every underlying to help us fine-tune the selection and get the best entry points.

If the Fair Value is very close to the strikes listed in the Strangle Details, we can be even more confident that the Strangles will be profitable.

Earnings Date is an event that can cause large price movements, so we want to avoid selling neutral options strategy past Earnings Date.

We can see the top 3 stocks with highest return have upcoming Earnings, so selling Strangles for them are quite risky.

SNAP's Fair Value is on the low side, but considering that SNAP has a robust social media platform like FB, consider selling SNAP's Strangles option.

If we sell to open a Strangle for SNAP that expires in 40 days, it has a 27% maximum return if SNAP stock price does not exceed the Put and Call strike prices before options expiration.

SlashTraders vs S&P 500: 450% Outperformance, Verified Trades and How to Copy Every Alert

I don't understand "we can look at selling Strangles to SNAP because the Fair Value is close to the 0.20 delta strikes ". In the example SNAP's FV is 35 but the C and P strikes are 90 and 65 respectively. The strikes are way above the FV.

Hi, thank you for pointing out the typo. I've corrected the wording.

You are correct about how we should use FV, ideally, we need an FV within the 0.20 delta strikes.

Tony, how to find profitable options using your scanner for 1-2 weeks?

As our scanners are optimized for monthly option trades, you can use the scanners to pick good symbols to trade, then play around the weekly settings in your platform of choice.

How to find out options for monthly that may be profitable?

A good way is to use the options scanner to find high IV symbols that have a high chance of contracting IV in the future

Then you can sell monthly Strangles to take advantage of the IV contraction

How to find out short strangles for 2 weeeks or for 1 week using your scanner?

I'm afraid we don't trade 1-2 week short Strangles, so you can't find that in our scanner.

Even though 1-2 week short Strangles have good theta decay, but.

-They have big gamma risks, so small fluctuations in stock price can impact the P/L a lot.

-The strike prices have to be very close to market price, making them very risky.

So we don't advise trading 1-2 week short Strangles.

I was afraid to trade Strangle before, thank you for sharing such a good way to trade Le Choice!

I finally found a good Strangle option pattern.

That's right, sell Strangles options whenever you find a stock that shows signs of IV contraction.

Thank you for such a great strangle option strategy!

Thank you for your kind words

hello, what do you think are the differences between iron condors and strangles?

Well, first things first, Iron Condors have limited losses while Strangles have unlimited losses.

So when the trades go wrong, Strangles can lead to larger losses if not closed in time.

That being said, Strangles are easier to repair when a trade goes "a little bit wrong".

Since Strangles only have 2 legs, it's easier to "roll" a losing trade to the future, and use the time value to Since Strangles only have 2 legs, it's easier to "roll" a losing trade to the future, and use the time value to cover your current losses, sometimes even allowing you to widen the strikes for a higher probability to profit.

So we prefer to trade Strangles with good theta and vega opportunities with low buying power to keep the risks low.

For higher value stocks, >$100, we prefer to trade Iron Condors.