你知道即使股價不動,還是可以用選擇權獲利嗎?

只要搭配Put Spread和Call Spread就可以定義出一個低風險的中性期權交易。

今天斜槓投資達人要分享如何用選擇權分析神器找到高機率和高報酬的Iron Condor鐵兀鷹選擇權進場,讓你趁著股價不動的時候賺錢。

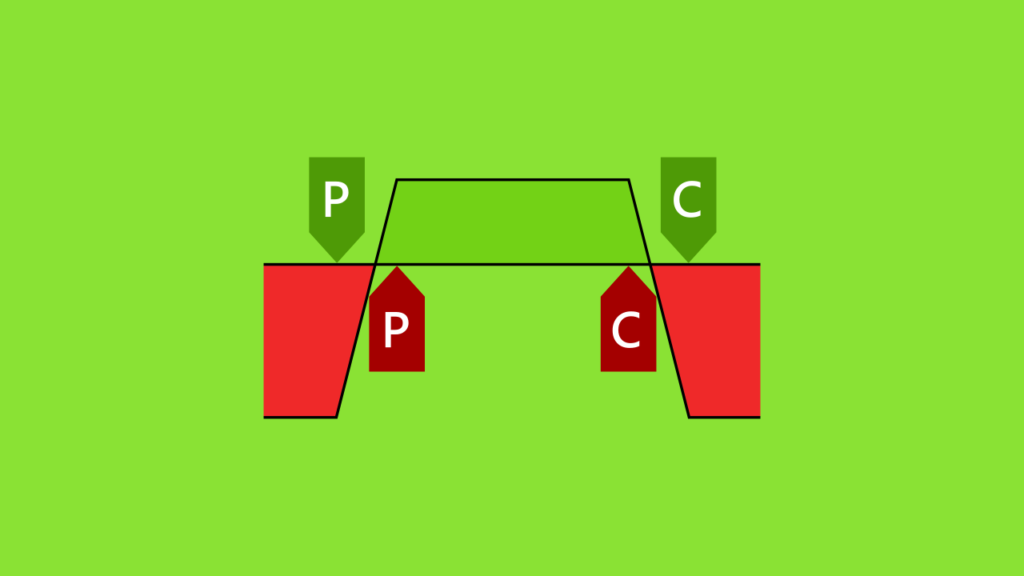

什麼是鐵兀鷹選擇權策略?

鐵兀鷹選擇權策略是由賣Put Spread和賣Call Spread來定義一個獲利區間,只要在期權截止前股價波動不大,股價維持在賣Put和Call的合約價之間,賣出的四個期權貶值後,賣家就會獲利。

我們來複習一下賣看漲Put Spread和看跌Call Spread的獲利機會,當我們賣看跌Call Spread時會先得到收入,只要股價在期權截止前不漲,Call垂直價差貶值我們就會獲利。

如果股價上漲超過履約價,最高損失是垂直價差的寬度乘以100減收入。

當我們賣看漲Put Spread選擇權時也會先得到收入,只要股價在截止前不跌,Put垂直價差貶值我們就會獲利。

可是如果股價下跌超過履約價,Put垂直價差的最高損失也是Spread的寬度乘以100減收入。

我們結合看跌Call Spread和看漲Put Spread就能知道為什麼交易鐵兀鷹Iron Condor,Put Spread會定義股價可以移動的下限,Call Spread定義股價可以波動的上限。

當我們覺得一個股票在截止前不會大幅度漲跌,就可以賣鐵兀鷹選擇權獲利,而且最大虧損機會是被限制住的。

鐵兀鷹最大虧損 = 垂直價差寬度 x 100 – 收入

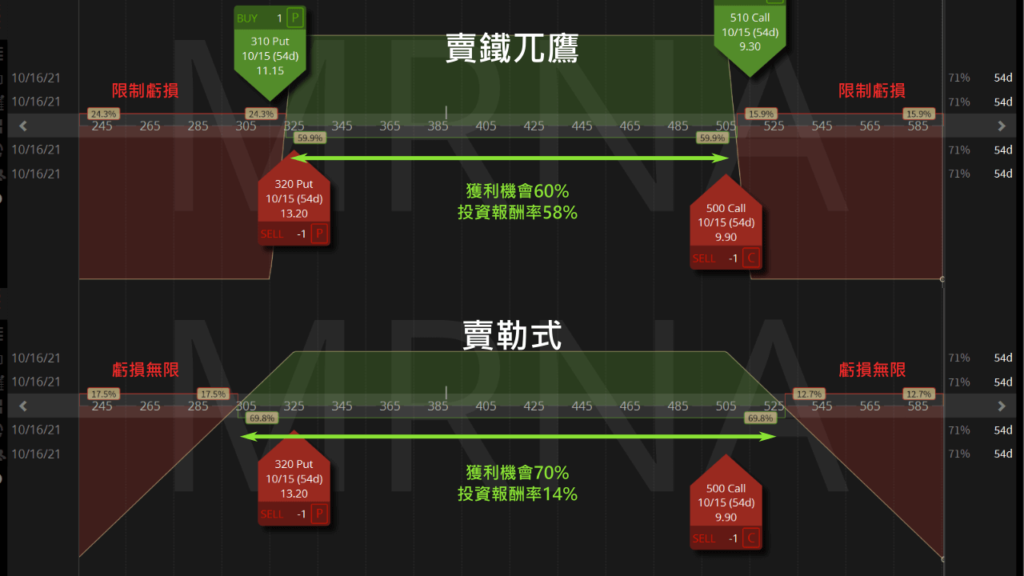

交易鐵兀鷹和勒式有什麼不一樣?

鐵兀鷹和勒式Strangle雖然同樣是中性策略可是獲利分析有很大的不一樣。

我們比較兩種策略的獲利分析,只要股價沒有大幅漲跌兩種選擇權策略都可獲利。

鐵兀鷹的最大損失是有限的,而賣勒式時如果股價超出Put和Call的價格,最大損失是無上限。

當鐵兀鷹的交易虧損時,我們可以roll up或roll down垂直價差來調整Iron Condor。

當Strangle虧損時,我們可以將期權roll到未來補救Strangle。

什麼時候賣鐵兀鷹最好?

賣鐵兀鷹時需要theta和vega的走勢讓期權價值衰減,讓我們在高價時賣Iron Condor進場,低價買回Iron Condor出場。

Theta是時間對期權價格的影響

從我們的經驗來看,如果賣30天以外截止的OTM選擇權,時間流逝時theta對選擇權價格的影響比較可預期,只要股價波動不大,我們可以等待用時間來獲利。

Gamma是股價對delta的影響,也是股價對期權價格的加速度

當選擇權快要截止時gamma會越大,選擇權價格會越不穩定,所以不管鐵兀鷹有沒有獲利最好在離截止前14天以上平倉或延後到下個月,期權價格比較不會因為gamma波動太大而造成損失。

Vega是IV隱含波動率對期權價格的影響

因為我們要賣高買低,所以我們要在股票IV高的時候sell to open選擇權進場,當IV萎縮vega造成期權價格貶值的時候buy to close出場。

另外我們也要挑選股價波動相對小的股票,最好是挑選市值比較高、股價比較不會被操作的公司賣選擇權比較安全。

選擇權分析神器的最佳鐵兀鷹交易設定

選擇權分析神器主要是針對挑選高機率、高獲利的中性交易而設計,我們來看一下要怎麼使用篩選功能找到最佳的鐵兀鷹進場時機。

- 為了符合良好的theta衰退速度並避開gamma風險,我們用選擇權分析器挑選下個月至少30天以外的截止日Expiration。

- 另外我們也要挑選IV Perc至少67%以上,未來有高機率IV和vega會萎縮。

- 市值Market Cap也要大於$10 billion,避免碰到像AMC一樣股價被操作暴衝。

- 也要排除股價現在波動被壓縮的狀態避免未來IV膨脹,所以要選擇沒有Squeeze的股票。

- 也可以篩選30天內沒有公布財報的股票,避免因為發表財報而碰到大幅漲跌。

- 最後再將Iron Condor ROC從最高排序,找到最高投資報酬率的Iron Condor交易機會。

我們照著剛才的條件在選擇權交易神器操作一次,最後就會找到最安全、獲利也最高的0.20 delta賣鐵兀鷹機會。

現在最佳的鐵兀鷹交易進場機會

既然我們找到一系列最安全、獲利最高的鐵兀鷹選擇權,我們再挑出最好的進場機會。

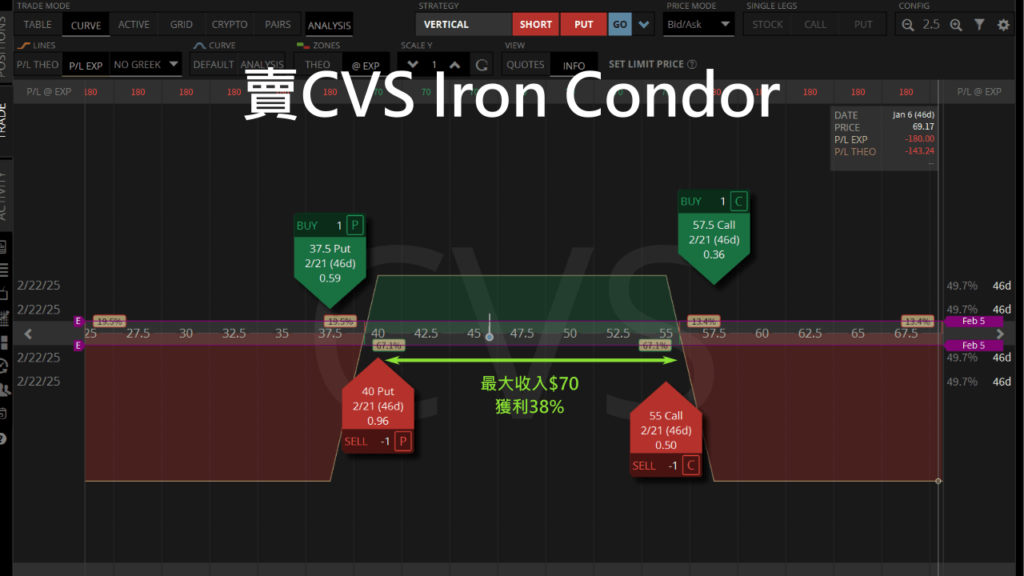

我們可以從清單裡用Options Volume找到交易量比較高的股票,例如現在清單裡的鐵兀鷹裡可以看到CVS的Options Volume比其他股票高,所以交易CVS比較容易成交,所以我們可以試著交易CVS的Iron Condor期權。

| Symbol | IV Perc | Strangle Details | Iron Condor BP | Iron Condor ROC | Market Cap (000s) | Options Volume |

|---|---|---|---|---|---|---|

| CEG | 73% | C300 (0.18) P220 (-0.18) | $715 | 39.86% | $69,969,016 | 106,399 |

| FTAI | 75% | C180 (0.18) P130 (-0.16) | $358 | 39.86% | $14,771,256 | 32,488 |

| CVS | 82% | C55 (0.14) P40 (-0.20) | $180 | 39.28% | $56,489,919 | 59,935 |

| FANG | 87% | C190 (0.19) P155 (-0.16) | $365 | 36.99% | $47,836,590 | 12,725 |

| TCOM | 81% | C80 (0.18) P60 (-0.18) | $385 | 29.87% | $44,705,131 | 3,535 |

我們賣一個46天後到期的CVS鐵兀鷹,如果截止前CVS股價沒有超出賣Put和賣Call的合約價,當四個期權失效可以得到38%的投資報酬率。

Great iron condor strategy! For exit point, say at 20% of initial credit, how do we set the exit point in IBKR?

Hi, we’re not familiar with IBKR, but I guess it might involve the Stop Orders.

https://www.interactivebrokers.com/en/trading/orders/stop.php#:~:text=Form%20the%20Order%20Type%20dropdown,order%20to%20remain%20in%20place.

Hi Tony,

Is there a assignment risk with Iron Condor Strategy?

Could you please clarify. Thanks !

Hi,

Iron Condors have long Call and Put contracts to limit the losses in the event of assignment.

So the assignment risk is minimal.

Thank you Tony !

Could you comment on exit strategies – specifically yesterdays exit from the MSFT 340/345 position? Your entry signals are pretty clear but knowing when to close out would seem as important. Thanks – I’m quite impressed with your general approach.

Our exit strategy is to close at 10-20% of the initial credit.

We usually do not close any vertical early on because we want to give the trades enough time to materialise.

It’s a good idea to setup GTC closing orders at about 10% of the initial credit to minimise the stress of checking the market constantly for the exit.

Another reason for not closing early is that once the price moves against our position, it is not easy to close unless we accept a very unfavourable bid/ask spread. Because the further the price moves away from ATM, the liquidity drops significantly.

As for the MSFT trade, I entered MSFT without having had a solid signal (emotional decision) and as soon as I entered, it moved against me.

Therefore, I exited the position to minimise the loss.

You said MRNA has a greater Options Volume than RIO, what does RIO mean???

I feel dumb but I figured it out lol so is there anything besides volume we should consider when picking one these stock results?

Hi Stephan,

We want to choose opportunities with greater than 30 DTE to get the safest theta decay and less gamma.

IV Perc >67% to find opportunities that have a high chance of contracting IV and vega in our favour.

By choosing Market Cap ($B) larger than 10 billion, we find stocks that are less likely to be manipulated in price.

A good idea is to eliminate stocks with depressed price movement, or in Squeeze, because IV will expand soon after.

We should also avoid underlying that have an upcoming Earnings Date in 30 days to reduce the chance of large fluctuations.

Finally, we can sort the Iron Condor ROC by descending order to get a shortlist of highest return Iron Condors.

Thanks Tony, I thought it’s better to buy at least 10 delta lower from sold strike either side to have quicker time decay, is that correct?

Having wider strikes for Iron Condors gives you a more significant premium.

But it does come as a trade-off of higher maximum loss if the trade goes wrong.

Love your tips on finding the best stocks to trade iron condors

We really need to avoid meme stocks when trading neutral option strategies

That’s right, we need to find stable stocks with overstated IV to trade Iron Condors.

Great article, thanks very much for the insightful read. Could you possibly speak more (or link to an article if you’ve already written on this) about how we can adjust the strikes of each leg so that we can obtain the maximum theta possible? In an ideal world, it would be nice to hold to expiration, but in the real world, my understanding is that it’s best to close a few weeks out or when you’ve met your profit objective. In short, how do we create the best IC setup to have the fastest decay?

Thank you for your kind words.

We like to have the inner strikes 0.20 delta on either side of the market price, and the outer strikes one step further out, shown in our Options Scanner.

To get the best theta decay, we also choose the expiration at around 45 days.

Yes, we usually close our trades around 14 days before expiration, or when we reached 50% or more profit.

Finally a good tutorial on how to find good Iron Condor entry points.

Thanks

You’re welcome

Thank you for the tips in picking the best stocks for iron condors

I’ll give it a try

Yes, you’ll find that using the options scanner can help you consistently find high probability iron condors to trade

我很愛中立策略 但最近台指中立很難做 IV太低 幾乎收不到多少權利金

但我沒投資過美股 更不用說選擇權了 加上本身不會英文 需要適應一下

希望可以上手 這樣就不會只有台指選擇權能做了 而是更多選擇

當IV高時交易中立策略是不錯的選擇,不過現在IV偏低不適合進場

美股交易期權的選擇很多,可以試試看

終於找到可以快速篩選高IV的鐵兀鷹分析器了,謝謝

沒錯,只要挑選高IV的時候進場,鐵兀鷹期權是很棒的中性交易方式

Hi Tony, your pick is set short side at delta 20, how about long side? So strategy stated that short call put at delta 30, long call put at delta 16, what’s your opinion?

Hi Nathan, I would choose the long side as the nearest strike further away from the short side.

Since different stocks at different expiration have different step-sizes of the strikes (usually $5-10), I usually pick short strikes at 20 delta, and choose long strikes 1 step further out.

This usually gives me the best ROC with balanced risk.

Choosing 30 delta short and 16 delta long for higher ROC can work if we feel the underlying’s IV will compress before expiration.

How do you choose the underlying to sell iron condors?

Short iron condor strategy works best when you expect the underlying price to not fluctuate a lot

So we sell iron condors when the IV percentile is high, as we expect the high IV to regress to a lower IV in the near future

And we’ll profit from vega

謝謝分享這麼簡單易懂的鐵兀鷹交易方式,讓我也想試試看中性的選擇權交易策略了

期待聽到您操作鐵兀鷹後的心得

Thank you for sharing the Iron Condor tips.

How do you pick the minimum ROC for Iron Condors to make the profit/risk balance worthwhile?

TastyTrade recommends a 1/3 width of the strikes as premium, which means 50% ROC

When you sort the Options Scanner by Iron Condor ROC, pick opportunities with ROC around 50% to follow TastyTrade’s recommendation.

Love the options scanner guys, I can’t trade iron condors and strangles without it now!

Glad you like it!

Thank you very much for the helpful information about how iron condor works

You’re welcome