Strangle is a neutral options strategy that profits from a lack of stock price movement.

If the stock price fluctuates beyond our expectations, there are a few adjusting strategies that can help us repair the losing Strangle by increasing credits received to offset the losses. Then we can patiently wait for the stock price to revert back to our range of profitability.

What Is Strangle?

A Strangle is the combination of a short Put and a short Call to create a neutral strategy. The trade is profitable if the stock price doesn't change very much.

The short Put defines the lower boundary of the stock price. The short Call defines the upper bound of the price movement.

As long as the stock price stays between the strike prices, the Strangle options will expire worthless, resulting in profit for the options seller.

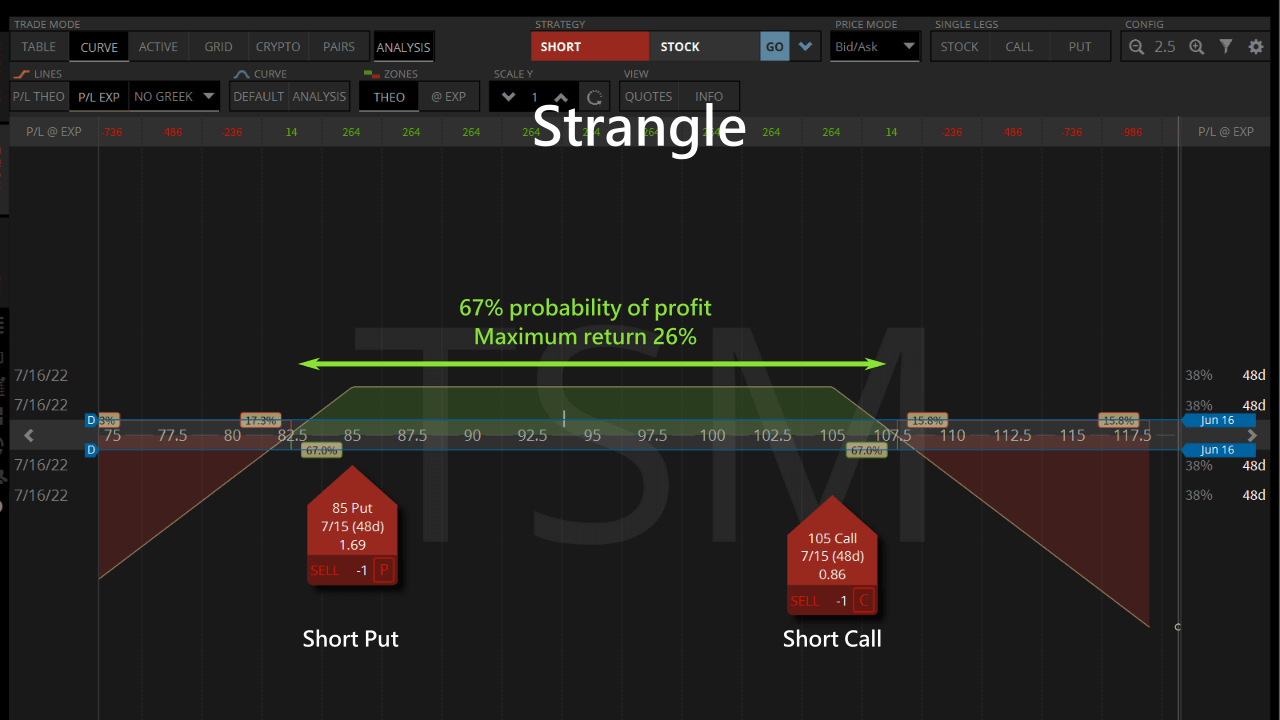

We can see a 0.20 delta TSM ADR Strangle that expires a month and a half later has a 67% probability of profit, and has the highest return on capital of around 26%.

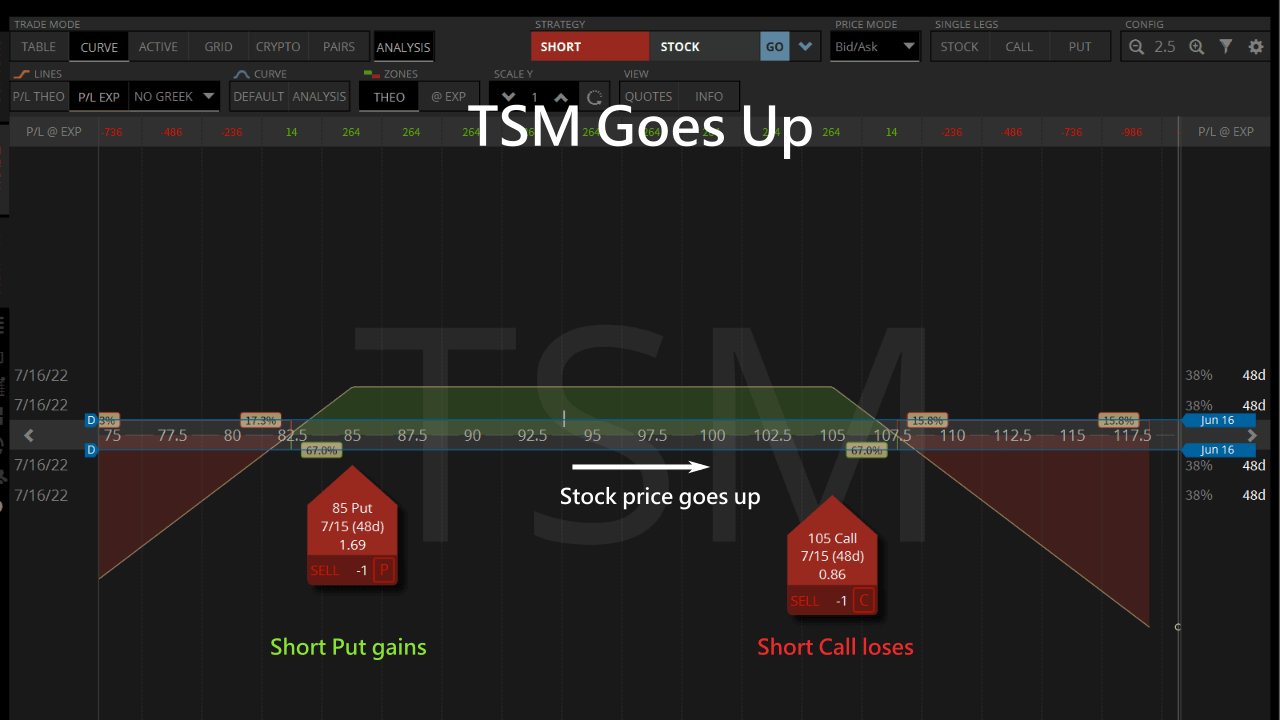

Roll Up Put After the Stock Price Goes Up

If the stock price goes up before the Strangle expires, we can roll up the profitable short Put option to pocket the profit.

In the TSM Strangle example, when the TSMC stock price goes up, our short Put becomes profitable due to a lower delta. While the short Call on the other side loses because of an increase in delta.

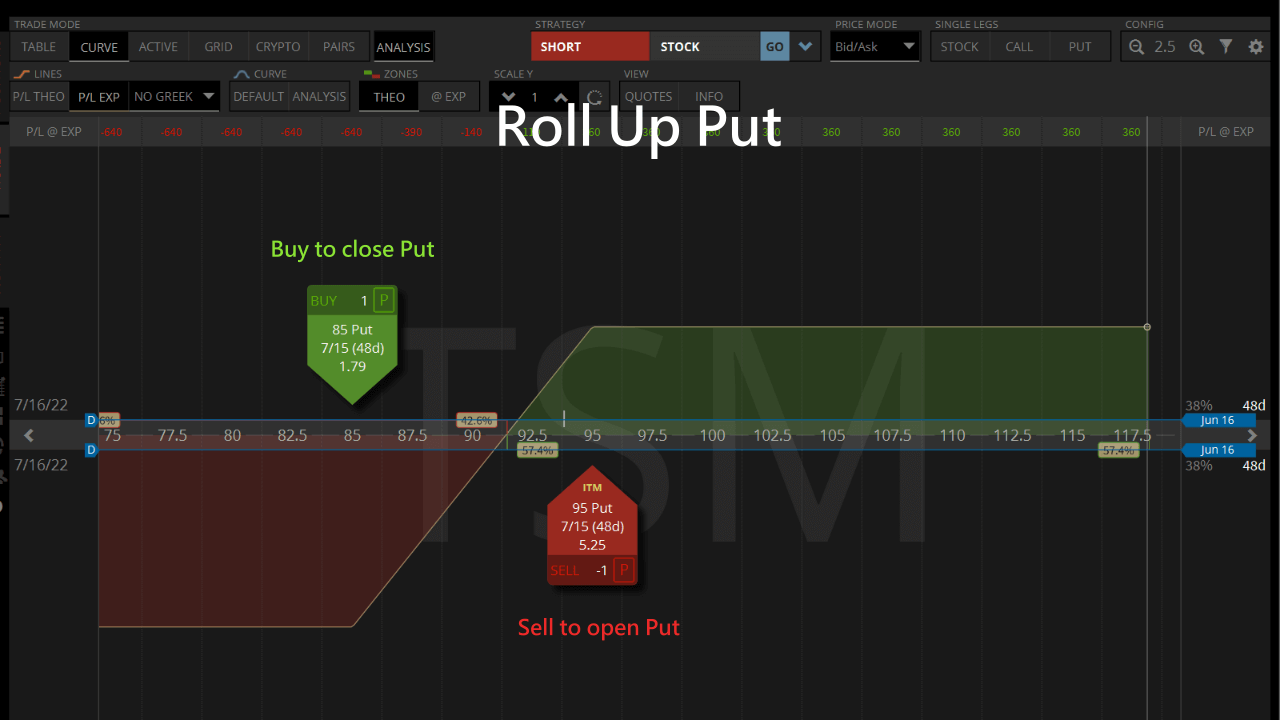

We can roll up the Put option to collect some profit first:

- Buy to close the Put option.

- Sell to open another Put option that expires at the same time at a higher strike price.

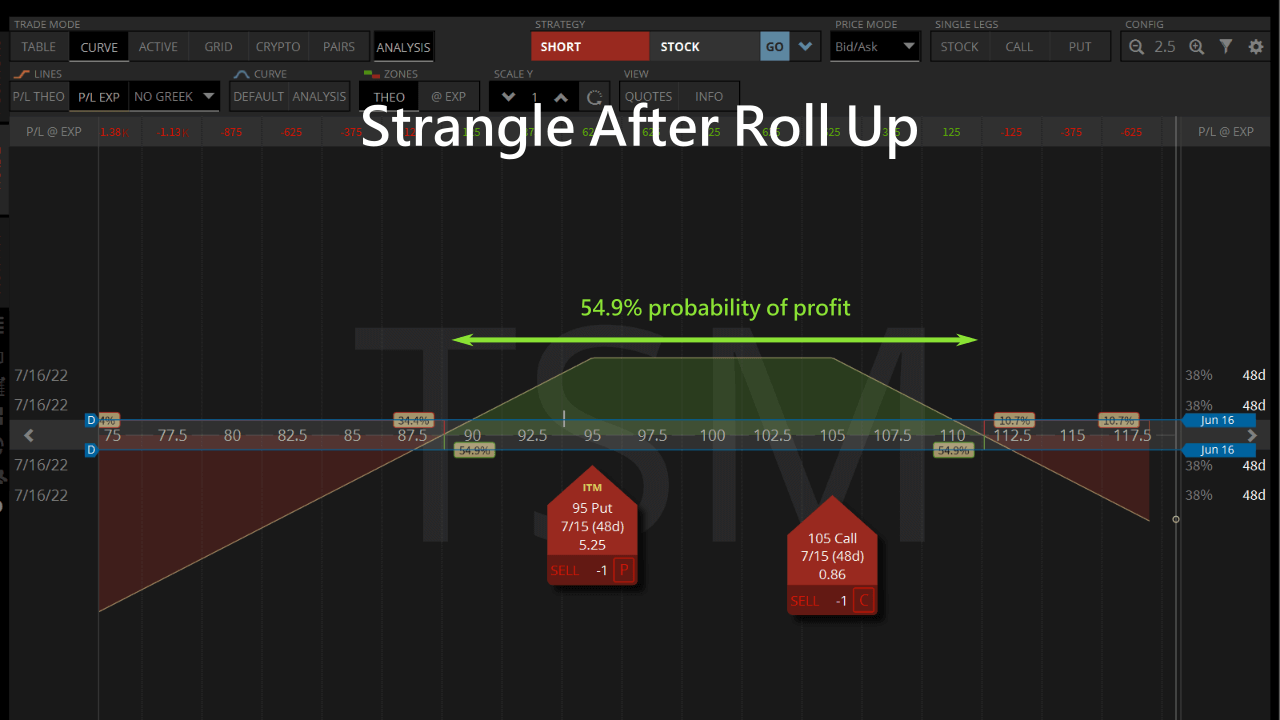

After rolling up, we create a Strangle with a smaller profitable width, allowing us to continue to benefit from theta decay.

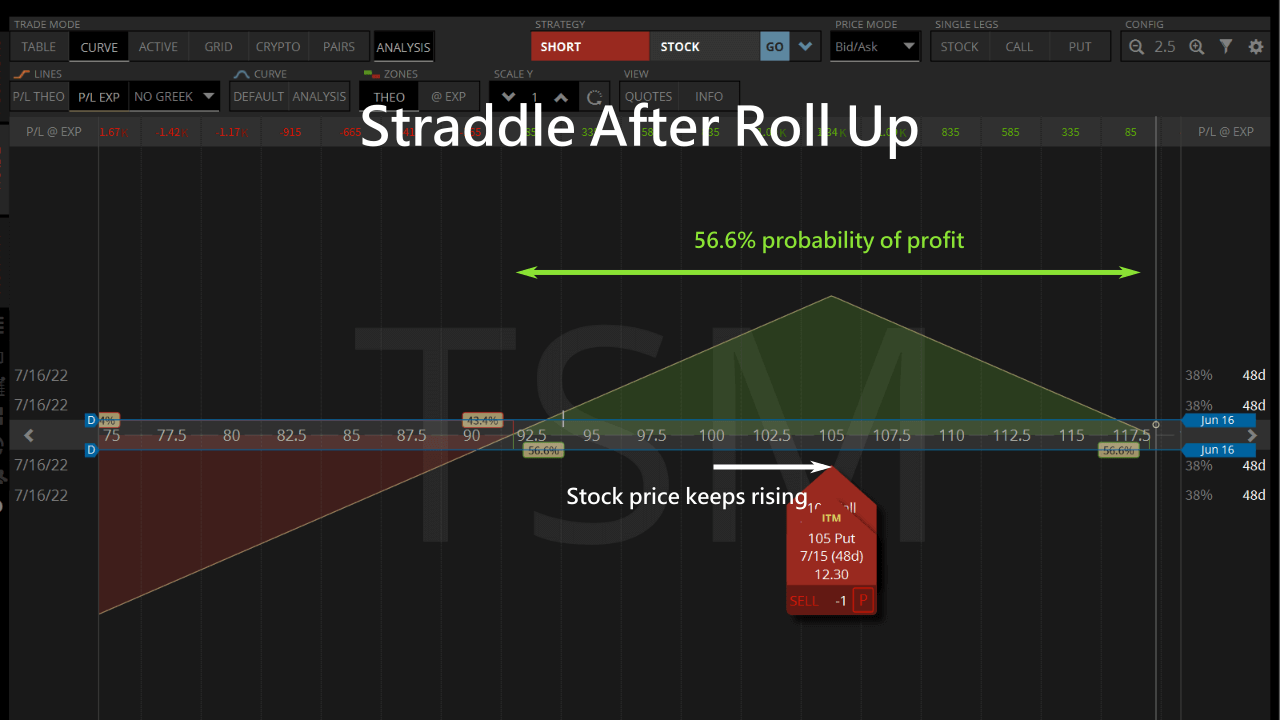

If the stock price continues to rise, we create a Straddle after rolling up the Put a few times.

Then the profitable range would be defined by the premium received. We can close the trade for profit if the stock price remains within the range before expiration.

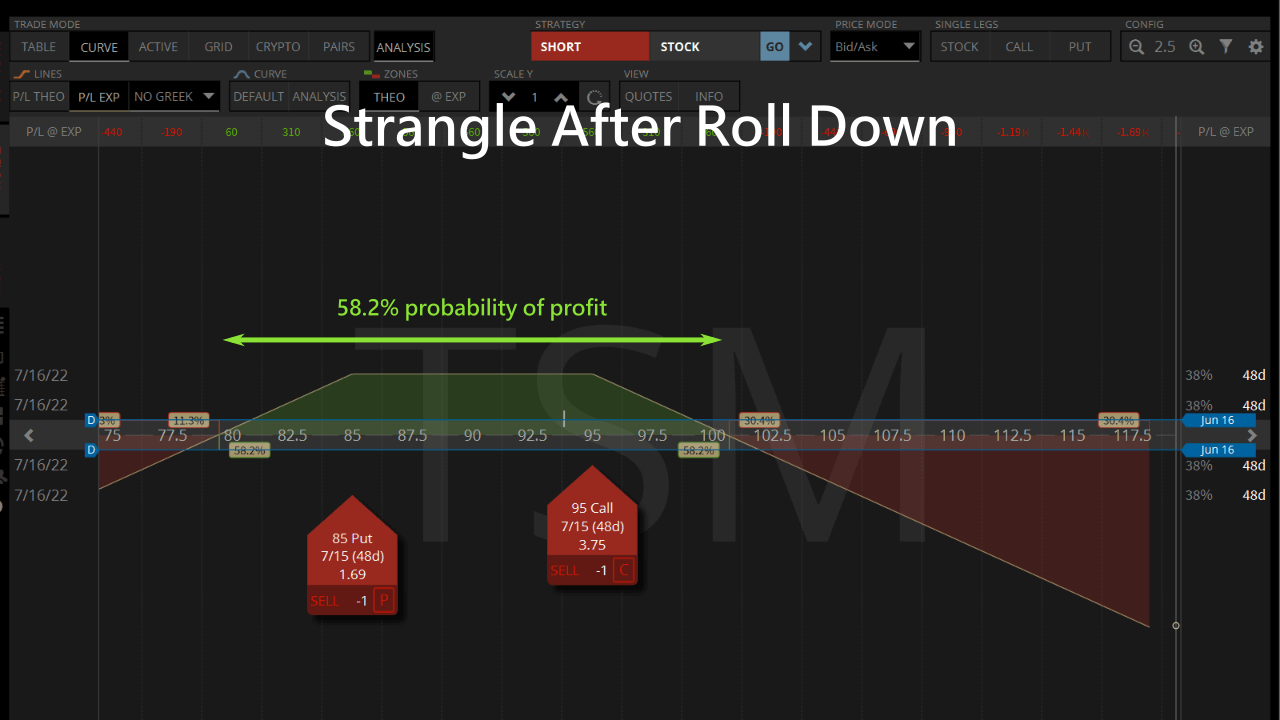

Roll Down Call After the Stock Price Goes Down

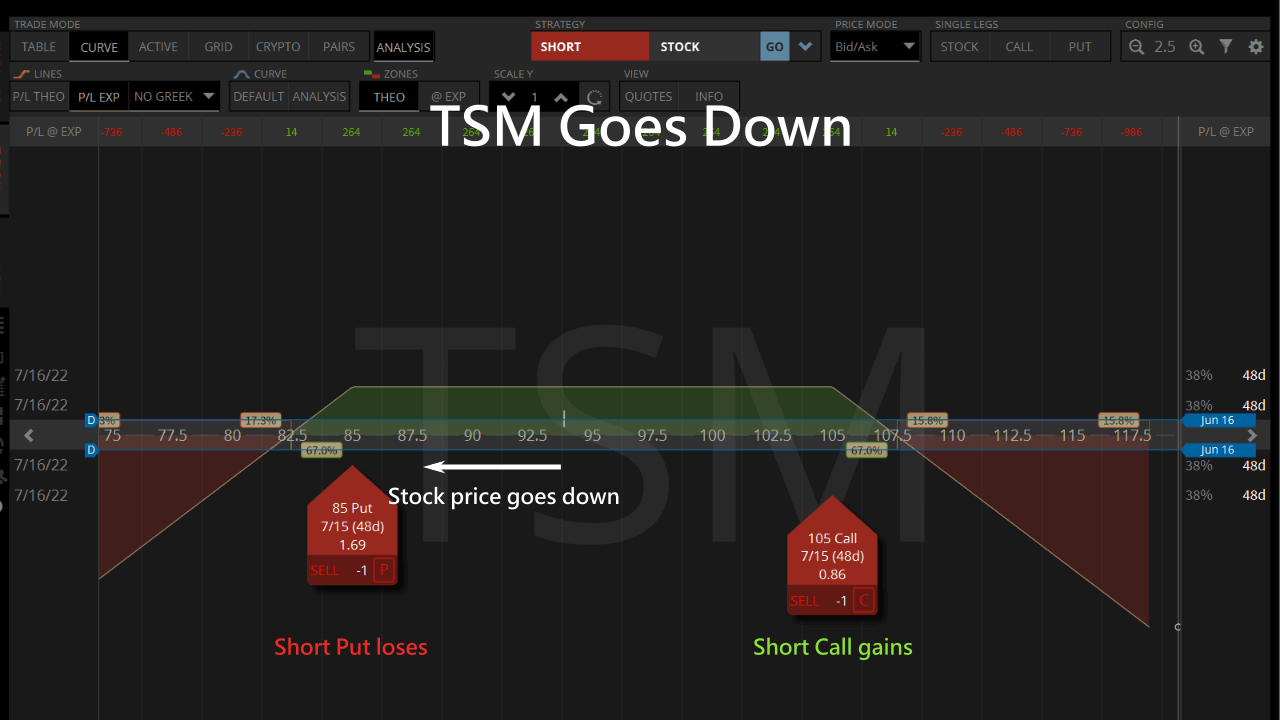

If the stock price goes down before the Strangle expires, we can roll down the profitable short Call option to pocket the profit.

If the TSMC stock price goes down, our short Call becomes profitable due to a lower delta. While the short Put on the other side loses because of an increase in delta.

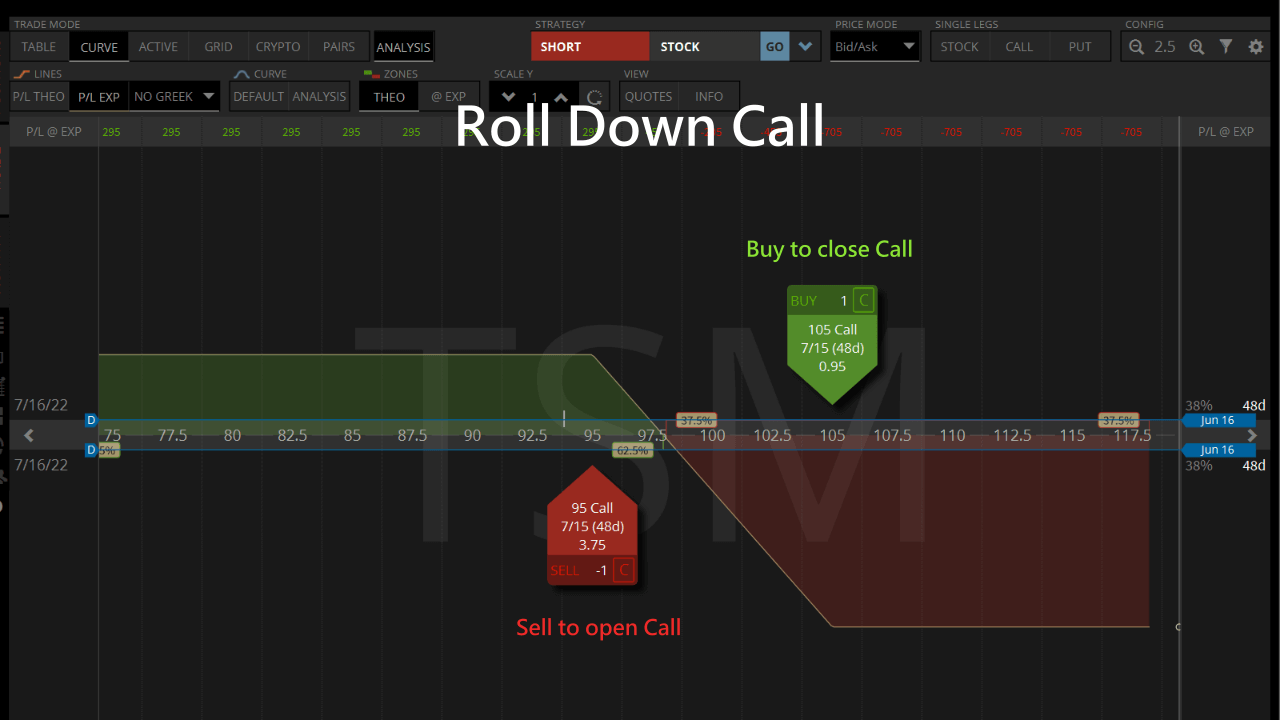

We can roll down the short Call to collect our profit:

- Buy to close the Call option.

- Sell to open another short Call that expires at the same time at a lower strike price.

After rolling down, we have a Strangle with a smaller profitable range, allowing us to continue to benefit from theta decay.

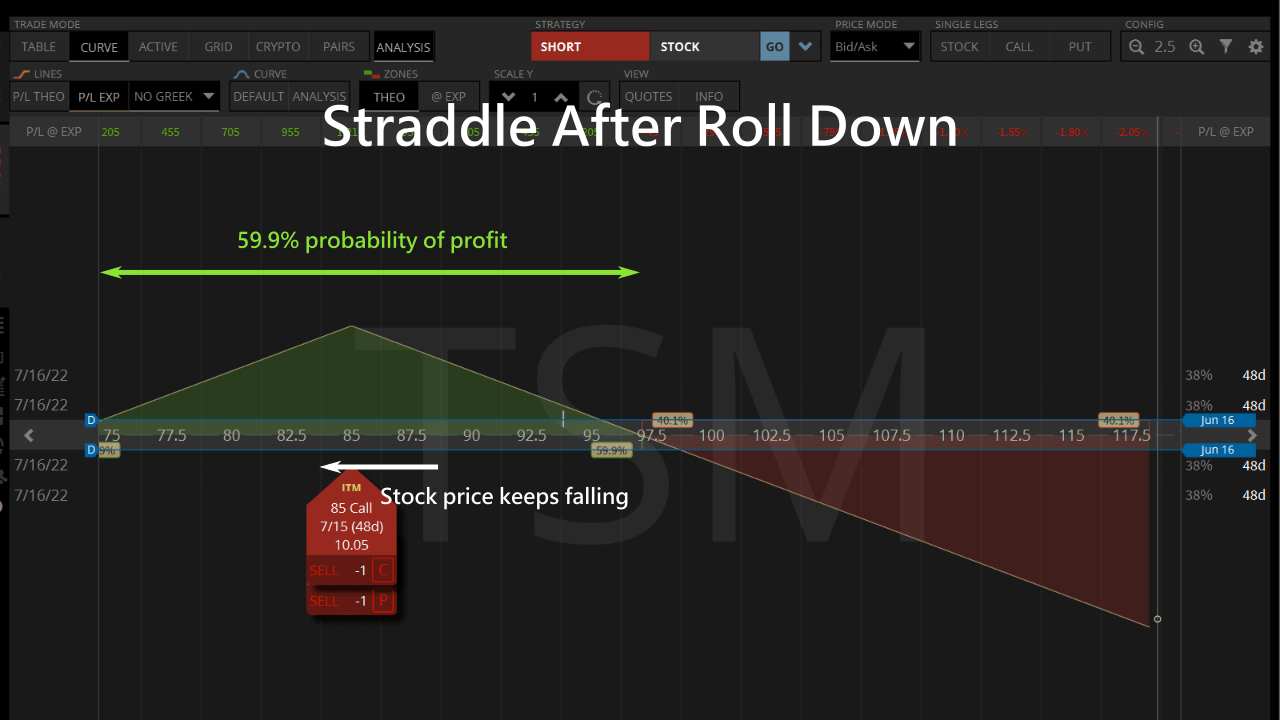

If the stock price continues to fall, we create a Straddle from the Strangle after rolling down the short Call a few times.

Then the profitable range would be defined by the premium received. We can close the trade for profit if the stock price remains within the range before expiration.

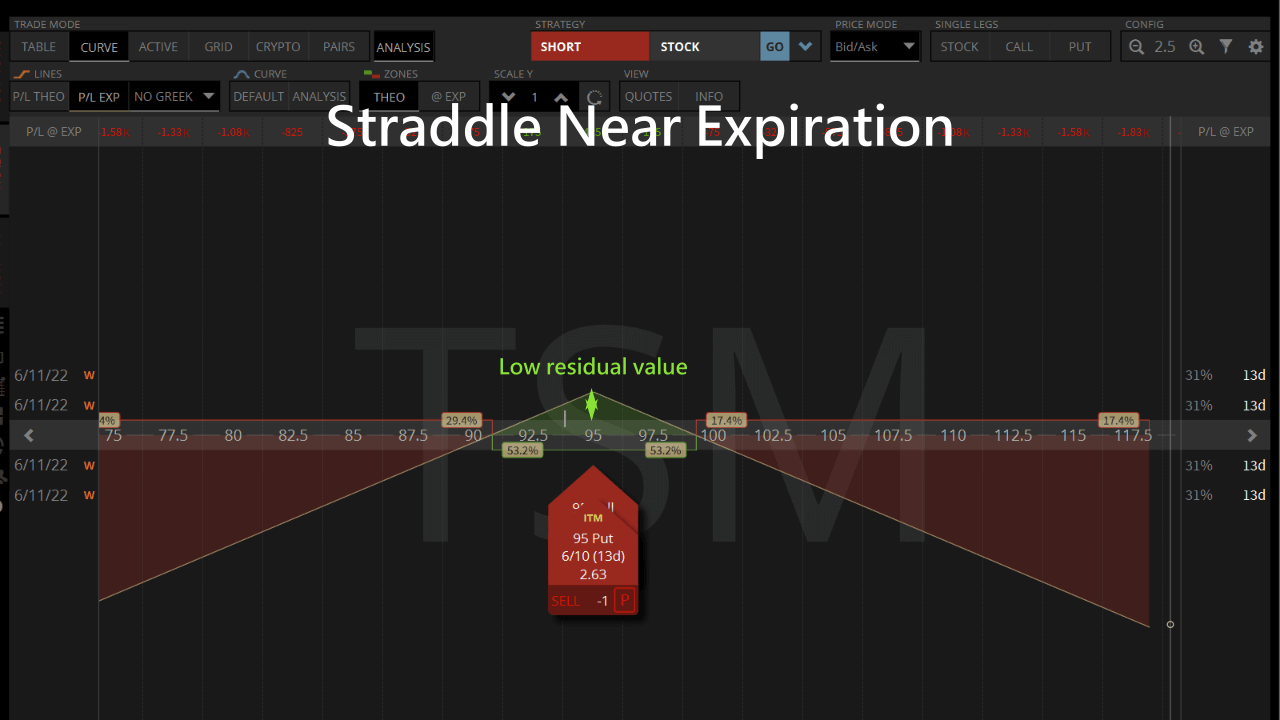

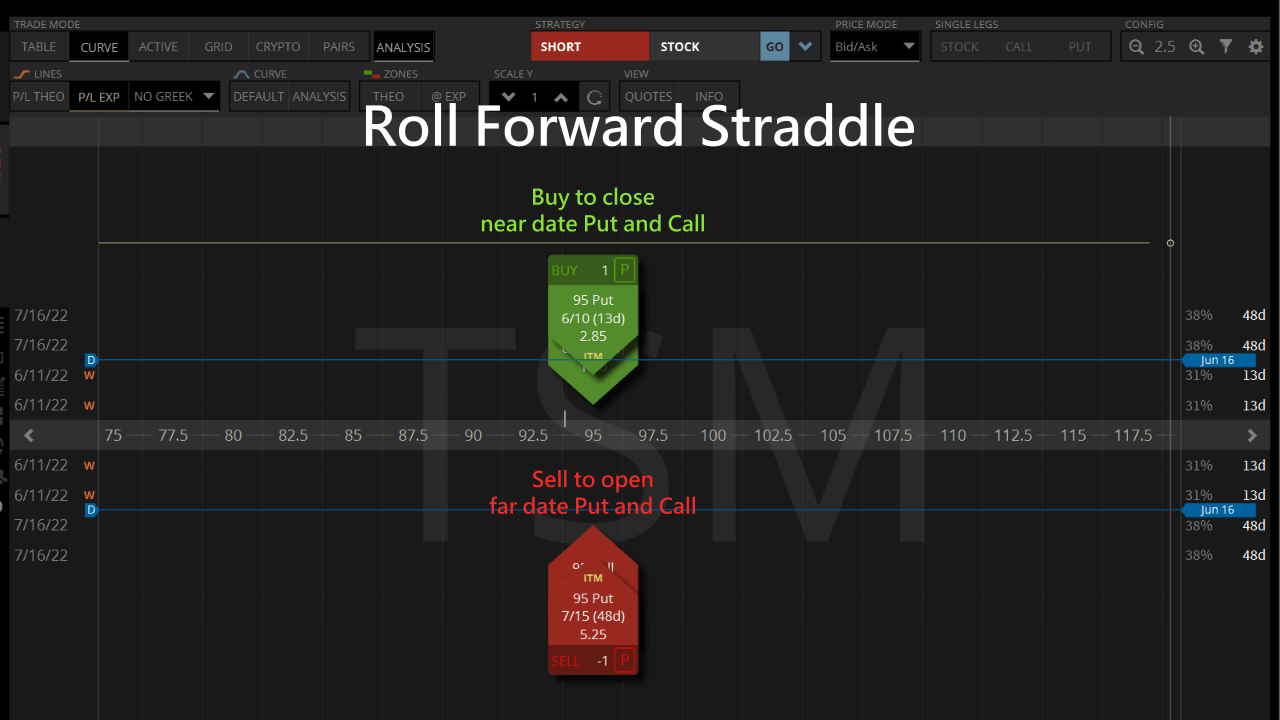

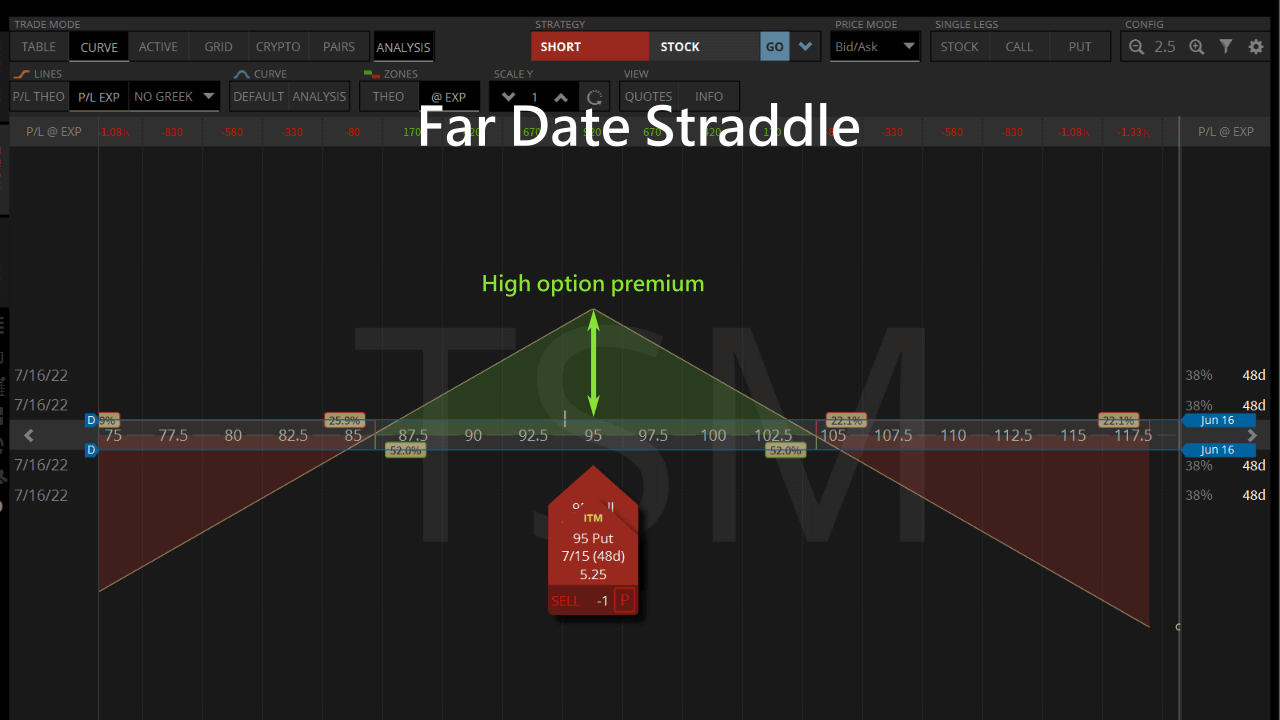

Roll Forward the Straddle Just Before Expiration

If the Straddle is unprofitable less than 14 days to expiration, we can roll the Straddle to a later date.

We can see a TSM Straddle near expiration is running out of time value.

If we believe the stock price can revert back within the profitable range, we can roll the Straddle forward to a later expiration, and use the extra premium to offset previous losses:

- Buy to close the current Put and Call options.

- Sell to open future Put and Call options.

It would result in a Straddle with a longer expiration, letting us create a wider profitable range with the additional premium received. Then we can wait for the TSM stock price to revert back within our expectation and profit from the time value decay.

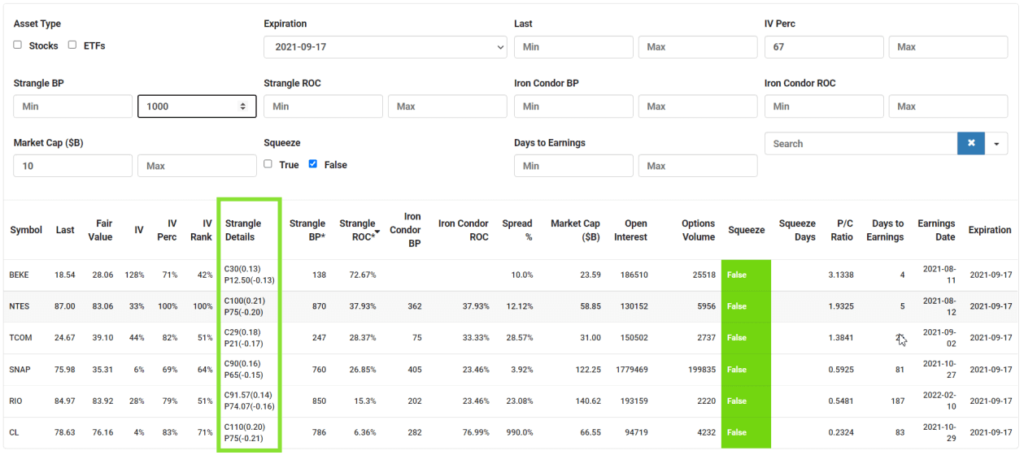

The Best Short Strangle Options Right Now

SlashTraders' Options Scanner is designed to find high probability and high return Strangles in seconds. Here are some tips to use the filtering function to find the best short Strangle entry points.

- We want to choose opportunities with longer than 30 DTE to get the safest theta decay.

- IV Perc is the relative position of current IV compared to the range of IVs in all the trading days in the previous year. We can filter IV Perc >67% to find stocks with IV higher than 2/3 of trading days in the past year. High IV stocks have a high chance of contracting IV and vega in our favour.

- Open Interest is the number of the total number of outstanding derivative contracts for the underlying. We can find stocks with Open Interests >100,000 to make sure the liquidity is good, so we get our trades filled easily.

- By choosing Market Cap ($B) larger than 10 billion, we avoid choosing stocks that can get manipulated and explode like GME.

- A good idea is to eliminate stocks with depressed price movement, because IV will expand soon after. So we need to choose Squeeze status as False.

- To further reduce risks, we can limit the Strangle BP to less than $1000, so we can easily diversify our portfolio.

Finally, we can sort the Strangles ROC by descending order to get a shortlist of the highest return Strangles.

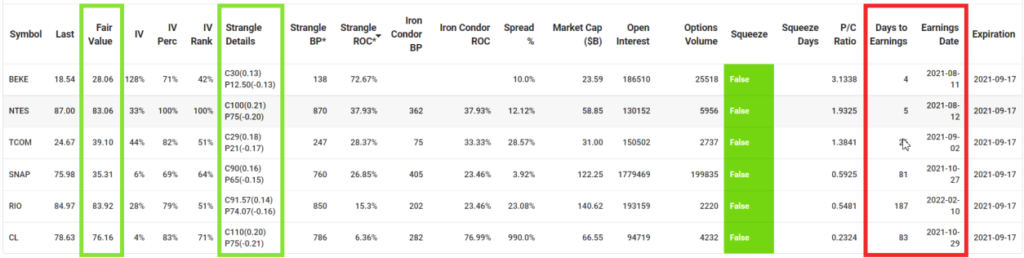

You can see the Fair Value and Earnings Date for every underlying to help us fine-tune the selection and get the best entry points.

If the Fair Value is very close to the strikes listed in the Strangle Details, we can be even more confident that the Strangles will be profitable.

Earnings Date is an event that can cause large price movements, so we want to avoid selling neutral options strategy past Earnings Date.

We can see the top 3 stocks with highest return have upcoming Earnings, so selling Strangles for them are quite risky.

SNAP's Fair Value is on the low side, but considering that SNAP and FB both have robust social media platforms, consider selling SNAP's Strangles option.

If we sell to open a Strangle for SNAP that expires in 40 days, it has a 27% maximum return if SNAP stock price does not exceed the Put and Call strike prices before options expiration.

Now you don't have to worry when a Strangle strategy goes bad. We can repeatedly roll up or roll down the profitable legs until we get a Straddle.

When it is close to expiration, we can roll the Straddle to a later expiration and wait for the stock price to revert to our expectations.

SlashTraders vs S&P 500: 450% Outperformance, Verified Trades and How to Copy Every Alert