Do you know even if the stock price doesn't move, you can still profit by trading options?

You can sell ATM Put and Call options, to make the most premium. If the stock price doesn't move before expiration, the neutral options strategy will profit.

Today, SlashTraders will show you how to use the Options Scanner to find high probability and high return short Straddle options strategies. So you can profit even when the stock price doesn't move.

What Is Short Straddle Options Strategy?

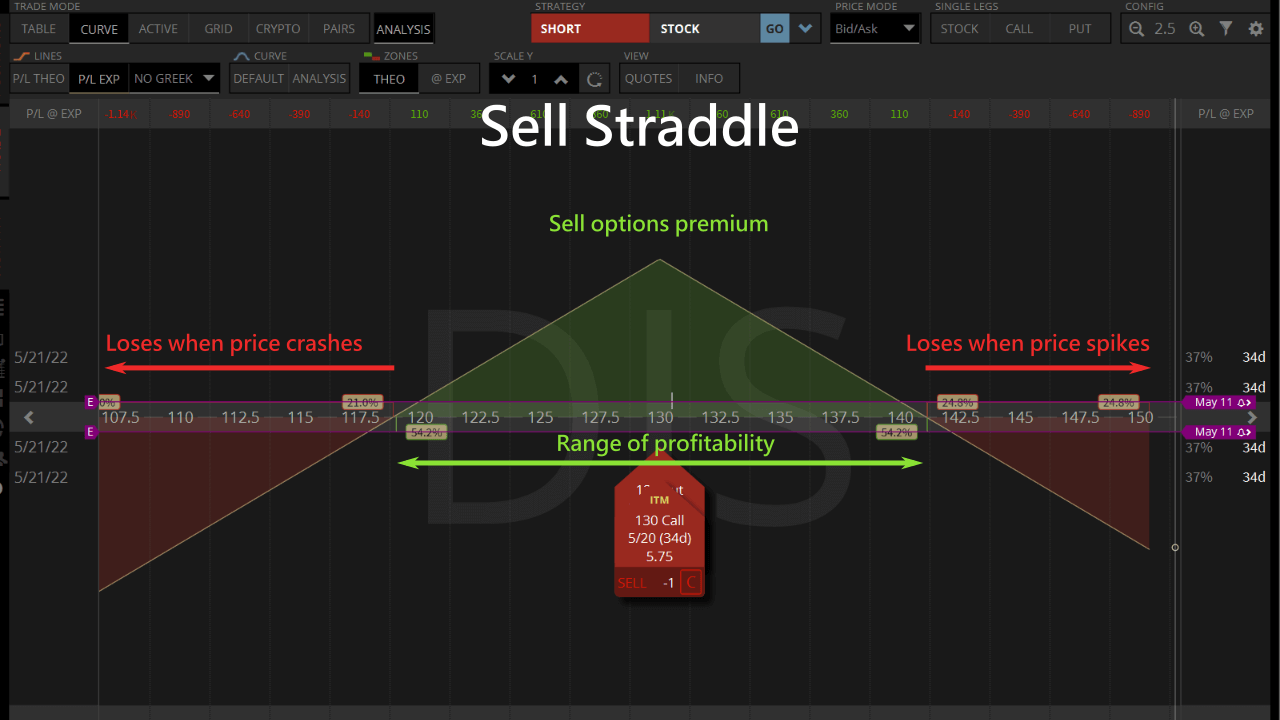

A short Straddle options strategy works by selling an ATM Put and an ATM Call to receive a huge premium. As long as the underlying price does not move beyond the breakeven prices before expiration, the Straddle seller can buy to close the two options for profit.

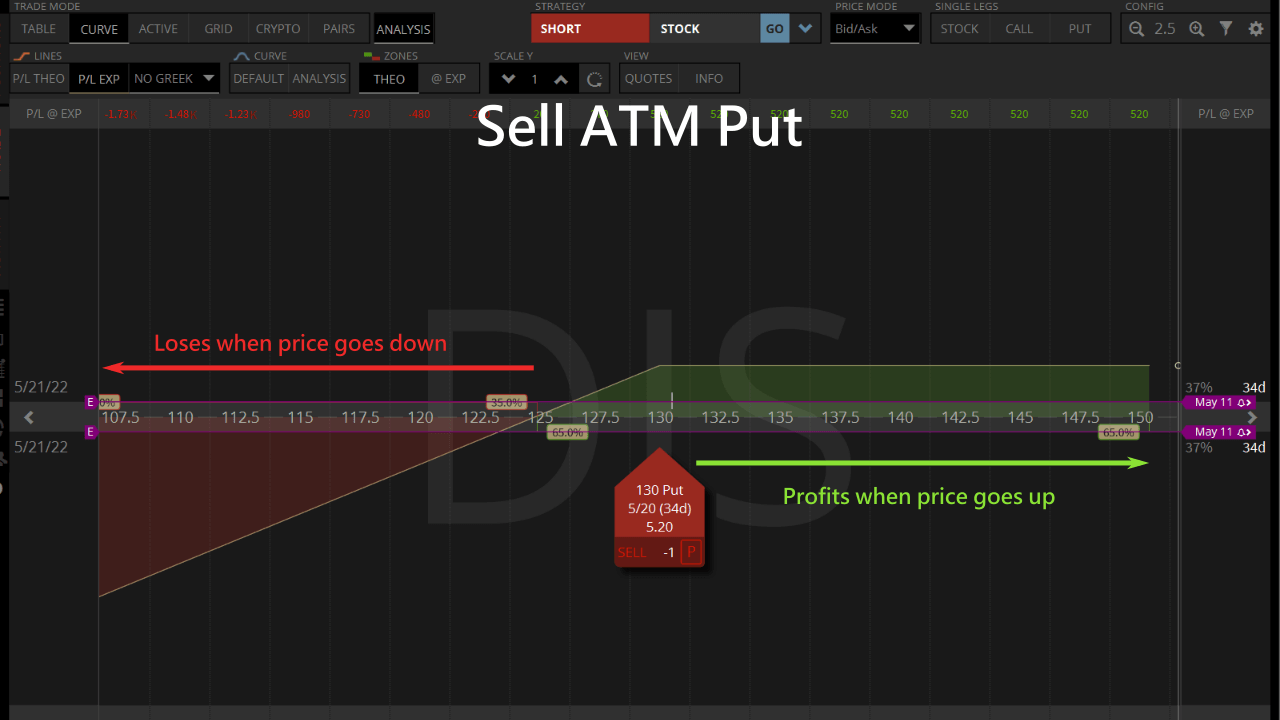

Let's use the Disney stock to analyse the profitability of selling ATM Call and ATM Put options. We receive a premium when we sell the ATM Put. If the underlying price doesn't fall, the Put option value will depreciate and we earn a profit.

But if the stock price drops beyond the Put strike, the maximum loss is buying 100 worthless stocks at the strike price.

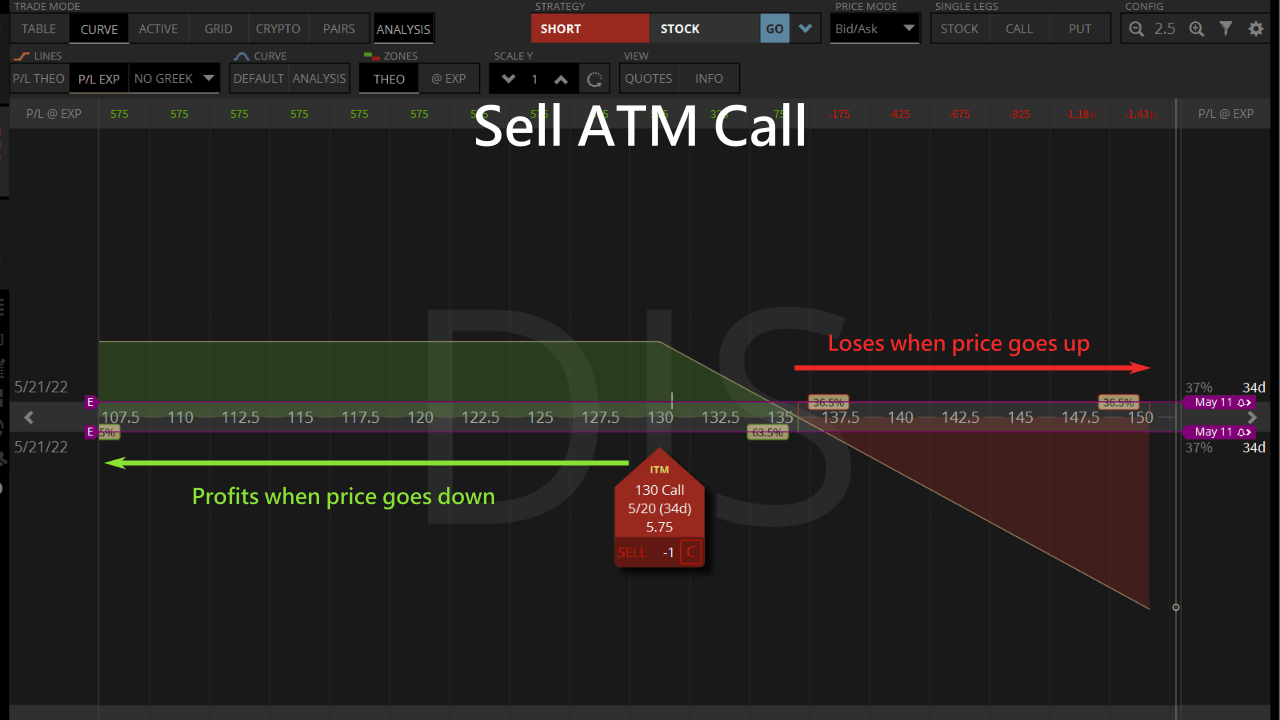

We also receive a premium when we sell an ATM Call option. If the underlying price doesn't increase, the Call option value will depreciate and we earn a profit.

But if the stock price increases beyond the Call strike, the maximum loss is infinite.

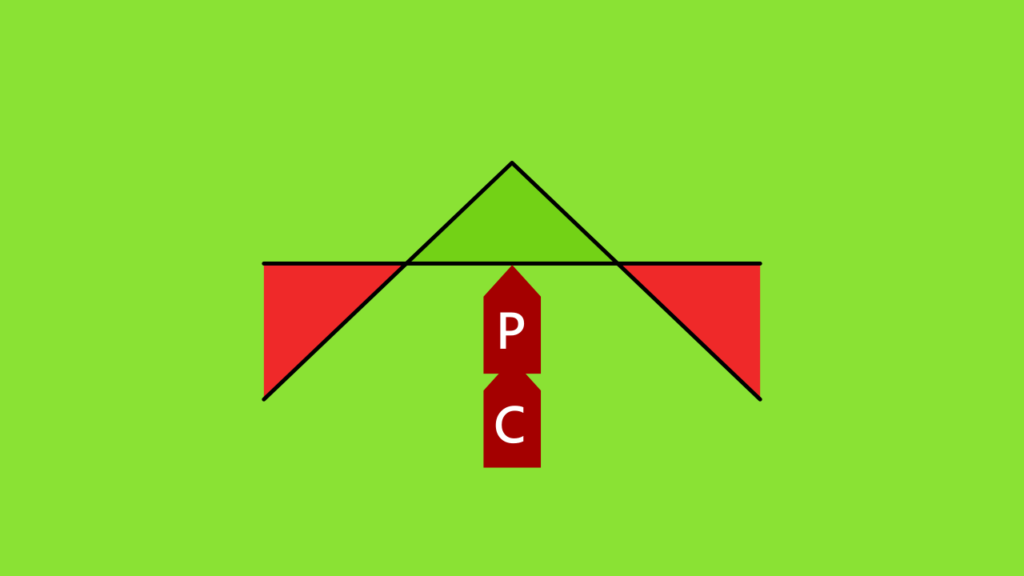

When we combine selling an ATM Put and an ATM Call we get a Straddle. The premium received defines the range of profitability in DIS stock prices.

If the underlying stock price doesn't move beyond the boundaries before expiration, the neutral Straddle strategy will be profitable.

What Is the Risk of a Short Straddle?

A short Straddle is made up of a short naked Put and a short naked Call. So the risk of a Short Straddle is that it can have unlimited losses when the stock price rises or falls in a big way.

| Price direction | Maximum loss to a short Straddle |

|---|---|

| Bullish | Unlimited |

| Bearish | Strike price x 100 - premium |

If you are worried about the high-risk short Straddle, you can try trading an Iron Butterfly instead, which has a defined maximum loss.

What Are the Key Points to Profitable Straddles?

We want both theta and vega to depreciate the options prices, so we can sell high price Straddles to open, and buy to close for a profit.

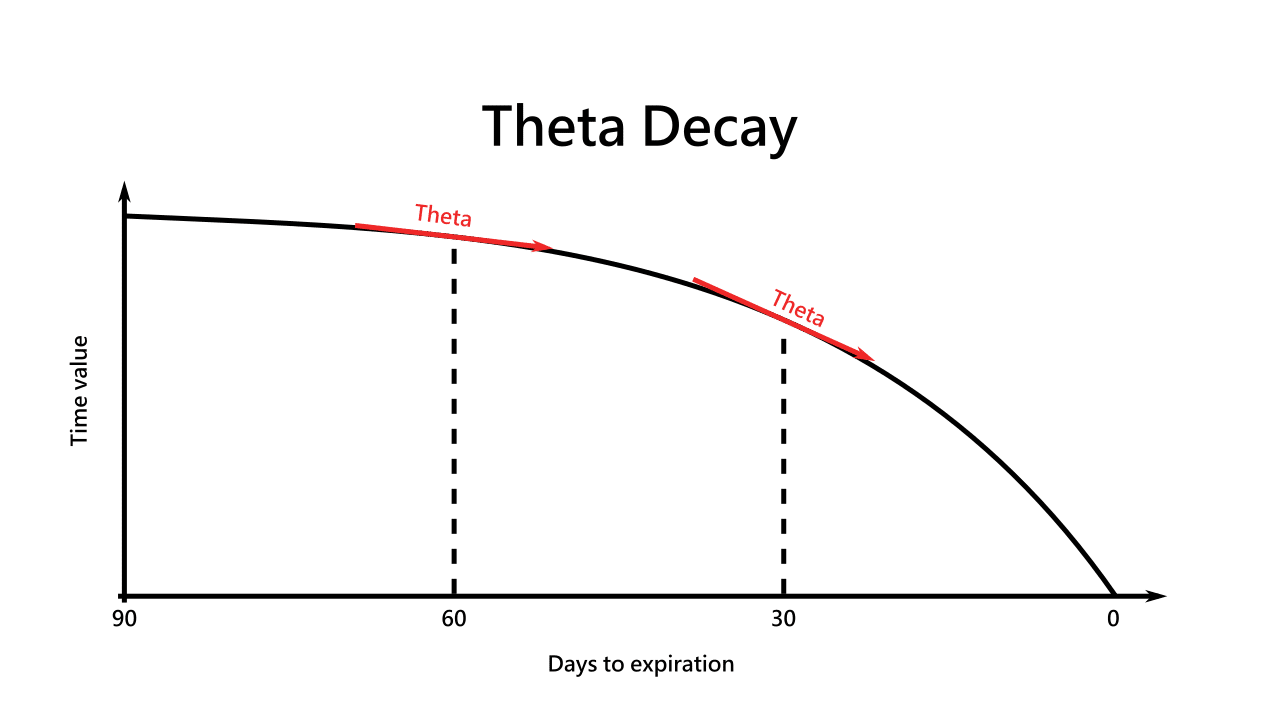

Theta is the changes to options value with respect to changes in time.

From our experience, selling options with more than 30 days to expiration have a predictable time value decay, and the gamma risk to the options price is lower. So we can be patient and earn a profit as time passes.

Vega is the changes to options value with respect to changes in IV.

Since we want to sell high and buy low, we need to sell to open at high IV, then buy to close when vega causes the option's value to decay at low IV.

We also need to find underlying opportunities with low volatilities. We can do that by picking stocks with price trends that rarely exceed Bollinger Bands, and also stocks with high market capitalisation to reduce the risk of manipulation.

If the Straddle is losing near expiration, we can consider rolling the straddle to a later date to offset the losses with extra premium. Then we can patiently wait for our trade to become profitable.

How to Find the Best Straddle Options

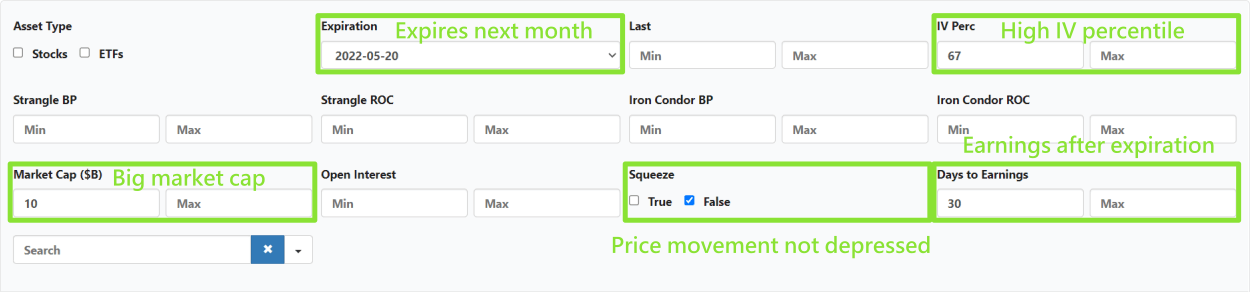

SlashTraders' Options Scanner is designed to find high probability and high return Straddles in seconds. Here are some tips for using the filters to find the best Straddle entry points.

- We want to choose opportunities with greater than 30 DTE to get the safest theta decay.

- We can filter IV Perc >67% to find opportunities that have a high chance of contracting IV and vega in our favour.

- By choosing Market Cap larger than $10 billion, we avoid choosing stocks that can get manipulated and explode.

- A good idea is to eliminate stocks with depressed price movement, or in a Squeeze, because IV will expand soon after.

- We can also avoid stocks with upcoming Earnings Dates, to avoid big price fluctuation due to the Earnings report.

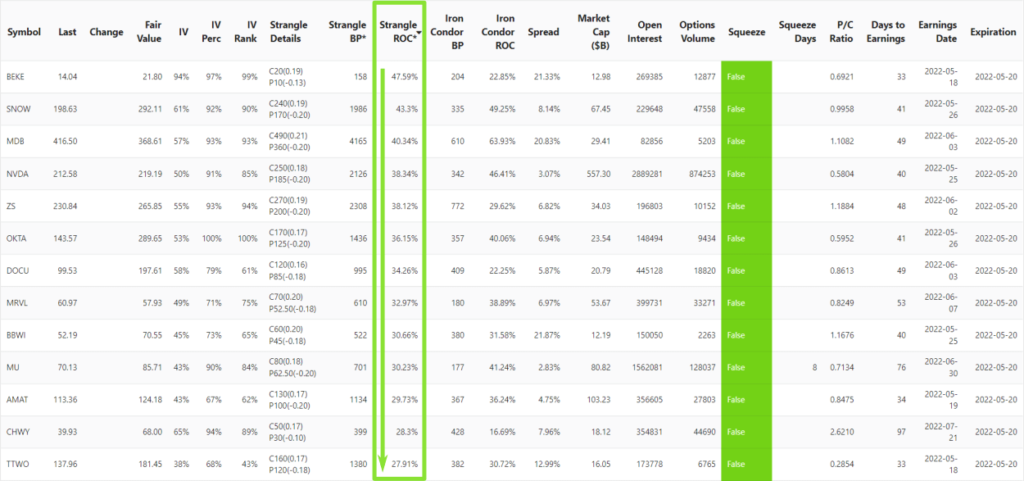

Since the mechanics of Strangles and Straddles are similar, we can use Strangle ROC to find high return Straddle entry points.

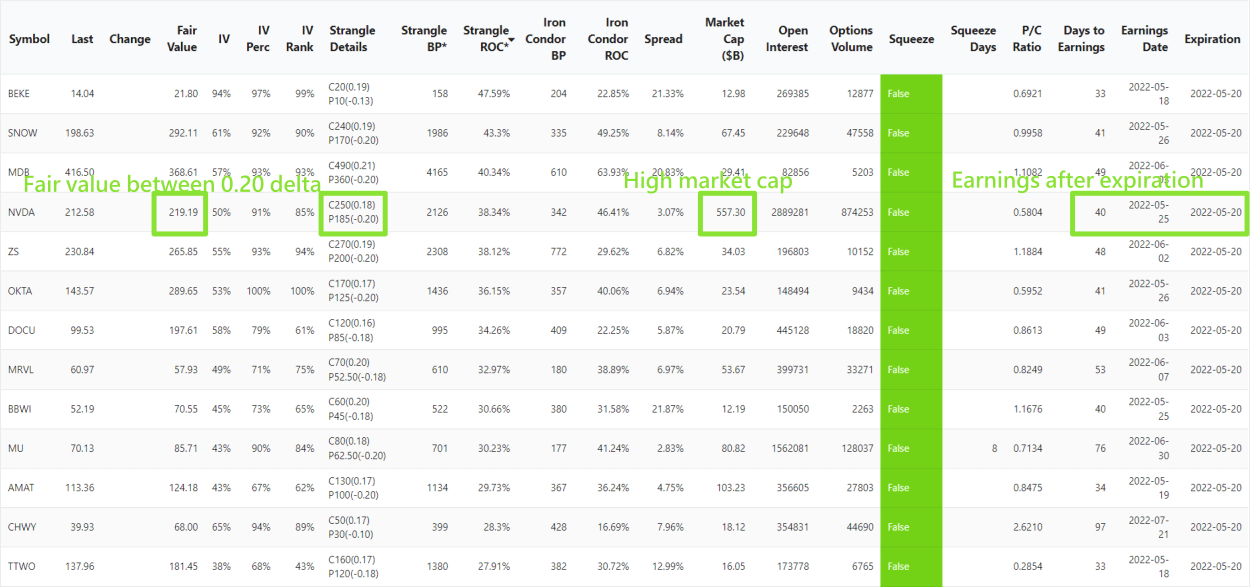

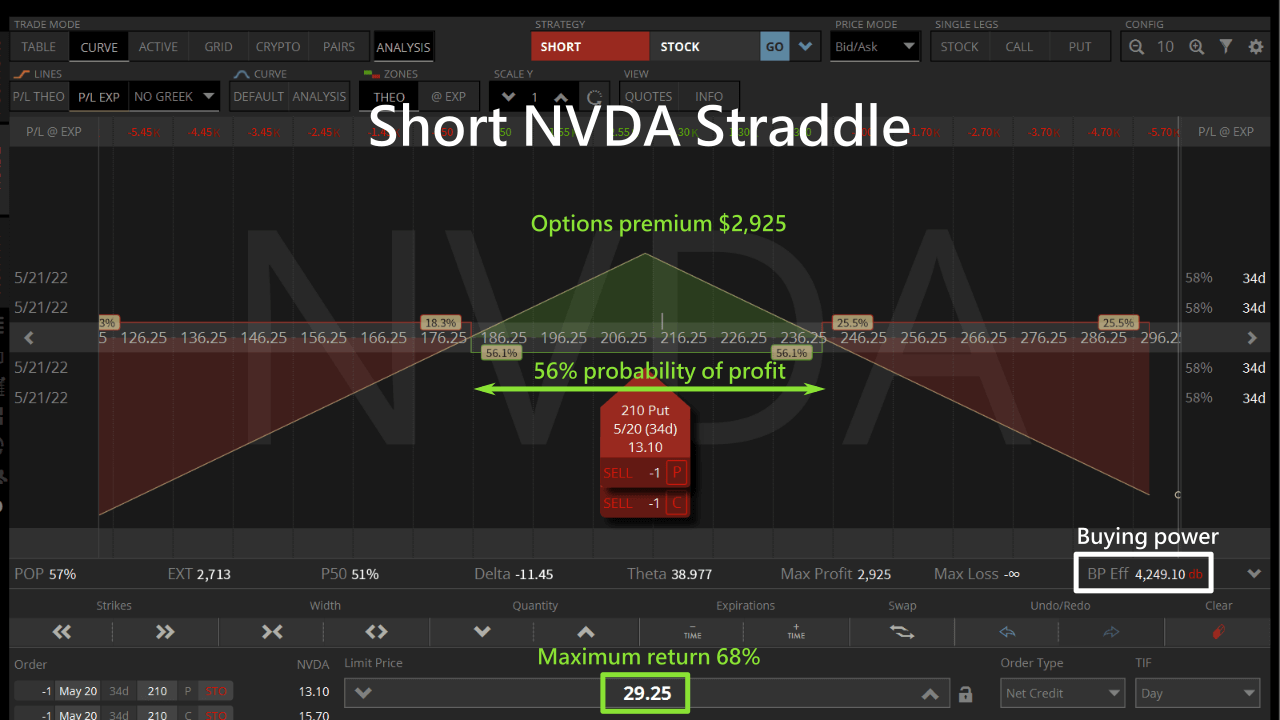

We can see NVIDIA is on the shortlist of high return Straddle opportunities right now.

- NVDA's Fair Value is $219, which falls within the recommended 0.20 delta Strangle Details of $185-$250.

- NVDA's Earnings Date is 40 days later at 5/25, which makes selling options that expire on 5/20 pretty safe.

- NVDA's Market Cap is more than $550 billion, making it an unlikely candidate for manipulation.

We can sell to open a Straddle for NVDA that expires in 34 days to collect $2,925 in premium, which defines our range of profitability.

If NVDA stock price does not exceed the breakeven price range before expiration, we can profit from the trade.

SlashTraders vs S&P 500: 450% Outperformance, Verified Trades and How to Copy Every Alert

Great breakdown of the straddle option strategy and its potential in various market scenarios! This approach is particularly useful for traders This approach is particularly useful for traders anticipating significant price movements but unsure of the direction. The detailed examples and insights in this article make it easier to understand how to effectively use this strategy. Thanks for sharing such practical and actionable content!

Is a short straddle a good strategy for ETFs?

A short Straddle is great when the underlying doesn't fluctuate a lot.

If an ETF has historically been stable in price, then it may be a good candidate for short Straddles.