We have all heard of the 4% rule as the guide to retiring early. As long as we don't withdraw more than 4% of our savings each year, we can maintain the same quality of life without ever running out of retirement funds.

We talk about how the 4% rule works, and how to pick stocks with more than 4% dividend yield to speed up your passive income for early retirement.

What Is the 4% Rule?

The 4% rule is a shortcut to calculating the Safe Withdrawal Rate from your retirement savings. If you withdraw no more than 4% of your total equity each year, then you can enjoy a comfortable lifestyle and never run out of money.

How Long Can You Live on the 4% Rule?

When William Bengen discovered the 4% rule in the 90s, he first analysed the market performance and different retirement scenarios over the past 75 years to find a safe withdrawal rate. Then he proposed that as long as you don't withdraw more than 4% of your life savings per year, you will never worry about running out of money in your lifetime.

We are confident the 4% rule can let us enjoy at least 30 years of retirement.

The 4% Rule Formula for Retirement

Since we want to keep our costs below 4% of our total equity, we simply multiply our annual expenses by 25 to find our target retirement fund.

Target Retirement Savings = Annual Expenses x 25

So we can create a comparison where our annual expenses meet the target retirement savings. This shows we can speed up our retirement by reducing costs in our lifestyle and accumulating wealth through savings.

| Annual expenses | Target retirement savings |

|---|---|

| $10,000 | $250,000 |

| $20,000 | $500,000 |

| $30,000 | $750,000 |

| $40,000 | $1,000,000 |

| $50,000 | $1,250,000 |

| $60,000 | $1,500,000 |

| $70,000 | $1,750,000 |

| $80,000 | $2,000,000 |

| $90,000 | $2,250,000 |

| $100,000 | $2,500,000 |

Why Use the 4% Rule?

There are a few advantages to planning your retirement with the 4% rule:

- The rule helps us set a money-saving goal quickly, and maintain good money habits.

- It is a time-tested, believable rule of thumb.

- A disciplined withdrawal rate of less than 4% should maintain a consistent quality of retirement.

Risks of the 4% Rule

Here are some risks to planning your retirement with the 4% rule:

- In the event of big and unexpected inflation, a 4% withdrawal rate may not be enough.

- Some people may feel leaving too much savings behind as inheritance is missing out on a better quality of life.

- The retirement cash flow may not be enough to cover medical emergencies and other unexpected expenses.

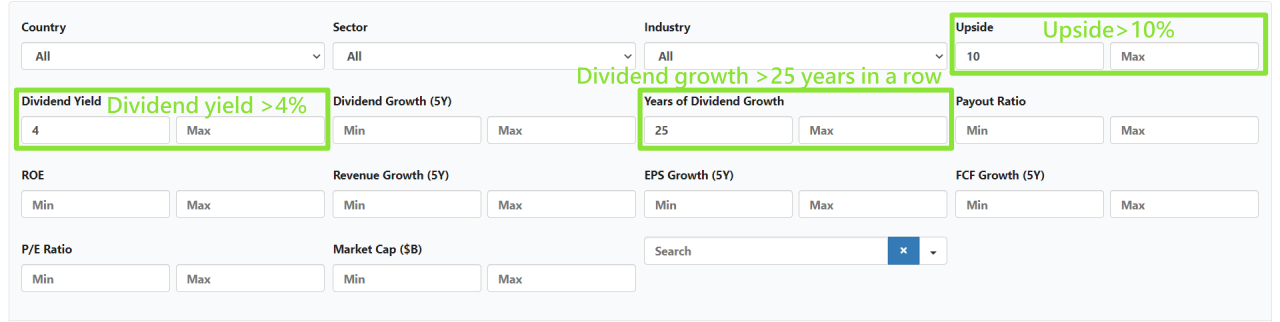

How to Pick Stocks With More Than 4% Dividend Yield

Since we want to retire with 4% of our equity, we can use the Dividend Stock Picker to find blue-chip stocks with more than 4% yield for long-term investment. So we can live on the dividends during retirement.

We can find long-term investment opportunities like dividend kings and dividend aristocrats:

- With more than 25 consecutive years of increasing dividends.

- More than 4% dividend yield.

- Also more than 10% in Upside so we have enough margin of safety to avoid stock price crashes.

- We also need to avoid value traps, to prevent buying and owning losing stocks.

Finally, we sort the list by Dividend Yield. We get a list of value stocks with a great dividend-paying record with more than 4% yield.

| Stocks | Description | Last | Fair value | Upside | Dividend yield | Years of dividend growth |

|---|---|---|---|---|---|---|

| WBA | Walgreens Boots Alliance Inc | $29.98 | $37.78 | 26.02% | 6.43% | 48 |

| WPC | W.P. Carey Inc | $66.45 | $73.99 | 11.35% | 6.43% | 26 |

| UGI | UGI Corp | $24.43 | $31.59 | 29.31% | 6.14% | 36 |

| FLIC | First of Long Island Corp | $13.85 | $19.38 | 39.93% | 6.06% | 27 |

| MMM | 3M Co | $105.49 | $118.67 | 12.49% | 5.69% | 65 |

| AROW | Arrow Financial Corp | $20.44 | $31.03 | 51.81% | 5.28% | 30 |

| NNN | National Retail Properties Inc | $40.32 | $45.81 | 13.62% | 5.19% | 34 |

| o | Realty Income Corp | $59.22 | $67.85 | 14.57% | 5.18% | 30 |

| NWN | Northwest Natural Holding Co | $41.33 | $47.05 | 13.84% | 4.48% | 67 |

The WBA stock has been increasing in dividends for 48 years straight. We can expect a 6.43% dividend yield for holding the stocks, with a 26% potential Upside for a bullish outlook. There is a high probability of providing us with passive income for retirement.

SlashTraders vs S&P 500: 450% Outperformance, Verified Trades and How to Copy Every Alert

The four percent rule is the greatest gift of all.

You're right.